Brian Blase, Ph.D.

Brian Blase, Ph.D., is the President of Paragon Health Institute. Brian was Special Assistant to the President for Economic Policy…

Reforming Government, Empowering Patients

Navigation

This paper proposes allowing Americans to allocate a portion of their ACA subsidy to health savings accounts (HSAs), arguing this option enhances consumer choice, control, and welfare by providing more equitable tax treatment and incentivizing cost-effective healthcare spending.

The Affordable Care Act (ACA) shortchanges enrollees by restricting choice and control over their health care decisions and spending. The ACA has generally led to plans with high cost-sharing, including deductibles, and restricted networks of providers and facilities that the plans will reimburse.1 By contrast, tax-free health savings accounts (HSAs) are powerful tools that give patients more choice and control over their personal health care decisions. HSAs also make the tax treatment of health care more equitable and help reduce overall health care costs by creating enrollee incentives to maximize value from their health care expenditures.2

In this paper, we propose a new option through which many ACA exchange enrollees could accept a deposit to an HSA instead of a reduction in their plan’s cost-sharing requirements through the cost-sharing reduction (CSR) program. Currently, insurers must reduce plan cost-sharing for certain lower-income exchange enrollees. In 2020, more than 5 million lower-income households received benefits from the CSR program. Under our proposal, insurers that offer exchange plans would be required to offer those enrollees an HSA-qualified plan with an HSA deposit as an alternative option.

For most people, the HSA option would enhance their overall welfare. Many enrollees with incomes below 200 percent of the federal poverty level (FPL) would have access to sizeable HSAs deposits each year if they selected the HSA option. According to analysis from Milliman, an independent risk management firm with expertise in health care financing, nearly seven-in-ten enrollees with income below 200 percent of the FPL would benefit from selecting the HSA option, with an average financial benefit of around $1,500 over the year.3 More than three-quarters of enrollees with income between 200 and 250 percent of the FPL benefit from selecting the HSA option, with a smaller average yearly benefit between $500 and $600.4 Importantly, the HSA funds could be used for a broader set of health services than what a health plan typically covers, help ease family cash flow, accumulate year after year, and better prepare the HSA owner to pay for health care expenses in retirement.

Most ACA plans today are relatively narrow-network health maintenance organizations (HMOs), which provide no coverage for out-of-network services. The HSA option would provide enrollees in these restrictive plans with greater financial protection since enrollees could use HSA funds for any qualified medical expense—a much broader set of services and treatments than what their HMO would cover.

To optimize the HSA option, Congress would also appropriate CSR funding and prohibit “silver loading,” thereby replacing the indirect CSR subsidies under current law with direct ones.5 These appropriations would include reimbursement for insurers’ HSA deposits.

Based on past scores from the Congressional Budget Office, the combination of the HSA option, a CSR appropriation, and a prohibition on silver loading should simultaneously expand coverage and reduce deficits—a rare feat. It would also increase the efficiency of health spending because consumers would have more control and greater incentive to obtain value. Finally, systemwide health benefits would accrue as providers would need to be more responsive to the demands of consumers.

The health savings account (HSA) option has eight components.

1. Enrollees who are eligible for the CSR program will have the option to enroll in an HSA-qualified plan that offers an HSA contribution.

Currently, the cost-sharing reduction (CSR) program (described in the text box below) requires plans to reduce cost-sharing and out-of-pocket limits for silver plan enrollees with income between 100 and 250 percent of the federal poverty level (FPL). This proposal does not repeal CSR payments but rather expands options for consumers on the exchanges to obtain the government subsidy in a way that best meets their preferences. Enrollees will be free to select an HSA-qualified plan with a partially funded HSA, or in some cases a fully funded HSA, instead of a silver plan with cost-sharing reductions. Many enrollees will be better off with this option, which will be particularly attractive to those who want greater control over their health care and greater ability to save for future health care expenses.

At least 5 million individuals could benefit since more than 5 million people received CSR payments in 2020.6 This number is a conservative estimate because some lower-income people who are not currently enrolled in an exchange plan would do so given the attractiveness of the HSA option. In fact, our proposal would likely decrease the number of people without health insurance by at least several hundred thousand.7

2. Enrollees need not already have an HSA account to participate; they may establish one upon choosing the option. The exchange and the participating insurer, under U.S. Department of Health and Human Services (HHS) and Internal Revenue Service (IRS) guidance, will provide enrollees with useful information about how to establish and properly use an account.

Low-income households are less likely to have HSAs than middle-income or high-income households.8 This proposal allows exchange plan enrollees who are eligible for the CSR program to establish an HSA when selecting an HSA-qualified plan, which will enable consumers to choose to use a portion of the ACA subsidy to obtain funds for out-of-pocket health care purchases and to build savings for future health care expenses. For most enrollees, it will likely be their first time saving for health care using pretax dollars. Many insurers currently help individuals enrolled in an HSA-qualified plan to establish an HSA. For more information on HSAs, see the appendix.

3. An insurer offering plans on an ACA exchange will be required to offer a plan with an HSA option and an associated contribution for each of the actuarially equivalent plans required by the CSR program.9

Current law requires insurers participating in the ACA exchanges to reduce cost-sharing obligations for enrollees who have income between 100 and 250 percent of the FPL. Our proposal requires insurers to also offer actuarially equivalent HSA-qualified plans with HSA contributions.10

Having the option of an HSA-qualified plan with an account deposit expands consumer choice and permits people to obtain higher value from the federal subsidies for exchange plans. There are several advantages to a funded HSA relative to the current structure:

4. HSA deposits count against the annual HSA contribution limits.

Enrollees in this option would be subject to the standard HSA contribution limits under current law.14 For example, if an enrollee received an HSA contribution from his insurer of $1,000 in 2023, he could personally contribute additional funds up to the 2023 limit of $3,850 (i.e., an additional $2,850).

5. The insurer will make a monthly prorated HSA deposit to the qualified enrollee’s account.

Ideally, enrollees would have access to the full HSA deposit at the beginning of the plan year since medical expenses can be unpredictable. However, many people are enrolled in an exchange plan for only a few months each year, and allowing an annual, full deposit at the beginning of the year raises complex implementation and compliance issues. Thus, our proposal is simple: for each month that an individual who has selected the HSA option is enrolled in an exchange plan and qualifies for the CSR program, the insurer must make a prorated HSA deposit.

6. The enrollee may access the HSA account only with a bank-issued debit card that ensures the funds are used only for qualified medical expenses.

To prevent enrollees from using their HSA funds for nonqualified expenses, they would be required to use a bank-issued debit card for purchases from the HSA. The card issuer must restrict the card’s usage at the point of sale, specifically at the product SKU code level. Some banks currently offer such restricted cards for customers to help prevent nonqualified purchases and cash withdrawals, whether intentional or accidental. As one bank representative explained the process, “The card scans the SKU and can reject a purchase immediately. Say you are at the pharmacy buying an Rx [prescription] and a bottle of wine. It will pay for the Rx but reject the wine and ask for additional payment.”15 As an additional protection, policymakers may wish to require that card usage be restricted by merchant code (MCC); doing so would ensure that the card could never be used at a bar, restaurant, or casino.

7. HSA deposits are subject to end-of-tax-year reconciliation and recapture rules by the IRS.

Since participants in the HSA option would be receiving premium tax credits (PTCs) they would be required to file a tax return.16 Reconciliation and repayment rules are necessary when providing advance payments of tax credits like the ACA’s PTCs and the expanded version of the Child Tax Credit, and such rules are appropriate here as well. Similar to how reconciliation works with advance PTCs, HSA deposits would be made up front and then reconciled after the year when household income is reported. Similar limits would apply to the amounts that could be recaptured. If Congress appropriates CSRs as we suggest, the recapture and reconciliation process between the HSA option and the CSR option should be equivalent for enrollees. Money lawfully still in the account following reconciliation would be the enrollee’s property and automatically roll over to the following year—the same as what happens with any other HSA.

8. HSA-qualified plans will adhere to IRS requirements regarding minimum deductibles, annual out-of-pocket limits, and coverage requirements.

Our proposal would adhere to HSA rather than ACA cost-sharing rules. Doing so could benefit enrollees, because the maximum out-of-pocket limit for HSA-qualified plans is currently lower for individuals and families than the out-of-pocket limits for ACA exchange plans.17 An HSA-qualified plan with an HSA contribution could have a lower out-of-pocket limit than a non-HSA plan with the cost—sharing reductions from the CSR program.

Giving lower-income exchange enrollees an additional way to use their ACA subsidy expands consumer welfare since some enrollees would prefer an HSA deposit over the reduction of their plans’ cost-sharing components. About seven-in-ten enrollees benefit from selecting the HSA option. A typical enrollee (one with income between 150 and 200 percent of the FPL) would benefit by about $1,400 each year.

This proposal has broader societal benefits as well. First, the HSA option should help facilitate transitions to more stable employment at higher wages. With the security of a funded HSA, some workers may be more likely to accept a job from an employer that offers coverage with a standard cost-sharing structure, knowing that the HSA balance can pay for cost-sharing requirements.

Second, the HSA option should improve the value of health spending and increase price competition in the market. Since people will be spending their own resources from their HSA, they will have a greater incentive to ensure that the health care they receive is worth the cost. Seeking to protect their HSA balances, patients will be incentivized to receive regular primary care and avoid unnecessary and costly emergency room visits. Providers will have to compete more for consumer dollars and thus will have an incentive to improve their efficiency and effectiveness in delivering care.

In 2020, 50 percent of ACA exchange plan enrollees were enrolled in a CSR plan. In such plans, the insurer is required by the government to reduce out-of-pocket expenses, including deductibles, co-payments, coinsurance, and maximum out-of-pocket limits.18 To receive CSR payments, an individual or family must be enrolled in a silver plan on the exchange, must be receiving a PTC, and must have income no greater than 250 percent of the FPL.19

The amount of the benefit from the CSR program is a function of household income—households with income between 100 and 150 percent of the FPL receive the most assistance, and households with income between 200 and 250 percent of the FPL receive the least assistance.

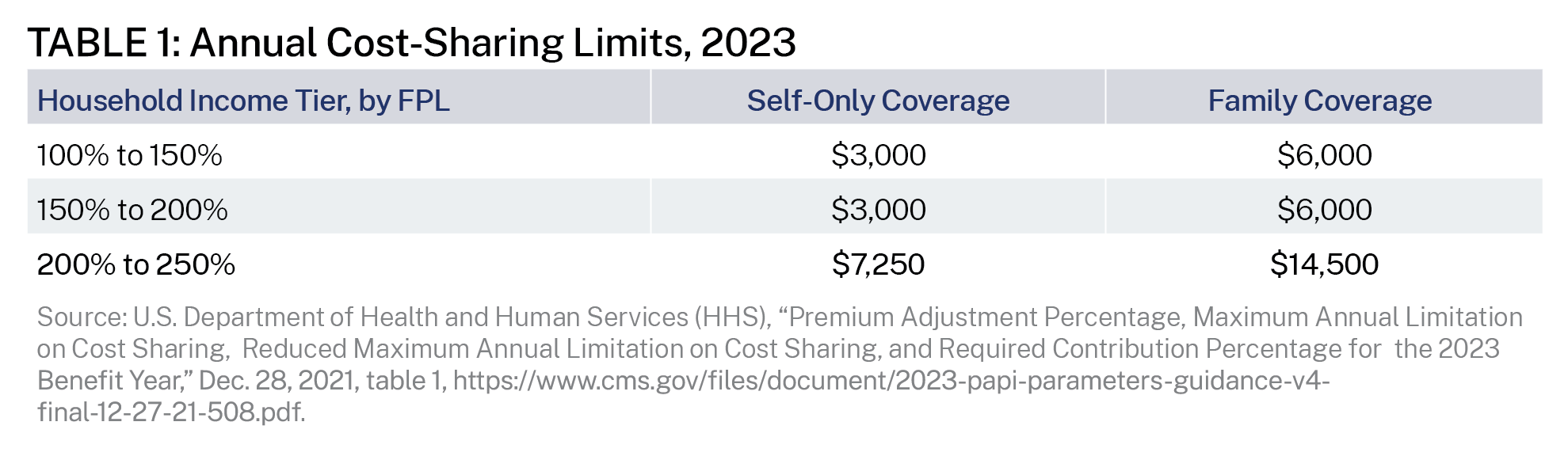

Technically, there are two steps of the CSR program. Step one reduces maximum out-of-pocket limits. The ACA caps the amount of annual cost-sharing for covered in-network services for all ACA-compliant plans. For 2023, the annual cost-sharing limit for self-only coverage is $9,100, and the limit for family coverage is $18,200.20 As shown in table 1, the first CSR step reduces these amounts, which limits the maximum annual financial obligations that households would face for covered health care expenses.

The second CSR step increases insurers’ share of health care expenses and reduces the cost-sharing amounts, including deductibles for individuals and families—effectively increasing the plan’s actuarial value (AV). For households that benefit from CSR payments, the cost-sharing of a 70 percent AV silver plan must be reduced so that the AV increases to:

The ACA authorizes payments to insurers to compensate them for the increased expense associated with shifting a portion of claim costs from enrollees to plans as well as for the expected further increase in claim costs attributable to greater consumption when enrollee cost-sharing is reduced (i.e., induced demand). However, the ACA did not provide financing for such payments. Despite the lack of an appropriation, the Obama administration made payments to insurers for CSRs. The House of Representatives filed suit in 2014, claiming the payments violated the appropriations clause of the U.S. Constitution, which provides that “no money shall be drawn from the Treasury but in consequence of appropriations made by law.” The U.S. District Court for the District of Columbia agreed with the House, finding that the Obama administration’s payments for CSRs were unconstitutional since there was not a valid congressional appropriation. After conducting its own review, the Trump administration terminated federal payments for CSRs in October 2017. As of this writing, the federal government has not provided direct reimbursements to insurers for CSRs since fiscal year 2017.21

Silver Loading

Since the loss of CSR payments from the government, health insurers—who are still legally obligated to provide cost-sharing reductions—responded by increasing premiums for silver plans, a process now referred to as “silver loading.”22 Since the PTC is a function of the second-lowest-cost silver plan, health insurers recouped the loss of CSRs through higher premiums.

According to the Congressional Budget Office (CBO), silver loading has resulted in a net increase in federal spending because the growth in PTC payments has exceeded the foregone CSR subsidy payments.23 In a 2018 analysis, CBO projected that a congressional CSR appropriation would reduce federal deficits by $29 billion over the 2018–2027 period, mainly from smaller federal subsidies for health insurance for people with income between 200 and 400 percent of the FPL.24 CBO also projects that prohibiting silver loading would reduce premiums for people who do not qualify for PTCs.

Finally, in response to insurers’ appeals on CSR payments, the Federal Circuit Court of Appeals concluded that insurers were “entitled to recover unpaid cost-sharing reduction (CSR) payments that the Trump Administration withheld, but only to the extent insurers had not recouped their losses through higher premiums.”25

The CSR program has always resulted in payments from the U.S. Treasury to health insurers. Under the Obama administration, the payments were direct. Under the Trump and Biden administrations, they have been indirect, through higher PTCs. Under both approaches, the insurer is the recipient of the federal subsidy.

The ACA created subsidies for people without eligibility for another government program and who lacked an offer of affordable employer coverage to purchase coverage in the individual market.26 (The subsidy structure is explained in the appendix.) However, these subsidies are not an efficient use of taxpayer dollars, in part because much of the subsidy expenditure simply replaces private spending with government spending. Given the government’s large share of the plan costs, enrollees have little incentive to make value-based, cost-conscious decisions. The ACA’s subsidy structure is also inflationary, raising overall premiums as well as prices.27 Moreover, there are economic losses from the excess burden of taxation necessary to finance these subsidies.28

Under our proposal, an insurer could meet its requirements under the CSR program by partially funding an enrollee’s HSA associated with an HSA-qualified health plan. Our proposal would give the enrollee control over the resources, unlike the CSR program in which the insurer makes decisions about how to reduce plan cost-sharing amounts. The amount of HSA funding and the other plan design elements should be structured to maximize the HSA funding while still meeting the AV requirements of the CSR program.

While the ACA subsidies are fundamentally flawed, the proposed HSA option would be a significant improvement over the current structure by allowing millions of consumers to choose a different way to structure their ACA subsidy. Specifically, this choice would permit consumers to direct a portion of the subsidy into an account that allows them to use the funds for health care expenses in ways that work best for them.

The ACA subsidy design does not permit enrollees to maximize their preferences by choosing the types of plans and the mix of premium and out-of-pocket expenditures that most appeal to them. Instead of being constrained by the ACA’s rigid cost-sharing rules, enrollees may prefer to control the money they spend on out-of-pocket health care services using an HSA.

Another benefit of the HSA option is that it provides liquid assets to cover cost-sharing obligations. Some enrollees would likely have an option in which the HSA deposit entirely covers the plan deductible. Many households do not have enough money on hand to pay cost-sharing in typical private health plans. For example, in one recent survey, 45 percent of single-person nonelderly households indicated they could not afford to pay more than $2,000 from current liquid assets, and 63 percent could not pay more than $6,000.29 Lower-income households were even much less likely than other households to have the liquid assets needed to meet typical cost-sharing obligations. HSA funds can help fill that gap.

In addition to being able to save money through the HSA for future health expenses, one of the main benefits for people with HSAs is that they can use the account in the present year to pay for any qualified medical expense. While this includes cost-sharing amounts for services and treatments covered by their plan, it also includes expenses that may not be covered by their plan.

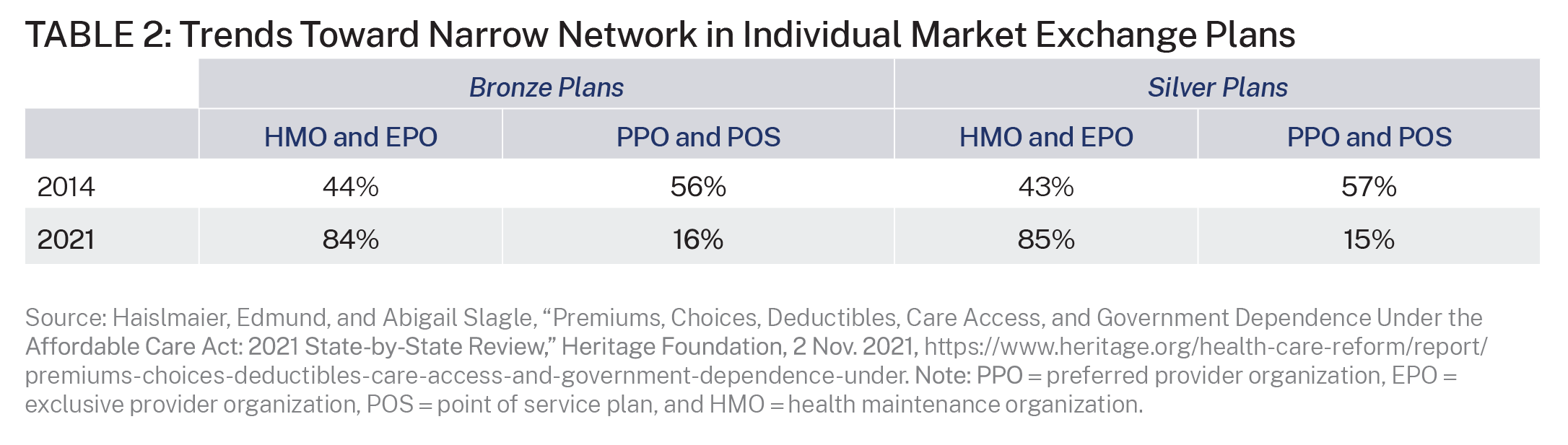

The HSA option expands consumer financial protection against out-of-network expenses. Since most exchange plans employ narrow, restrictive provider networks, this feature of HSAs is particularly useful for exchange plan enrollees. Table 2 shows the trend toward narrow network plans in the exchanges. In such plans, the consumer is fully responsible for out-of-network medical expenses. HSAs provide consumers with risk protection from unexpected costs of receiving accidental or unintentional out-of-network services.

The HSA option would give enrollees greater resources for their future. Most Americans spend little on health care each year. Roughly 14 percent of the population had no health expenditures in 2019.30 Half of the population accounts for only 3 percent of all health spending, with average spending for this group of just $374 per person in 2019.31 Extrapolating from these facts, about half of Americans have health expenses below $1,000 each year. Thus, for most enrollees, the HSA option will enable them to save for the future as the balance of their HSA grows. Assuming a real interest rate of 6 percent and annual net HSA contributions of $1,500, the amount in the account would equal about $55,000 after twenty years, $119,000 after thirty years, and $232,000 after forty years. Such savings would lead to significant financial resources to reimburse health care expenses that occur later in life.

To anticipate how the HSA option would work, we modeled four different silver plans using varying combinations of deductibles, coinsurance, and out-of-pocket limits, while satisfying the AV requirements for CSR plans. The CMS AV Calculator for 2023 was used for the modeling.32 The calculator allows the user to vary plan features, such as deductibles, coinsurance, out-of-pocket limits, and HSA contributions. The regulations permit the plan AV to vary within de minimis ranges from the specified AV requirements. The calculator does not account for the age of the enrollee.

The results are displayed in Tables 3 and 4 for three income groups:

For convenience in this section, we will refer to these groups as the “highest,” “middle,” and “lowest” income groups, respectively.33

We derived the tables using a modified version of the 2023 CMS AV Calculator, after consultation with actuaries from Milliman. The calculator shows the expected percentage of member expenditures on essential health benefits made by the plan, based on a variety of plan designs.

The current CMS AV calculator provides for the value of a health reimbursement arrangement (HRA) but not an HSA, meaning that the amount unspent in the year of the contribution is foregone in the original calculator. HSA contributions, including those under our plan, remain with the individual past the plan year and until they draw down the value of the HSA contribution. Thus, it was necessary to adjust the calculator to reflect our proposal’s reliance on HSAs rather than HRAs. Milliman produced a modified AV Calculator that values HSA contributions as a full paid benefit, rather than a benefit that is limited to a percentage that would be spent on cost-sharing for essential health benefits during the year.34

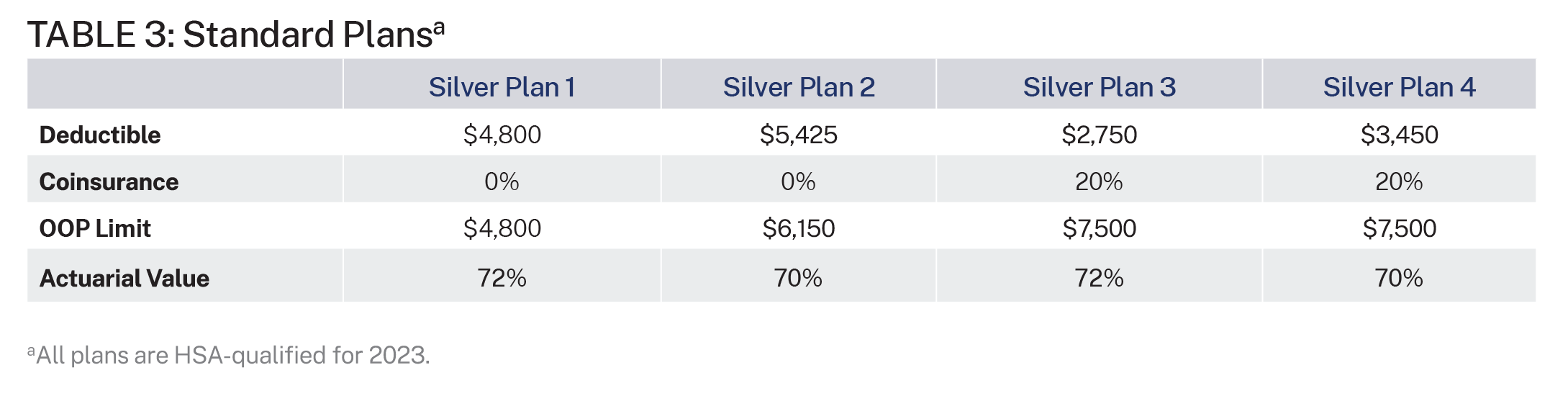

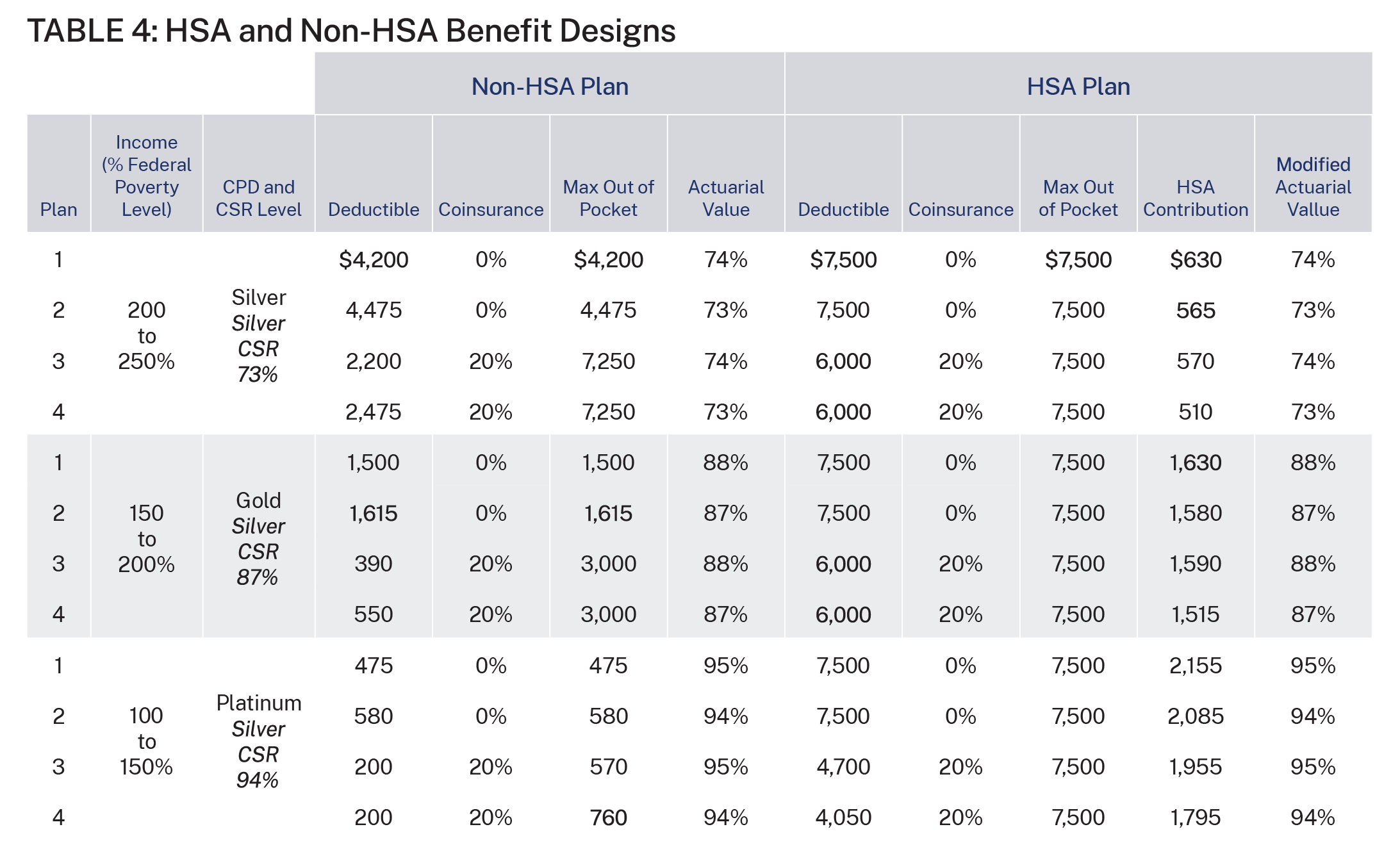

Table 3 shows the status quo and includes four standard HSA-qualified plans that an insurer could offer in the silver metal tier today without the proposal. None of these four plans includes an HSA contribution from the insurer. These plan designs are examples of many possible designs.

Table 4, which is reproduced from Figure 4 in Milliman’s report, shows the comparison between the CSR plan (i.e., the non-HSA plan) and the HSA plan.35 Using four different plan options (with varying deductible, cost-sharing percentages, and out-of-pocket limits), the non-HSA plan columns show the reduced plan deductibles and out-of-pocket limits to meet the AV requirements of the CSR program. Of note, none of the CSR plans for the lowest-income category are HSA-qualified since the deductible is below the required minimum deductible for HSA plans and plans 3 and 4 with the lower deductible and 20 percent coinsurance for the middle-income group are not HSA-qualified.36

The right-hand columns in Table 4 show alternative plan designs that include an HSA-qualified plan with the maximum possible HSA contribution instead of reduced cost-sharing.

These HSA contributions are the amounts that Milliman’s modified CMS AV calculator indicates would provide a similar AV to the plans under the CSR program.37 For the highest-income group, the HSA contributions would be relatively modest because the CSR program only increases the AV of these plans from 70 percent to 73 percent. The contributions are much more robust for the lowest- and middle-income groups because the CSR program requires insurers to raise the plan AV to 94 percent and 87 percent, respectively.

The annual benefit of the HSA option, compared to the CSR plan under current law, equals the amount of the HSA deposit until total spending equals the CSR option deductible. Until that spending amount, the individual is paying out of pocket under both plans. After that amount, the benefit of the HSA option begins to decline dollar for dollar since the enrollee would no longer have any out-of-pocket payments under the CSR plan and would bear the cost of additional plan spending under the HSA plan. This decline occurs until annual spending equals the deductible for the HSA option.

For example, enrollees in the middle-income group who choose plan 1 would be eligible for an HSA deposit of $1,630. Since this plan has no coinsurance, the tradeoff they face for choosing the HSA plan instead of the CSR plan is a higher deductible. The HSA plan carries a $7,500 deductible, much higher than the $1,500 deductible of the CSR plan. This individual is clearly better off with the HSA plan if he has less than $3,130 of health expenses in that year (his HSA contribution plus the deductible for the CSR plan). In reality, the individual’s true out-of-pocket limit for the HSA plan would be only $5,870—the difference between that plan’s maximum out-of-pocket limit and the HSA contribution.38

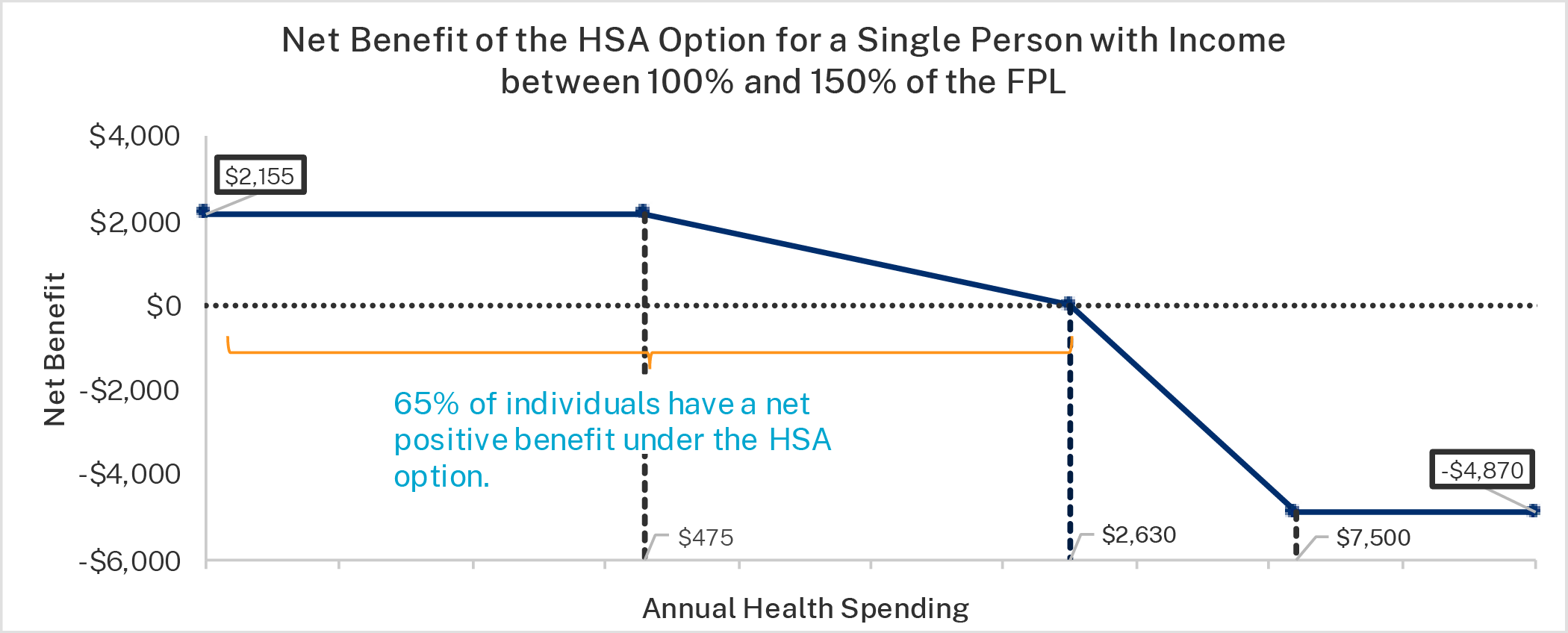

Table 4 also illustrates the potential benefit of the HSA option for the low-income group. Consider plan 1. If the enrollee chooses the CSR option, he faces a deductible of $475, which also represents the plan’s maximum out-of-pocket limit because there is no cost-sharing after the deductible is met. If the individual chooses that same plan but with the HSA contribution instead of the CSR benefit, he will receive an HSA deposit of $2,155. The plan deductible and out-of-pocket maximum would be $7,500, but the true out-of-pocket maximum would be $5,345—the maximum out-of-pocket limit minus the plan’s HSA contribution.

Milliman estimated the average benefit when the HSA option is beneficial and the average loss when the HSA option is not beneficial for enrollees.39 The average benefit of the HSA option, which varies across plan designs, is more valuable for lower-income enrollees since their HSA deposit is larger under the HSA option (given the requirements of the CSR program). The average benefit over the course of the year is about $550 for enrollees with income between 200 and 250 percent of the FPL, about $1,400 for enrollees with income between 150 and 200 percent of the FPL, and about $1,600 for enrollees with income between 100 and 150 percent of the FPL. For the relatively small number of enrollees who choose the HSA option but incur sizable medical expenses during a plan year, out-of-pocket expenditures would exceed HSA deposits, potentially by a few thousand dollars. Importantly, the Milliman analysis assumes that enrollees’ expenditures are covered by the plan, which will not happen in many instances because of the restrictive networks of most exchange plans.

Importantly, the limits on cost-sharing and expenses apply only if the individual receives care from in network providers. Not only do enrollees benefit when their health care spending is below the level equal to the HSA deposit and the CSR plan deductible amount, but they also have more flexibility to spend the money as they prefer. They can spend it for any qualified medical expense, not just what their plan covers. They can use it to access discounted cash prices and providers outside their plan’s network. They can also save anything they do not spend to use in subsequent years.

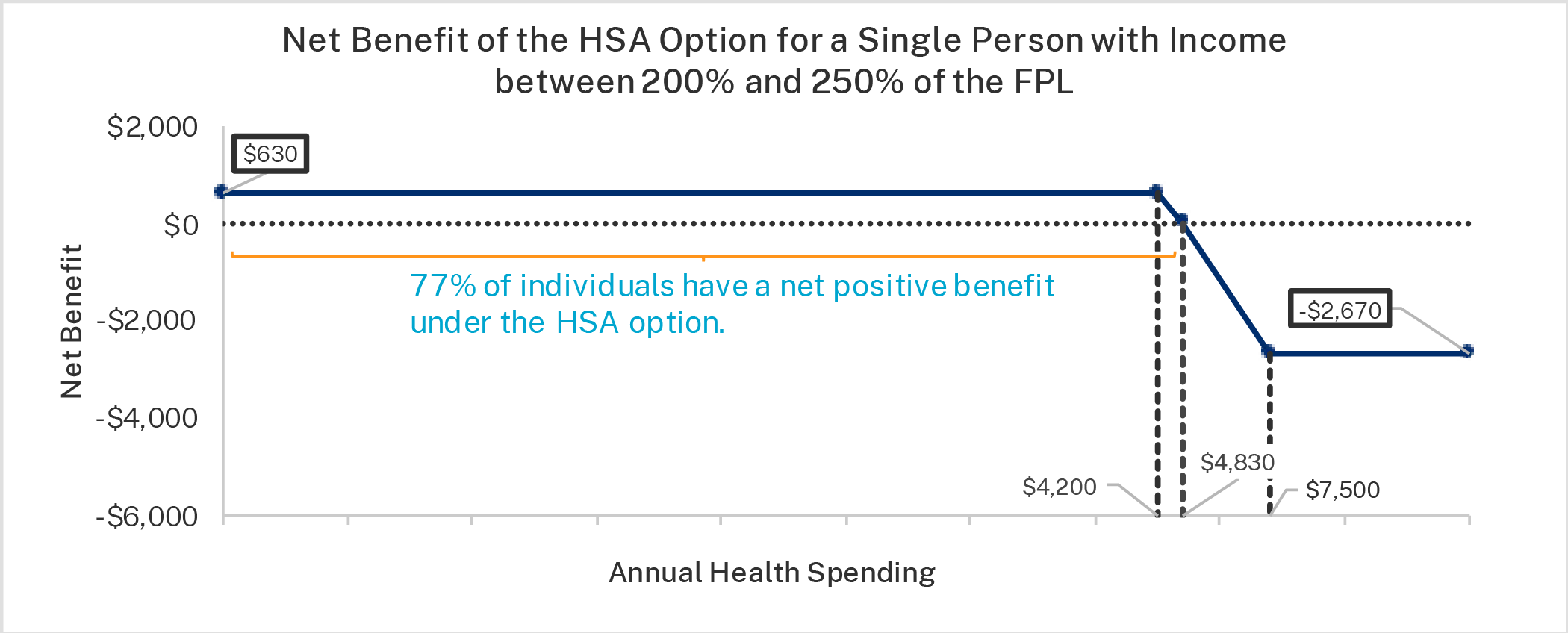

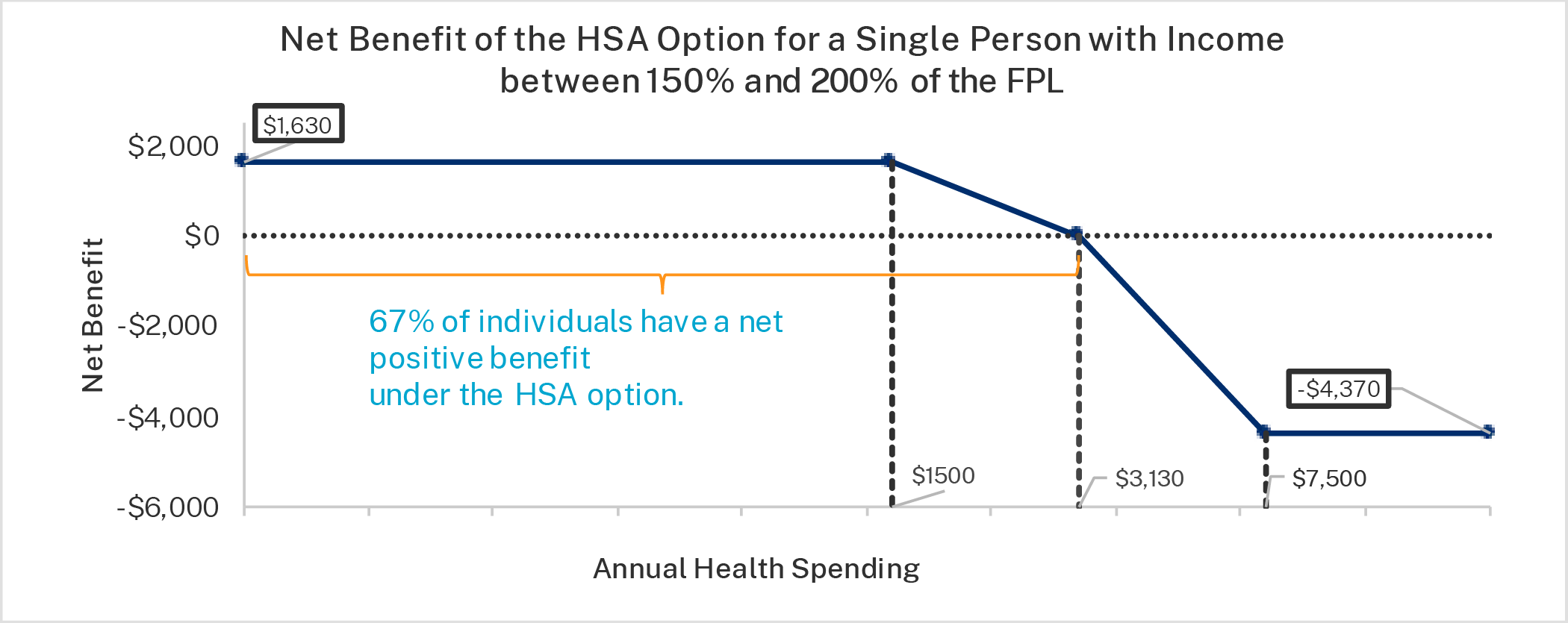

The figures below show the net benefit of the HSA option for the three income groups for plan 1. Plan 1 was used for illustration because the math is easier when there is no coinsurance. The first figure is the highest-income group, the second figure is the middle-income group, and the third figure is the lowest-income group. The figures show the net benefit based on annual health care expenditures. If enrollees do not have any annual health care expenditures—as roughly one in seven Americans do not—their net benefit from choosing the HSA option is the amount of the HSA deposit.

Importantly, these figures understate the value of the HSA option since the HSA can be used on a wider variety of health care expenses than under the CSR option, which is limited to services covered by the plan. Even accounting for this, most enrollees, would benefit from the HSA option since most enrollees have health care expenses below the break-even points. According to analysis provided by Milliman, roughly 65 percent of enrollees with income below 200 percent of the FPL benefit from the HSA option and roughly 75 percent of enrollees with income between 200 and 250 percent of the FPL benefit from choosing the HSA plan.40

As discussed, Milliman’s net benefit analysis does not account for the added value of HSAs since they can be used for a variety of qualified medical expenses beyond those typically covered by insurance. It also does not consider the greater efficiency that people obtain from using HSAs and the ability to stretch dollars further, assuming instead that health care expenditures remain constant under the CSR and HSA options. The greater efficiency or greater value is achieved since enrollees making expenditures from their HSAs tend to be more cost-conscious consumers

Under the ACA’s design, enrollees lack an ability to obtain the government subsidy to reduce their cost-sharing expenses in ways that best meet their preferences and financial situations. Moreover, the government subsidy is often of little value to enrollees, particularly those who expect minimal medical expenses during the year. Amy Finkelstein and coauthors estimate that Medicaid enrollees only value Medicaid at 20 to 40 cents of the cost of providing coverage.41 A recent economics study found consumers value the PTCs at less than half of their cost, with insurers capturing an excessive amount of the benefit.42 People’s welfare would be raised if, instead of subsidizing health insurers directly, the government allowed individuals to direct a portion of the subsidy to the purchase of health care they prefer. Another problem with the current CSR program is that lower cost-sharing reduces consumer incentives to obtain value from their medical spending and thus increases overutilization and waste, which our proposal would mitigate.

Impact by Age Group

One of the ACA’s main health insurance requirements is a 3:1 age-rating restriction, which prohibits the premium amount for the oldest member of the individual-market risk pool (a 64-year-old) from being more than three times the premium amount for the youngest adult in the risk pool. The PTC structure, which limits the amount of income that a household must pay for a benchmark premium regardless of age, results in much larger subsidies for older individuals than younger individuals. It is unclear, particularly with silver loading, how the overall subsidy to insurers for lower-income enrollees in silver plans is divided between the premium assistance and the CSR assistance. However, it is nearly certain that the amount of the HSA deposit that would be available to enrollees under the HSA option would be greater for older enrollees than for younger enrollees, perhaps approaching the 3:1 ratio.

Because of this reality, older enrollees—particularly those who expect below-average health care expenses—may be particularly attracted to the HSA option. For these individuals, they will be able to save money for the health care expenses that they will incur in retirement when they are likely to be enrolled in Medicare.

In addition to creating the HSA option, Congress can take other steps that would improve government policy and reduce federal deficits.

As noted previously, Congress does not currently appropriate taxpayer dollars to offset insurers’ CSR obligations under the ACA. The use of silver loading as a workaround has allowed insurers to fund their CSR obligations through higher PTCs.43 Total subsidies to insurers have likely increased because of silver loading.44

Congress should appropriate CSR payments, thereby providing a more direct subsidy mechanism. If it did so and prohibited silver loading, the overall cost of the subsidies would likely be reduced. This decrease would likely be more than the cost of a CSR appropriation.45

In 2018, CBO projected that a CSR appropriation would reduce federal deficits by $29 billion with the main effect being smaller subsidies for households with income between 200 and 400 percent of the FPL.46 Thus, according to CBO’s past estimate, directly funding CSRs and ending silver loading would result in a net decrease of federal deficits by billions of dollars each year.47 Such reforms could be used to offset the budgetary cost of the HSA option, while also reducing budget deficits and improving beneficiaries’ welfare.

1. Program Integrity Concerns

This proposal would give individuals greater control over ACA subsidies. While increasing individual control over these resources would enhance welfare, it does naturally raise questions about program integrity. In particular, enrollees—subject to a current-law 20 percent penalty48—could withdraw HSA funds for non–health care purposes. Our proposal takes steps to minimize this risk.

While improper payments are troubling in any context, we believe this program would have lower improper payment rates than many other government programs due to its essentially simple design, conformity with existing HSA rules, and reliance on secure debit card technology.

2. Enrollees’ Unfamiliarity with HSAs

Those who lack experience with an HSA will receive information from insurers under HHS and IRS guidance about how to set up and properly use one. They will also have a technological guardrail in the form of a restricted-use debit card to prevent accidental withdrawals for nonqualified expenses.

3. Enrollees’ Poor Decision-Making

Individuals and families have different preferences for meeting their health care needs. An HSA offers them maximum choice and control over their health spending. Some policy experts raise a concern that this much consumer freedom could lead to poor decision-making. For example, some participants may exhaust their HSAs early in the year without adequate funds later in the year for medical expenses. This problem can happen, but it is not unique to health care. People generally make decisions in the present that maximize expected utility, and they are best to weigh the tradeoffs that result from different choices.

On the whole, having an HSA has numerous benefits. First, because HSA savings roll over from year to year, people accumulate money against future medical expenses faster than they could otherwise. Second, because of the rollover and the fact that HSA savings are personally owned and controlled, consumers have incentives to ensure that the benefit from their spending exceeds the cost. Third, enrollees can use their HSA for any qualified medical expense. Fourth, HSAs protect consumers from out-of-network expenses, which are a growing problem for exchange enrollees since more than five in six health plans restrict access to providers.49 Some consumers may unintentionally use out-of-network providers and realize only later that their expenses were not covered by their plans. The HSA option minimizes this risk for those who select it.

This proposal is ultimately optional for enrollees. People with high and predictable health care costs, or who are simply uncomfortable with the HSA model, may always opt for the CSR plan rather than the HSA option.

4. Failure to Obtain Useful Preventive Care

Studies suggest that while people with HSAs reduce their utilization of health care services, they do not stint on needed care or useful preventive care. Multiple studies have found HSA ownership to be associated with higher rates of preventive care use.50 Such behavior is not entirely unexpected: when people have control over their own money, they have an incentive to try to minimize future expenses through regular investments in beneficial preventive maintenance.

5. Lack of Funds to Pay for Expenses

Some may raise concerns about cash flow and timing of HSA deposits. For example, an enrollee could incur high out-of-pocket health expenses early in the year before receiving enough monthly HSA deposits to cover them. This situation can be managed in the same ways that such situations are usually managed—through borrowing and deferred payment agreements. And nothing in our proposal prevents an insurer from accelerating the timing of a regular monthly deposit to assist an enrollee in need.

6. Adverse Selection Pressures

Opponents of consumer choice in health care often make arguments that such freedom will harm the ACA risk pool through adverse selection. The overall effect on the ACA risk pool from the HSA option should be minimal and likely beneficial for four reasons:

7. Mandate on Insurers

Some people may be concerned that this proposal includes yet another mandate on insurers, but in fact it merely modifies an existing mandate (the CSR program mandate) and only applies to insurers who voluntarily choose to offer products through an ACA exchange. Whether enrollees choose reduced cost-sharing or an HSA contribution, the insurer will be reimbursed by the government.

8. Higher Deficits

The budgetary effects of adding an HSA option are likely to be small, because such an option would alter rather than expand an existing subsidy. In effect, enrollees would be using a portion of their subsidy as an HSA deposit rather than reducing their plan cost-sharing amounts. If in addition to creating the option, Congress were to appropriate funds for CSRs and prohibit silver loading as we propose, CBO would likely score the proposal as actually reducing deficits because premiums would be lower, and therefore outlays for the ACA’s PTCs would be lower.

Congress can improve the welfare of lower-income individuals by creating an HSA option. This option permits enrollees a choice of directing a portion of their current, generous premium subsidy—the portion that insurers use to reduce plan deductibles and copayments—into an HSA that they own and control. According to Milliman’s analysis, the typical enrollee who selects the HSA option would accumulate a net HSA benefit, accounting for expenditures during the year, of about:

Moreover, the HSA option allows enrollees to use tax-preferred dollars to pay for medical items and services not covered by their insurance plans, including those provided by out-of-network doctors and hospitals. If Congress were to enact modest reforms of the CSR payment program in addition to the HSA option, the proposal would likely reduce federal deficits while expanding overall coverage.

What Is an HSA?

A health savings account (HSA) is a special financial tool created by Congress in 2003 to help Americans pay for out-of-pocket medical expenses tax-free. Like other bank and investment accounts, an HSA is personally owned and portable from job to job, but unlike other financial tools, it enjoys special tax advantages under existing federal tax laws (both income and payroll) as well as under most state income tax laws. HSA contributions, growth, and qualified withdrawals are all tax-free. This triple tax advantage makes the HSA unique among American savings vehicles.

Account holders may use tax-advantaged HSA funds to pay for a wide array of qualified medical expenses as well as to cover deductibles under a health insurance plan, not only for themselves but also for a spouse and dependents. Nonqualified withdrawals are taxed as income and subject to an additional 20 percent penalty.51

HSA balances may be saved or invested, accumulate indefinitely, and be left to a surviving spouse or designated beneficiary. Unlike owners of individual retirement accounts, HSA owners are not subject to required minimum distributions after a certain age.

HSA holders receive what is effectively a price discount on each medical purchase. Having a funded HSA also provides a source of funds to help pay for health care expenses between jobs or expenses not covered by health insurance and a cushion against annual increases in insurance maximum out-of-pocket limits. Having an HSA can help smooth health care expenditures over a lifetime and provide a health care nest egg for retirement.

HSAs promote tax equity. As a result of federal and state tax laws, most health care expenditures in the United States today are paid by third parties, such as insurers and employers, rather than by patients. This situation leads to economic distortions and medical price inflation. HSAs help counter these distortions by providing tax breaks for health care purchased directly by patients. Studies suggest that HSAs help reduce overall health care spending without causing patients to stint on preventive care. This trend is likely because people tend to be more careful when spending their own money.52

Roughly 33 million Americans—about one-tenth of the U.S. population—have an HSA account, and experts predict this figure will grow to 38 million by the end of 2024. Account holders’ spouses and dependents also benefit from HSAs. Thus, over 60 million Americans—approximately one-third of the U.S. population with private health insurance coverage—currently benefit from HSAs. Aggregate HSA balances exceed $100 billion and are projected to exceed $150 billion by the end of 2024.53

Despite these figures, per capita HSA enrollment is unlikely to grow substantially under current law because access is restricted. To contribute to an HSA, a taxpayer must have a specific, federally defined form of health insurance called a “high deductible health plan” (HDHP). (In this paper, we refer to HDHPs as HSA-qualified plans.) To be an HDHP, a plan must conform to federal rules regarding minimum deductible and maximum out-of-pocket amounts, and certain items and services covered by the plan must be exempt from the plan deductible. Because most health insurance plans, including most employer-sponsored plans, do not meet these criteria—most Americans are effectively barred from using this powerful financial tool.54

How Do ACA Subsidies Work?

Since the beginning of 2014, the ACA has imposed a complicated assortment of mandates on the group and individual health insurance markets. It has also provided means-tested subsidies to eligible people who purchase insurance coverage in the individual market through an ACA exchange.

The largest and most important of the ACA’s subsidies is a premium subsidy that typically goes directly to exchange insurers on enrollees’ behalf. This subsidy takes the form of a PTC, the amount of which is largely a function of the benchmark plan premium and the household’s income. The credit is structured to limit the amount of income that the household owes for a benchmark plan. When the credit is paid out ahead of time, in monthly installments, it is known as an advance premium tax credit (APTC). A household qualifies for an APTC based on its estimated income, and the government sends a monthly payment to the insurer selected by the household. At tax time, when actual household income for the previous year is known, the enrollee must go through a reconciliation process for overpayments or underpayments.

About half of enrollees receive additional support in the form of plan cost-sharing reductions, also called CSR payments. As explained elsewhere in this paper, this support currently takes the form of an embedded boost in the PTC subsidy that indirectly compensates the insurer for its costs of complying with the CSR mandate.55

The ACA’s rules have caused premiums in the individual market to soar, with average premiums increasing from $242 to $589—a 143 percent increase between 2013 and 2019.56 Deductibles have also soared.57

Although insurer participation in the exchanges has grown in recent years, fewer insurers are currently offering coverage on ACA exchanges than were offering coverage on the pre-ACA individual market in 2013, and increasingly the plans they offer are narrow-network HMOs.58

The ACA’s high premiums and deductibles and narrow networks are unattractive to people who lack eligibility for large subsidies, and this is almost certainly why individual market enrollment declined each year from 2015 to 2019. Although enrollment increased in 2020 and 2021, the increase was due to temporary subsidy expansions enacted as part of the congressional response to the COVID-19 pandemic.59 Those expansions have been extended through 2025 by the Inflation Reduction Act. Regardless, individual market enrollment has increased by only a few million people from the pre-ACA levels.60

From the enrollee’s perspective, ACA premium subsidies can be very generous, with the most benefit going to lower-income enrollees and leading many people to purchase plans with little, if any, out-of-pocket premium expense.61 In 2020, the subsidy for a typical subsidized enrollee covered 86 percent of the plan premium.62 From the taxpayer’s perspective, the subsidies are inefficient and inflationary, placing excessive upward pressure on the cost of coverage and increasing the government’s costs.