Medicare is on a fiscally unsustainable trajectory. Policy experts rightly point out that the looming insolvency of Medicare’s Part A hospital insurance program risks sudden and sizeable cuts to benefit payments. But Medicare’s overall finances are much more precarious than the trust fund insolvency date suggests. Medicare’s rising costs are the number one programmatic factor driving unsustainable federal deficits and debt.

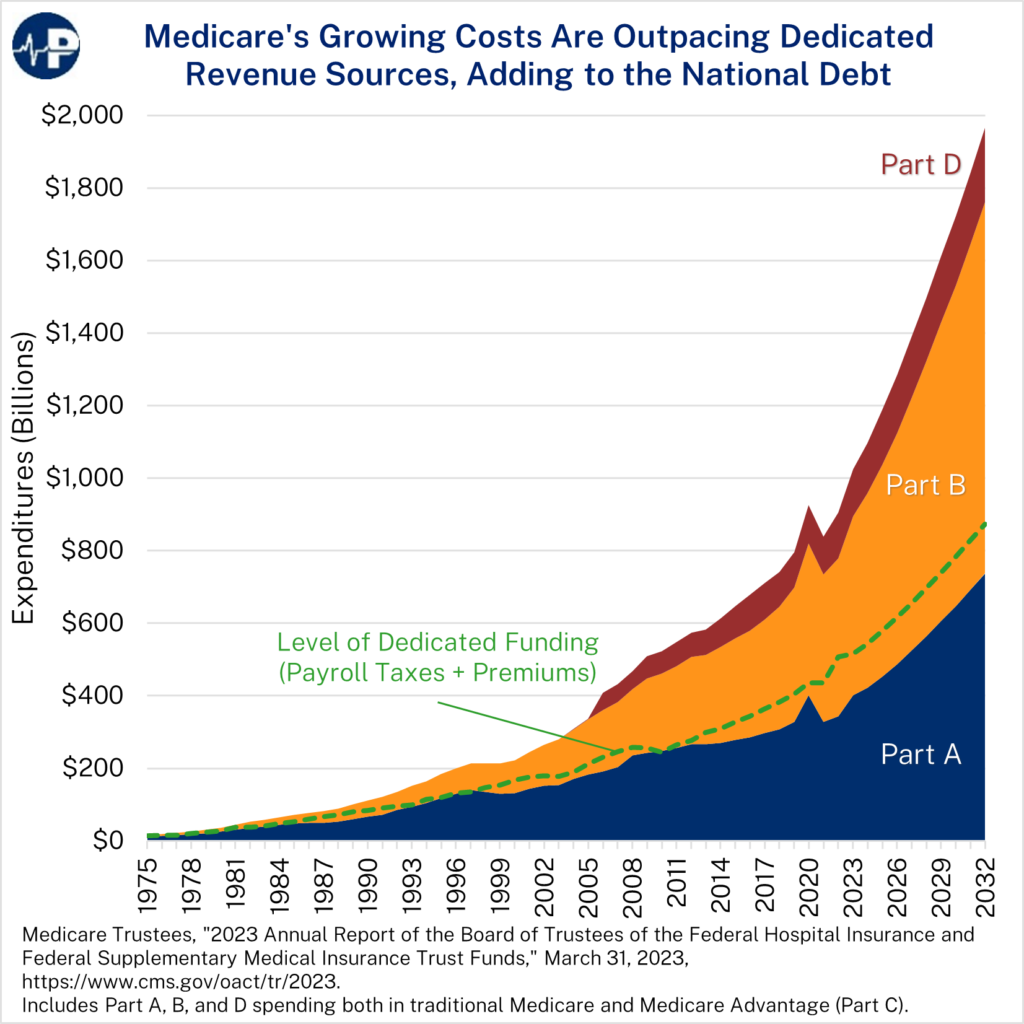

This week’s Paragon Pic shows that spending on every Medicare component is rising. Overall expenditures are outpacing Medicare’s dedicated sources of funding, mainly payroll tax receipts for Part A and beneficiary premium payments for the other parts.

The fastest growing part of Medicare is the Part B program, which mostly covers outpatient and clinician services. According to the Medicare trustees, Part B payments grew by 82 percent between 2013 and 2022. During that time, Part A payments grew by about 40 percent – less than half as much. Part B represented 48 percent of total Medicare expenditures in 2022.

Part B’s relatively high growth is due to several factors. On the positive side, medical innovations are allowing more services to shift from inpatient settings to lower-cost and lower-acuity ones like outpatient departments, ambulatory surgical centers, and physician offices.

On the negative side, excessive payments for certain services – such as outpatient hospital services and drugs – are also driving spending in this area. Between 2013 and 2022, Part B spending grew by 90 percent for hospital services and 113 percent for drugs, according to the trustees. This growth partly results from bad incentives created by misguided payment policies. For example, Medicare pays for routine services at a significantly higher rate when they are delivered in a hospital than when they are delivered in a physician’s office. It also pays an average of 48 percent above the maximum acquisition cost for drugs that hospitals acquire at a discount through the 340B program.

Part B does not face the same insolvency threat as Part A because most Part B funding comes from general revenue transfers rather than Medicare payroll taxes. (See this Paragon brief for an explainer of Medicare’s financing.) Every dollar spent on overpriced care in Part B is a dollar that cannot be spent on other public priorities – and another dollar added directly to federal deficits and debt.

Even without an insolvency date, the fiscal reality will make it more difficult to preserve Medicare benefits for future generations without crippling taxes. And by overpaying for certain outpatient services and drugs, Medicare significantly distorts the entire health care system today.