Today’s newsletter discusses developments with the implementation of the No Surprises Act, recent reports on enrollment problems in the ACA exchanges, and a congressional proposal to reform the tax treatment of health insurance.

Surprise Billing Act Not Off to a Good Start

The No Surprises Act, legislation enacted to cure surprise medical bills, is not working as intended and is likely raising health care expenditures. Understandably, Congress wanted to protect insured patients from excessive costs in two situations: 1) in medical emergencies and 2) when they go to in-network facilities but receive treatment from a provider who is out of their network. In both cases, Congress limited patient cost-sharing to no more than they would owe for receiving in-network services.

Rather than leaving insurers and providers to settle on the price for services in which there was no prior contractual arrangement, Congress opted for an arbitration system—so-called independent dispute resolution (IDR). This led to the creation of a new bureaucracy through the Department of Health and Human Services in which the federal government is now a party to resolve payment disputes.

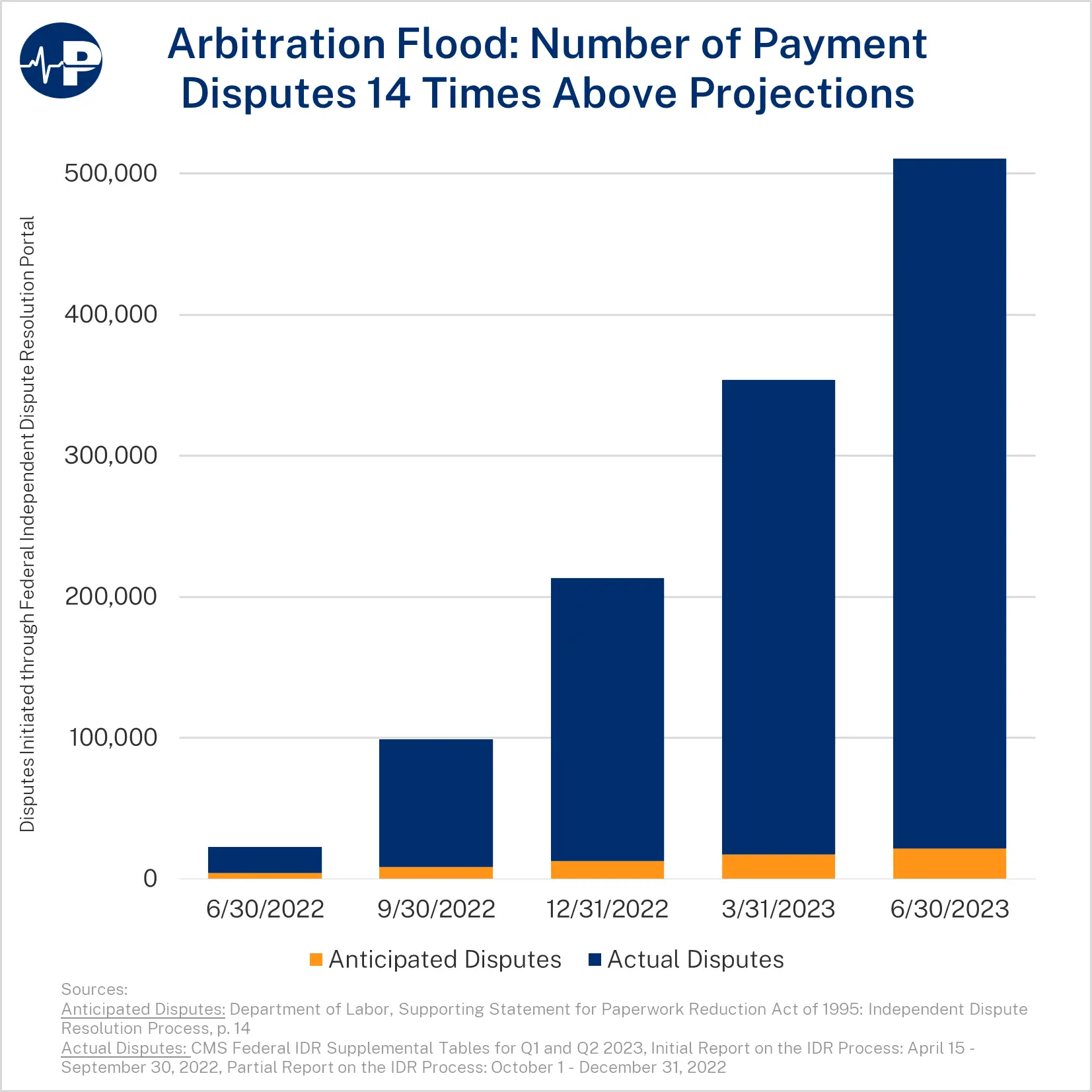

As the Paragon Pic below shows, there has been a flood of cases submitted to IDR. Here is HHS’s own description:

In the first year … disputing parties submitted 14 times the number of disputes that the Departments had expected to receive in an entire calendar year. Due to this unexpectedly high volume, the limited number of certified IDR entities, the complexity of determining disputes’ eligibility for the Federal IDR process, and a large number of ineligible disputes submitted, it is taking certified IDR entities longer than the timeframes established … to process payment disputes.

In addition to an overwhelming flood of cases, the selected prices are much higher than expected. According to a new Brookings Institution review, the median IDR decision is nearly 4 times what Medicare would pay and the median decision is at least 50% higher than historical mean in-network commercial prices.

Unfortunately, much of what the federal government does in health policy does not work as politicians intend—almost always to the detriment of American families. It appears that The No Surprises Act is no exception. Early evidence shows it will increase what Americans pay for health care, largely through higher insurance premiums, while adding additional administrative complexity to an already too complicated payment system.

Chaotic ACA Plan Switching

While the Biden administration used bogus rationale about consumer confusion to dramatically worsen short-term plans, there are genuine concerns of rapidly growing abuse with ACA exchange plans. According to a recent report by KFF Health News’ Julie Appleby:

Unauthorized enrollment or plan-switching is emerging as a serious challenge for the ACA, also known as Obamacare. …

Indeed, armed with only a person’s name, date of birth, and state, a licensed agent can access a policyholder’s coverage through the federal exchange or its direct enrollment platforms. …

Some unwitting enrollees, like Michael Debriae, a restaurant server who lives in Charlotte, North Carolina, not only end up in plans they didn’t choose but also bear a tax burden.

This chaos is a result of recent public policy changes as well as the Biden administration prioritizing enrollment over program integrity. Because of a large increase in subsidies to health insurers, taxpayers are covering the vast majority of premiums for most exchange enrollees and the entire premium for roughly half of them. Knowing this, brokers can switch peoples’ plans and reap commissions with enrollees having no financial liability. Many exchange enrollees use little, if any, medical services during the year, so lack incentive or insight to police this. Therefore, the number of people being unwittingly switched is undoubtedly magnitudes more than the number of complaints would indicate. The apparent ease with which personally identifiable information can be accessed by a wealth of outside parties should also be investigated.

One other point demonstrates problems with the ACA’s core structure: Although the government sends the subsidy directly to the health insurer, if an individual, like Mr. Debriae, is unwittingly enrolled and is not eligible for the subsidy, the IRS will come after the individual and not the insurance company at tax time.

Capping the Employer-Sponsored Health Insurance Exclusion

Later this spring, Paragon will release a comprehensive paper authored by Paragon senior research fellow Theo Merkel and me on the provisions of the tax code that influence health care and health insurance expenditures and how Congress can better rationalize the tax code to improve economic efficiency and reduce wasteful health care expenditures.

Perhaps the most prominent provision of the tax code that affects health coverage is the tax exclusion for employer-sponsored health insurance (ESI), in which the premiums paid for ESI are an untaxed form of compensation. In a new National Review piece, Paragon’s Dr. Joel Zinberg highlights a House Republican Study Committee budget proposal to cap the exclusion. Joel first explains the economics of the exclusion:

This is the tax code’s largest tax expenditure, reducing federal revenue by almost $3 trillion between 2019 and 2028. It encourages employers to substitute untaxed health-insurance expenditures for taxed wages and employees to obtain their health coverage at work. Economists have long regarded the exclusion as economically inefficient and regressive.

Joel writes that the proposal to cap the exclusion would reduce wasteful health expenditures and lead to cheaper plans and higher wages. The political reality is that tackling the exclusion in such a broad way will be difficult. The ACA’s Cadillac tax, which would have penalized overly expansive ESI, was repealed in a huge bipartisan vote before it ever took effect.

In addition to capping the exclusion, the RSC proposal would eliminate the ACA subsidies, create a state block grant program to subsidize health coverage, and extend the same level of ‘capped’ tax exclusion to all Americans. Undoubtedly, this policy mix would create a much more efficient health sector and be a better use of taxpayer dollars, but it would be politically very difficult to achieve. The proposals that Paragon will release later this spring will advance a health tax reform agenda that introduces new policy options and refines old ones to give workers more control over their health care and reduce the most inflationary aspects of health-related tax policy.

All the best,

Brian Blase

President

Paragon Health Institute