On March 23, 2023, Paragon’s Brian Blase testified before the House Committee and Ways and Means Subcommittee on Health to Address why Health Care is Unaffordable.

“Why Health Care Is Unaffordable: The Fallout of Democrats’ Inflation on Patients and Small Businesses.”

My name is Brian Blase, and I was privileged to work for the House Committee on Oversight and Government Reform from 2011 through 2014. You have vital jobs serving the American people, and it is an honor to testify before this Committee today on this important topic.

I am the founder and president of a new health policy think tank—Paragon Health Institute. My testimony today represents my views and not those of Paragon. I am also a visiting fellow at the Foundation for Government Accountability. From 2017 through 2019, I served as a Special Assistant to the President for Economic Policy at the White House’s National Economic Council.

For many people, neither health care nor health coverage is affordable. Counterproductive, illadvised government policies have significantly contributed to high and rising health care prices, costs, and spending. For example, the coverage and benefit mandates in the Affordable Care Act (ACA) significantly increased insurance premiums in the individual market and to a lesser extent, the small group market. According to an analysis by The Heritage Foundation, individual market premiums increased 129 percent on average from 2013—the year before the ACA’s provisions took effect—to 2019.1 The ACA mandates that most significantly increased premiums were rules that expanded the services for what health insurance needed to cover as well as restrictions that prevented premiums from reflecting expected health expenses and produced adverse selection in the market. The ACA, with its complexity and emphasis on accountable care organizations, was designed to increase consolidation in health care markets,2 and consolidation reduces competition and often raises prices, reduces access, and lowers quality of care.3

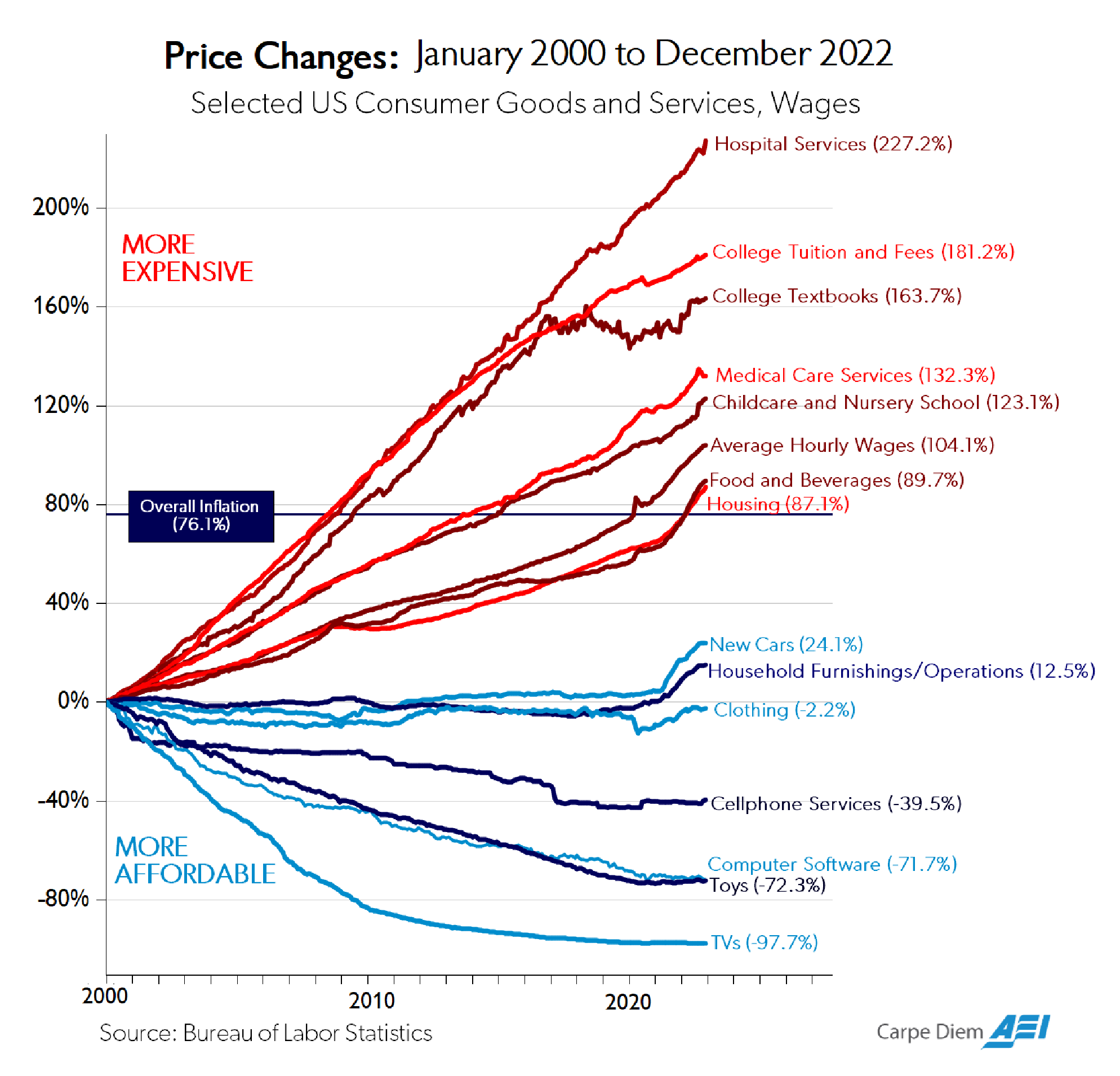

In many areas of the economy, products and services have become higher in quality over time while real prices, after accounting for inflation, have declined (Figure below: “Price Changes”).4 Unfortunately, this has not been the case for most health care products and services.5 As the following figure shows, prices for hospital services—the largest component of health care expenditures—have increased three times faster than general inflation over the past two decades.6

As health costs have risen, insurance premiums have correspondingly soared, even as plan deductibles have risen dramatically. In 2021, health care spending was 18.3 percent of U.S. Gross Domestic Product, a 38 percent increase from the 13.3 percent of U.S. GDP expended on health care in 2000.7 There is also significant waste in the health care sector, with some estimates suggesting that up to a quarter of health care spending provides people with little, if any, health

benefit.8

Importantly, over the past few decades, there have been some noticeable advances in health care, such as a decline in cardiac mortality, improvement in cancer survival rates, a cure for Hepatitis C, and new AIDS treatments. Yet, health outcomes have stagnated despite the Affordable Care Act’s (ACA) new spending and the significant expansion of Medicaid. American life expectancy was lower in 2019 (a pre-pandemic measure) than it was in 2013, before the ACA’s coverage and spending provisions took effect.9

Government Subsidies Contribute to Rising Health Care Prices and Costs

There are many policies—at both the federal and state levels—that raise health care prices and costs. Generally, in most areas of the economy, high prices convey high value. But because of government’s heavy involvement, excessive third-party payment, and generally consolidated markets—high prices in health care are often not a reflection of high value. A major consideration for policymakers in addressing high prices for medical care should be examining how existing government policies contribute to the problem and then focusing on reform.

The federal government—through tax and spending programs—inflates health care spending and is responsible for substantial expenditures that provide little, if any, benefit to Americans. As mentioned above, estimates indicate that up to 25 percent of spending on health care provides no health benefit, with some of it actually harmful, to our health. Reforms are clearly needed, particularly to our health care entitlement programs.

A primary way that government inflates health care prices and costs is through tax and spending policies. In 2021, government health care spending—including both state and local government spending—was 49 percent of total U.S. health care expenditures.10 Federal policy also has a major influence over private sector health care spending, particularly through the tax exclusion for employer-sponsored health insurance. The White House estimated that this tax exclusion will reduce federal revenue—both income and payroll tax collections—by $387 billion in 2023.11

The key economic reality is that when government subsidizes something, that thing becomes more expensive. Subsidies increase demand, raise prices, and thus increase total spending in that area. Substantial and open-ended federal subsidies for health insurance mean that most Americans have comprehensive health insurance. This in turn puts upward pressure on health care prices and diminishes the amount of shopping for health coverage and care.

For complete economic analysis, the taxpayer share of the total cost must be considered. For households to receive subsidies, other households must finance those subsidies. This financing can occur through higher taxes or through greater debt. More debt represents higher taxes in the future, either through direct taxes or higher inflation.

Although the magnitude of government subsidies for health care increases prices and spending, the design of the subsidies is also problematic. Historically, government programs and tax policy have encouraged third-party payment of health services. Thus, for the vast majority of health care transactions, individuals do not directly spend their own money but instead rely on a government program or their insurance plan. Insurance should play a significant role in financing catastrophic and expensive care but having insurance pay for routine and shoppable services rather than relying on markets for these services distorts decision-making and leads to overconsumption and waste.

While inflation in health care services has been substantial, health care services where third-party payment is limited—such as cosmetic surgery and Lasik-eye surgery—have had real price declines as quality has significantly improved.12 Also, a number of physician practices and medical centers, such as the Oklahoma Surgery Center, do not accept insurance and have much lower average prices.13

Disappointing ACA Exchanges

The ACA made individual market health insurance less affordable and introduced a generally inefficient set of subsidies. The ACA expanded coverage in two ways—with a large Medicaid expansion funded almost entirely by federal dollars and with new premium subsidies to help people afford individual market insurance that was made much more expensive because of the ACA’s extensive new federal regulations.

Nearly the entire net coverage gains from the ACA occurred through Medicaid expansion, although many people who gained coverage through Medicaid were, in fact, not eligible for the program.14 Enrollment in the individual market exchanges has largely been disappointing, falling far below original projections. From 2015-2020, exchange enrollment averaged about 10-11 million people15—about 60 percent below what the Congressional Budget Office projected in May 2013 in its last analysis before the ACA’s provisions took effect.16

Low exchange enrollment may be explained by the individual market premiums increasing 105 percent from 2013 to 2017.17 The vast majority of enrollees receive large subsidies as the premium increases have largely priced unsubsidized individuals out of the market.

For the unsubsidized, the average exchange plan annual premium plus deductible for a family of four exceeded $25,000 in 2021 and continues to climb.18 In addition to the high cost, ACA plans tend to have narrow networks, excluding the best hospitals and doctors in local regions. For example, in Texas, not a single ACA plan covers Houston’s world-renowned MD Anderson Cancer Center.19

Misguided ACA Subsidy Expansion

Rather than addressing underlying problems with the ACA that caused high premiums and deductibles and narrow plan networks, the American Rescue Plan Act (ARPA) further increased subsidies for this coverage from 2021-2022. ARPA increased the amount of taxpayer assistance that people receive to purchase exchange plans in two ways. First, it reduced what people with income between 100 and 400 percent of the federal poverty level (FPL) need to pay for a benchmark plan. Second, it lifted the cap on subsidy eligibility at 400 percent of the FPL. The Inflation Reduction Act (IRA) continued the expanded subsidies through 2025.

According to CBO, the enhanced subsidies were the most inflationary part of the IRA and reduce work and economic output.20 The typical exchange enrollee now pays only about 15 percent of premiums, with taxpayers picking up the other 85 percent. Here are half a dozen additional problems.

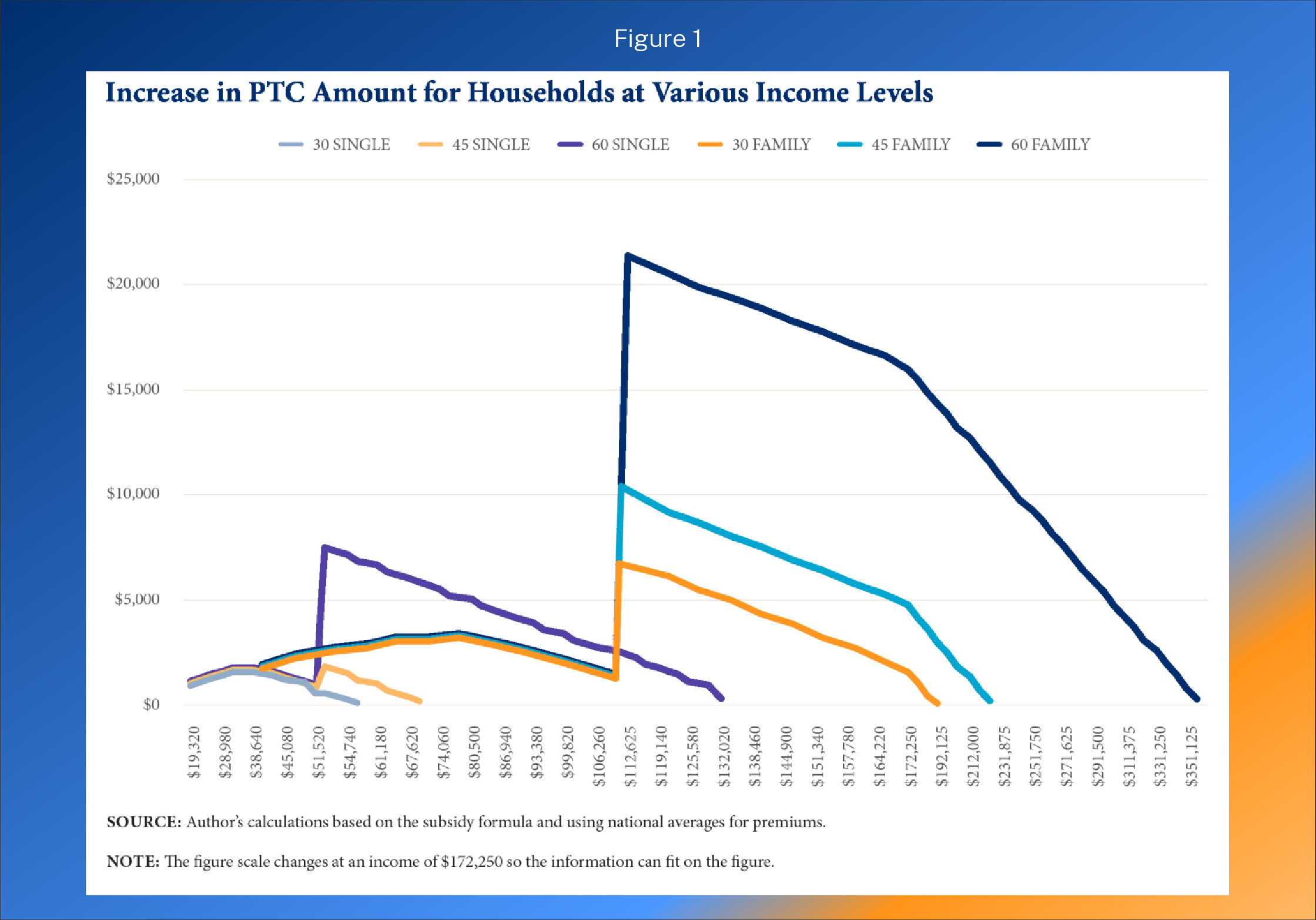

First, as the figure below (taken from a report I authored for the Galen Institute in 2021)21 demonstrates, the relatively wealthy receive far more benefit from the subsidy expansion than lower-income families. The figure shows the benefit in expanded PTCs for six different households at various income levels.

In areas of the country where exchange premiums are high, the expansion of the ACA subsidies leads to extremely high taxpayer subsidies for affluent households. For example, the benchmark premium for an exchange plan in Prescott, Arizona, for a family of five with a 60-year-old household head is $50,923 in 2023.22 A benchmark plan covers 70 percent of a household’s expected health care expenses on average. Of note, the fact that the exchange plan for a family of five can be more than $50,000 a year suggests serious underlying problems with the program.

- If that family made $150,000, they would qualify for a subsidy of $38,173.

- If that family made $350,000, they would qualify for a subsidy of $21,173.

- If that family made $500,000, they would qualify for a subsidy of $8,423.

- This family does not lose subsidy eligibility until they make more than $ 599,000.

Second, the subsidies go directly to health insurance companies, subsidizing their profits even though enrollees may place low value on the coverage and would prefer different health care and health coverage products.

Third, if the subsidies are extended, millions of people will likely lose workplace coverage. This will be especially true of employees at smaller firms since these firms are not subject to tax penalties from the ACA’s employer mandate. In fact, CBO projects that about 3.1 million people will replace private unsubsidized individual market insurance or employer-provided insurance with subsidized exchange coverage.

Fourth, the subsidies are inflationary in their design and will drive up health care prices and health spending, as well as prices throughout the economy.

Fifth, the expansion of these subsidies will likely result in an annual federal spending increase of about $30 billion or more, depending on the extent of employer drop as the subsidies are generally larger than the tax revenue loss associated with the tax exclusion for employer coverage. From a federal budget perspective, employer-sponsored health insurance is the least expensive option on average—only about one-third of the budgetary cost of the other main types of coverage for the non-elderly. According to the Congressional Budget Office, the average federal subsidy per enrollee under 65 is $2,000 for employer coverage, compared to a roughly $5,800 cost for Medicaid and CHIP enrollees and individual market exchange enrollees.23

CBO estimates that making the expansion of subsidies permanent would increase premium tax credits (PTCs) by $305.5 billion from 2023-2032, with a deficit increase of $247.9 billion. (The deficit increase is less than the PTC cost because of higher federal revenues resulting from a shift in compensation from untaxed health insurance to taxable wages.)

Sixth, the projected PTC cost per newly insured is nearly $14,000 a year over the next decade—a high amount that shows that most of the new spending is simply replacing private spending with government spending.

Unlawful and Unwise “Fix” to the So-Called Family Glitch

Another inefficient enhancement of the ACA subsidies is the unlawful expansion of subsidies promulgated through a Biden administration regulatory action to fix the so-called family glitch. I have previously written at length about the unlawful nature of this action as well as the policy problems.24 In sum:

The White House press release for the proposed rule stated that about 200,000 additional people would gain insurance coverage on net if this rule were to be finalized. These two estimates together show that the cost to provide health insurance coverage would be a staggering $225,000 over ten years for just one additional person. This huge cost would result from the rule’s primary economic effect: replacing employer-financed coverage with public subsidies. And of course, the economic burden from taxation, or deadweight loss, would be significant if this rule is finalized— on the magnitude of several billions of dollars of economic loss each year.25

Reforming Federal Health Insurance Subsidies

Policymakers should look for ways to reorient existing expenditures to minimize harmful distortions in the health care market and to expand families’ ability to access affordable health insurance coverage and affordable health care services. A guiding principle for reforming government health financing would be to allow Americans to control more of their own money for health care and coverage rather than to continue to have the government control how most of their money is spent. A guiding principle for reforming government health care subsidies should be to permit individuals and families’ greater control over the resources instead of having the government pay so much directly to insurers for restricted choices of plans.

Grandfathering Existing Enrollees to Expanded Subsidies

A permanent expansion of the enhanced ACA subsidies would increase inefficient health care spending and, in doing so, would exacerbate inflationary pressures in the economy. For the variety of reasons that I discuss above, Congress should not extend the enhanced subsidies. At the very least, a better option than permanently extending the enhanced subsidies would be to permit existing enrollees to keep the enhanced subsidy but prevent new enrollees from receiving it. A grandfathering policy would mean that no one who currently receives an extra subsidy would lose that subsidy, and it would severely limit the harm from a permanent extension—both minimizing employers dropping coverage and reducing the inflationary and deficit-increasing aspects. Nearly half of exchange enrollees have coverage for less than a year, largely because they get jobs and leave the program for employer-provide coverage. Thus, the number of people with enhanced subsidies will rapidly decline over time, restoring the original subsidy design of the ACA.

HSA Option

Last year, Paragon released a policy proposal that would represent a major reform of the ACA subsidy structure.26 Our proposal would permit lower-income exchange enrollees to take a portion of the government subsidy that now goes to health insurers as a health savings account (HSA) deposit instead. Currently, exchange enrollees with income below 250 percent of the federal poverty level quality for a cost-sharing reduction (CSR) subsidy that reduces plan deductibles, cost-sharing amounts, and out-of-pocket limits.

This proposal would significantly expand consumer control over their health care, permitting them maximum flexibility for how to use the government subsidy. Giving lower-income exchange enrollees an additional way to use their CSR subsidy expands Americans’ welfare since some enrollees would prefer an HSA deposit over the reduction of their plans’ cost-sharing components. The HSA funds could be used for a broader set of health services than what a health plan typically covers, help ease family cash flow, accumulate year after year, and better prepare the HSA owner to pay for health care expenses in retirement.

Nearly seven-in-ten enrollees with income below 200 percent of the FPL would benefit from selecting the HSA option, with an average financial benefit of around $1,500 over the year. More than three-quarters of enrollees with income between 200 and 250 percent of the FPL benefit from selecting the HSA option, with a smaller average yearly benefit between $500 and $600.

1332 Waivers

A far more efficient approach than expanding ACA subsidies would be for policymakers to redirect a portion of existing government spending on health care to financing high risk pools or state reinsurance programs. Such an approach, as demonstrated by the 17 states that have used Section 1332 waivers to establish reinsurance programs, would better target federal funds to individuals who have expensive medical conditions or who experience significant spending during a period of time.27

Helping Employers and Workers Obtain Affordable Coverage

Roughly half of Americans receive health insurance through their employer or the employer of someone in their family. Typically, employers offer workers comprehensive health insurance that covers a large number of hospitals and doctors. Workers at large firms often receive several different plans from which to choose, while most workers at smaller firms only receive one plan option.

Employers provide coverage for a variety of reasons, including that it is a tax-free employee benefit. Economists universally agree that employees pay for their health insurance—both the employer and employee shares of the coverage—in the form of reduced wages. This reality means that the rising premiums and overall costs for employer coverage have significantly eaten away at wage increases over this period.

According to the Kaiser Family Foundation’s survey of employers, the average premium for single coverage was $7,911 and the average premium for family coverage was $22,463 in 2022. In 2000, the respective premiums were $2,471 and $6,438. The premium includes both the employee share as well as the employer share; although referred to as the employer share, this amount is paid for by workers in the form of lower wages.

Over this period, premiums for individual coverage increased 220 percent, and premiums for family coverage increased 249 percent—much greater than the 70 percent increase in overall prices during this period.228Although premiums for workplace coverage have increased, the increase in premiums for individual market coverage—which was much more affected by the ACA—rose far more rapidly since 2013.

Premiums for employer coverage increased by about 14 percent between 2013 and 2017, compared to the 105 percent increase in individual market premiums.29 Using 2013 to 2017 is the best period to measure the effect of the ACA on premiums because the ACA’s key provisions took effect in 2014. Additionally, 2017 was the first year without the ACA’s transitional reinsurance and risk corridor programs, which were intended to reduce premiums in the ACA’s transition period.

Since 2010, when the ACA was enacted, there has been a 30 percent decline in the number of workers covered by employer health benefits at firms with between 3 and 24 workers, a 28 percent decline at firms with between 25 and 49 workers, and a 17 percent decline in the number of workers covered by employer health benefits at firms with between 50 and 200 workers.30 While there has been a sizeable drop in employees with employer coverage at small firms, coverage at large firms has only had a slight decline.31

According to the Kaiser Family Foundation’s survey, the number one reason that small employers do not offer coverage is the high cost.32 Among small firms that do not offer health insurance, 79 percent believe employees prefer higher wages to health insurance benefits, compared to only 12 percent who believe employees prefer health insurance.33

Clearly, as premiums have increased, particularly in the individual and small group markets most affected by the ACA, enrollment in private coverage has declined. According to The Heritage Foundation’s analysis of insurance data from the National Association of Insurance Commissioners and Mark Farrah Associates as well as Medicaid data from CMS, the number of people with employer coverage declined by nearly six million from 2013 through 2021.34 Medicaid and CHIP enrollment soared by more than 25 million people during this period.

There are ways to increase affordable health coverage without new federal spending. Many policies implemented by the previous administration expanded affordable coverage options for employers and families without new federal spending.

These policies included:

- expanded coverage options through Association Health Plans (AHPs)

- new flexible financing methods through individual coverage health reimbursement arrangements (HRAs) which built off qualified small employer health reimbursement arrangements (QSEHRAs), and

- price transparency policies intended to improve the functioning and efficiency of health care markets.

Association Health Plans (AHPs)

All employers—especially small employers—need additional options to provide coverage to their workers. One such option is to permit employers to band together to offer coverage through Association Health Plans. While AHPs have existed for decades, employers needed to have a close nexus in order to join together and offer coverage. For example, dental practices could form an AHP, but a dental practice and an auto mechanic shop in the same town could not.

In June 2018, the Department of Labor finalized a rule creating a new pathway for any employer, including sole proprietors, within a state and or common metropolitan area to join together and offer coverage through an AHP. This rule provided smaller employers a way to gain the regulatory advantages and economies of scale that large employers receive when offering health insurance.

As discussed in a Washington Post piece from early 2019, the AHP expansion had a promising start with most new AHPs launched by regional chambers of commerce.35 According to the Washington Post, “there are initial signs the plans are offering generous benefits and premiums lower than can be found in the Obamacare marketplaces.”36 The Post wrote that an analysis of the new plans showed they offered benefits comparable to most workplace plans and did not discriminate against people with preexisting conditions.37 A study by the Foundation for Government Accountability found that new AHPs produced savings of 29 percent on average.38 One local chamber of commerce that enrolled hundreds of employers was projected to save policyholders more than $2,000 on average.39 The Congressional Budget Office projected that these new AHPs would cover as many as 4 million people by 2023, half a million of whom would have been uninsured.40 Unfortunately, a March 2019 decision by a federal judge invalidated this new pathway.41 Although the Department of Justice appealed this decision and the appellate court heard arguments in November 2019, the court granted the Biden administration’s motion to pause the appeal while the DOL considers further agency action.

Given the litigation challenges and the Biden administration’s apparent opposition to AHPs, congressional action is likely necessary for businesses to benefitfrom the new AHP pathway. As projected by CBO, these new AHPs would help hundreds of thousands of businesses and millions of employees obtain more affordable health coverage and would reduce the number of uninsured. This increase in health coverage would involve no new federal spending.

ICHRAs and QSEHRAs

In June 2019, the Departments of Health and Human Services, Labor, and the Treasury issued a rule creating individual coverage Health Reimbursement Arrangements (ICHRAs). Like AHPs, ICHRAs should be bipartisan. They work within the ACA’s basic framework and should significantly increase individual market enrollment.

As of January 1, 2020, employers have been able to provide tax-preferred contributions through an ICHRA, which their employees can use to purchase the individual market plan that work best for them. Most employers that offer health insurance only provide workers with a single option, so the HRA rule has the potential to significantly increase worker choice and control over their health insurance. Employees are currently limited to purchasing ACA- compliant plans in the individual market, although Congress could permit employees to use their HRAs to purchase a broader set of plans.

ICHRAs will help employers attract and retain employees, gain greater predictability over their health costs, and reduce administrative expenses, allowing them to better concentrate on their core business purpose. The rule should help reverse the decline in small employers that offer coverage to their workers. Moreover, the rule contains significant flexibilities for larger employers to offer coverage to part-time workers or hourly workers.

According to estimates provided in the June 2019 rule, 800,000 employers will offer ICHRAs, and more than 11 million people will receive individual market coverage using this type of HRA by the middle of this decade.42 This rule is expected to reduce the number of people without health insurance by about one million.43 According to the Departments’ analysis, “Most of these newly insured individuals are expected to be low- and moderate-income workers in firms that currently do not offer a traditional group health plan.”44 Similar to AHPs, the increase in insured people through ICHRAs involves no new federal spending.

ICHRAs have similarities to Qualified Small Employer Health Reimbursement Arrangements (QSEHRAs), which Congress enacted in a bipartisan basis in 2016. QSEHRAs permit employers with no more than 50 full-time employees to reimburse individual market premiums. QSEHRAs have some limitations that do not apply to ICHRAs, such as setting an overall limit on the amount the employer can reimburse as well as a prohibition of creating classes of employees to vary benefit offerings. However, QSEHRAs represent a valuable coverage option for many small businesses and their employees.

Congress could codify the 2019 HRA rule to enhance employers’ certainty about the future of defined contribution health insurance. Policies that improve the individual market would boost the opportunity for employers and employees to benefit from ICHRAs. One such policy would be to permit states greater flexibilities over benefit requirements and pricing, such as widening the three-to-one age rating restriction in the ACA. There is not yet good data on the uptake of ICHRAs, and there is a lot of education needed to ensure that employers and brokers understand them. Moreover, migration to ICHRAs has been affected by employers’ understandable focus on weathering the pandemic as well as a general risk aversion to changing employee benefits in such a tight labor market.

Price Transparency

In 2019, HHS finalized a rule requiring hospitals to post complete price information starting in 2021. In 2020, HHS with the Departments of Labor and Treasury finalized a separate rule that requires health insurers and health plans to post complete price information starting this year.

Price information can enable both individual consumers as well as employers to be better shoppers of health care. Price information is particularly important in health care because it is a large part of the typical families’ budget and because there is significant variation in prices— with prices for the same service often varying by magnitudes, even within the same geographic area.

I analyzed these requirements and their potential impact in a 2019 report.45 Expanded price transparency should result in five benefits.

- First, price transparency will encourage more consumers to shop and obtain lower prices.

- Second, price transparency will help employers establish better payment structures. These payment structures include reference pricing models, in which the plan sets a payment rate regardless of which provider delivers the service and which have been shown to generate significant savings.

- Third, price transparency will better enable employers to monitor the effectiveness of their insurers by comparing different rates received by providers across payers and across regions.

- Fourth, transparent prices should help employers eliminate counterproductive middlemen and contract with other entities that will incentivize employees to utilize lower-cost providers, including ones outside of their local region.

- Fifth, just as sunlight is often the best disinfectant, price transparency will better enable consumers and the broader public to hold providers accountable when prices reach outrageous levels.

Disappointing Health Benefits from Government Coverage Expansion

While access to affordable health coverage and care are important, it is vital for policymakers to recognize two key facts. First, a large amount of medical spending is wasteful—with some of it even harmful to patients. Second, health insurance expansions, particularly through government programs such as Medicaid, tend to have disappointing results in terms of health improvements.

A significant concern with our high medical spending is that a large share of it—estimated by some researchers to be 25 percent of spending as mentioned above—does not provide Americans with any benefit.46 In fact, some of that spending may instead harm our overall health. A 2016 study found that medical errors are the third leading cause of death in the United States and as many as 250,000 people die each year from errors in hospitals and other health care facilities.47 Medical tests and treatments all carry some risk. Those that are unnecessary will result, on balance, in harm to patients.48

The impact of health insurance on health is not as clear or as positive as commonly believed. At a macro level, despite the significant increase in health coverage beginning in 2014 as a result of the ACA, American life expectancy declined for three straight years from 2014 through 2017.49 The 2018 Economic Report of the President by the White House’s Council of Economic Advisers (CEA) put it this way:

[T]he evidence shows that health insurance provided through government expansions and the medical care it finances affect health less than is commonly believed. Determinants of health other than insurance and medical care—such as drug abuse, diet and physical activity leading to obesity, and smoking—have a tremendous impact and have exacerbated recent declines in life expectancy, despite the ACA’s increased coverage.50

The CEA report evaluated numerous studies, including the two well-known health insurance experiments—the RAND health insurance experiment and Oregon’s Medicaid experiment—in its conclusion that expansions of government coverage produce limited health benefits. They suggest at least four reasons why health insurance, through government coverage expansions, have a minimal effect on health.

According to the report, “The first three of these reasons—that the uninsured were often able to obtain care before coverage, access problems for patients who gain Medicaid coverage, and mandated insurance benefits that have a minimal impact on health—are particularly salient when examining the results of the ACA coverage expansion.”51

The fourth reason raised by CEA is that “public coverage may have limited or possibly negative effects on health because of its long-run impact on innovation. Many governments, particularly in Europe, have paired large coverage expansions with the imposition of price and spending controls. These centralized controls may have an adverse impact on medical innovation and make healthcare less effective and more costly to obtain in the future.”52

The lack of clear health benefits from the expansion of Medicaid, which I detailed in a report released in the spring of 2020, should raise policymakers’ concern about additional subsidies that simply expand government spending on the current structure.53 I concluded that large coverage expansions disappoint for several reasons: the uninsured receive nearly 80 percent as much care as similar insured people, the crowd-out of potentially superior private coverage, and the indirect effects on others such as longer wait times for care.

Furthermore, the ACA’s model of subsidization results in direct payments from the government to health insurance companies. A 2018 report from the Council of Economic Advisers found that health insurer profitability had soared—more than doubling the growth of the S&P 500 in the first four years of the ACA’s enactment.54 Both the design of the ACA’s premium subsidies as well as the ACA’s Medicaid expansion were inflationary and resulted in high payments to health insurance companies. There have been a variety of news stories documenting how these programs that are intended to benefit lower-income Americans have produced windfall profits for health insurance companies.55

Adverse Consequences of New Government Price Controls for Pharmaceuticals

One of the few constraining factors on increasing health costs in recent years has been innovation.56 For example, the inflation measure for prescription drugs shows that drug prices have been relatively flat while overall prices have soared.57 Yet it was in this environment that lawmakers enacted sweeping new powers for the Secretary of Health and Human Services to set pharmaceutical prices and impose penalties on manufacturers that raise prices faster than inflation. These provisions will increase launch prices, make it harder for generics to come to market, and reduce the incentive for innovators to bring new drugs to market.58 According to University of Chicago economist Tomas Philipson, who was the chairman of the White House Council of Economic Advisors from 2019-2020, the pricing provisions in the Inflation Reduction Act (IRA) will significantly reduce the number of new drugs, lowering both the quality and longevity of Americans’ lives.59

Conclusion

Renowned health economist and Harvard Business School professor Regina Herzlinger has written that “choice supports competition, competition fuels innovation, and innovation is the only way to make things better and cheaper.”60 Unfortunately, government policies—despite good intentions—often stifle choice, competition, and innovation in health care. Furthermore, these programs and policies produce incentives that lead to waste ratherthan value in our health care expenditures.

- Government mandates have pushed up the price of insurance. The high price of insurance necessitates large subsidies, so people can afford the coverage.

- Government restricts people from buying coverage that works best for them and prevents small employers from joining together to gain the same advantages that large employers obtain in their coverage.

- Government contributes to higher health care prices and overall inflation with poorly designed subsidies.

Although increasing subsidies may be tempting, expanding inefficient health care subsidies makes health care less affordable. Government spending replaces private spending that would have otherwise occurred. Government subsidies often permit insurers to raise premiums with taxpayers on the hook for the higher premium cost. The subsidy cost of nearly $14,000 per newly insured from the expansion of exchange premium subsidies by the American Rescue Plan Act and Inflation Reduction Act is testament to this inefficiency. Two main subsidy reforms I presented above would be permitting the enhanced PTCs to expire after 2025 and permitting exchange enrollees to receive their cost-sharing reduction subsidy as an HSA deposit.

Fortunately, by reforming existing government programs and pursuing policies that promote choice and competition in health care, policymakers can expand access to affordable health coverage without new government spending.

The following policies, if fully implemented, would help millions of families, and reduce the number of uninsured by a projected two million people—all without any new federal spending:

- Association Health Plans, which offered significant savings to small employers for highquality coverage.

- Individual coverage health reimbursement arrangements, which permit employers a way to provide health coverage in ways that employees may prefer.

- In addition to the expansion of coverage opportunities, new price transparency rules that are properly implemented can improve the functioning of health care markets and expand opportunities for consumers and employers to maximize value from their expenditures.

Lastly, policymakers should avoid centralized regulatory or price controls that would diminish health care innovation. Rather policymakers should pursue policies that create a climate conducive to innovation in which entrepreneurs are best serving patient needs. Thank you for the opportunity to testify before the Committee today, and I look forward to your questions.

The following clips feature Dr. Blase before the House Ways and Means Committee.

https://youtu.be/FmiDp74jZ0U