Most exchange enrollment is now driven by enrollees choosing plans where taxpayers bear the entire cost, according to new data released last week by the Centers for Medicare and Medicaid Services. As is increasingly clear, the Affordable Care Act (ACA) is more a welfare program that transfers income than a health care program that benefits the middle class. According to CBO, federal subsidies—largely directly deposited into health insurers’ coffers —through the ACA totaled $218 billion in 2023. The vast majority of this was for Medicaid expansion and massive subsidies for people earning less than 150 percent of the federal poverty level (FPL).

The American Rescue Plan Act of 2021 significantly increased premium subsidies to insurers. The subsidy amount limits the premium people must pay for a benchmark plan (the second lowest-cost silver plan), although the subsidy can be applied to any plan. The subsidies are larger for lower-income people. People below 150 percent of the FPL also pay virtually no cost-sharing, including a de minimis deductible, if they select a silver plan.

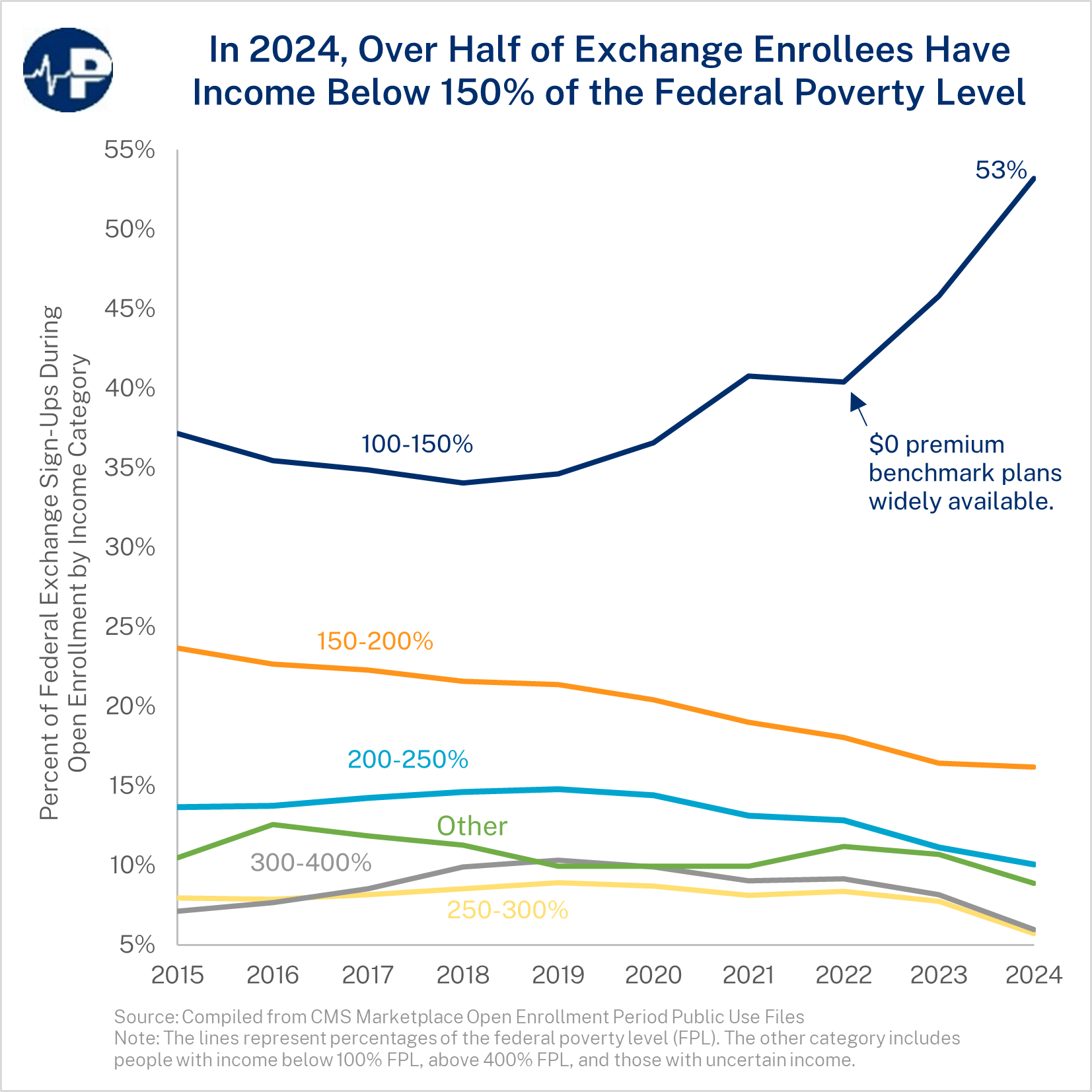

As a result of ARPA, individuals making under 150 percent of the FPL now pay no premium for a benchmark plan, whereas previously, they had to contribute 2 to 4 percent of their income. These increased subsidies substantially increased exchange enrollment. The Paragon pic below shows that new enrollment is coming from people who now pay nothing for coverage because taxpayers foot the entire bill.

In 2019, roughly 35 percent of people who selected a plan during open enrollment had income below 150 percent of the FPL. In 2024, this population accounted for 53 percent of enrollment.

Prior to ARPA, many people below 150 percent of FPL were unwilling to pay the $25 or less per month required to enroll in an ACA plan—a strong sign that they just don’t place much value on the coverage and that the main beneficiaries of the enhanced subsidies are health insurers. As last week’s Paragon pic demonstrated, health insurers’ profits have soared over the past few years with the large ACA subsidies.