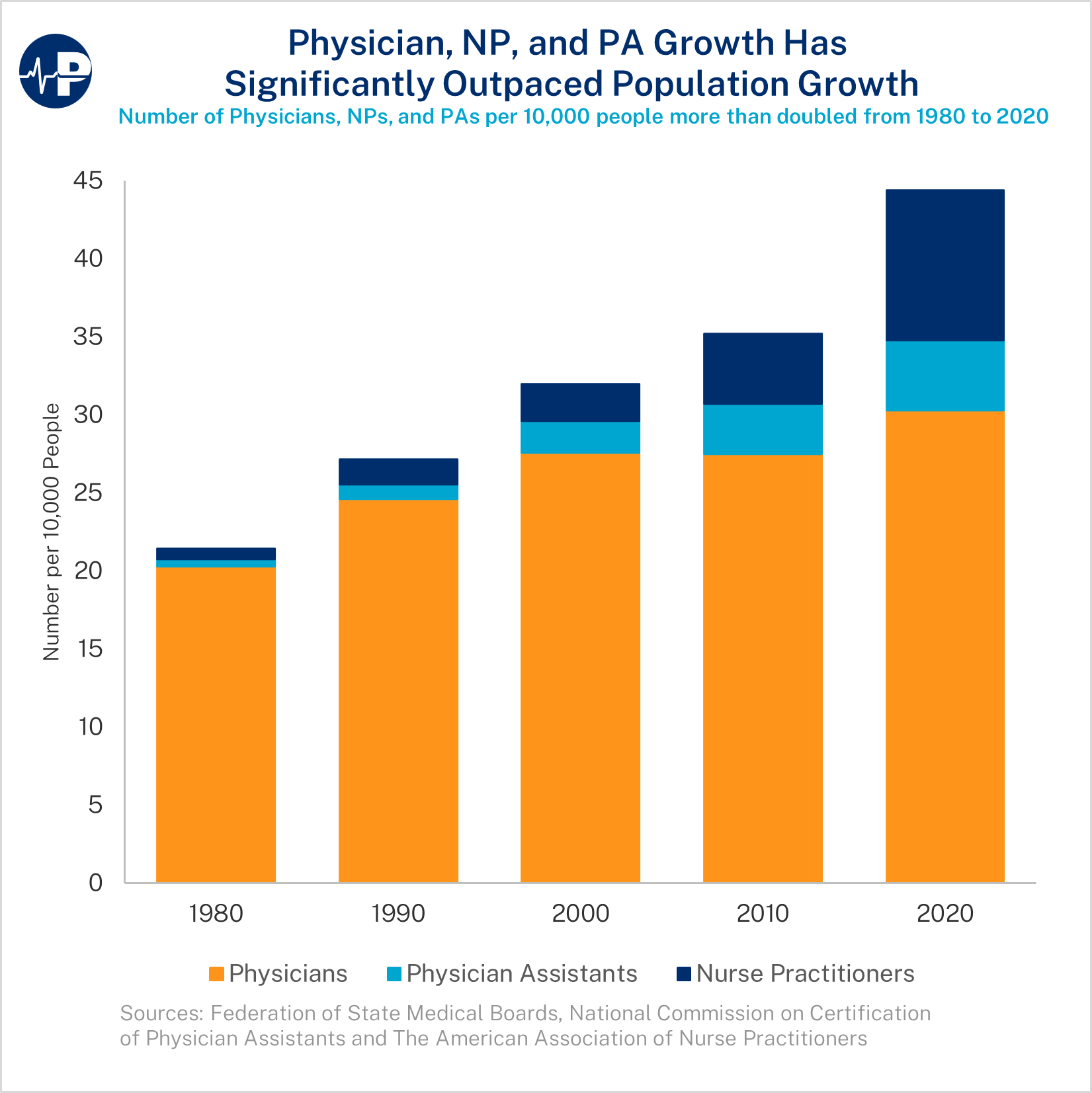

Spring is in the air, and Paragon is out with a new policy paper that investigates the federal government’s extremely outdated methods of distributing taxpayer resources through programs designed to alleviate health provider shortages. A Paragon Pic, which complements the paper’s analysis, shows that the aggregate number of physicians, nurse practitioners, and physician assistants has more than doubled per capita since the federal government created these programs. Finally, I highlight a recent piece I coauthored with long-term care (LTC) expert Steve Moses in an attempt to correct several problems with the LTC policy debate.

Improving How Washington Determines Provider Shortage Areas

Today, Paragon released an important new paper, Where are Provider Shortages? Reassessing Outdated Methodologies, authored by rural health expert Bill Finerfrock. Bill finds that the methodology used for decades to determine whether a shortage of health professionals exists is outdated and results in a mismatch of federal dollars to actual need.

The key problem: the shortage area designations used by the federal government—Health Professional Shortage Areas (HPSAs) and Medically Underserved Areas/Populations (MUA/P)—reflect the primary care workforce of the 1970s. In addition, thousands of communities designated by the federal government as underserved in the 1970s, 1980s, and 1990s have not been re-evaluated since they were initially classified as MUA/P.

If the federal government revised the methodologies to include the primary care workforce available in 2024, thousands of communities currently designated as underserved would see their shortage area classification removed. Furthermore, if the federal government updated the designations for thousands of communities that were last reviewed more than 30 years ago, many would no longer be designated as underserved due to changing workforces and demographics in those communities.

The federal government commits billions of dollars each year to support a wide range of health professionals in their educational training in exchange for those individuals agreeing to work in shortage areas upon completion of their training. In addition, billions of taxpayer dollars are spent on supporting Rural Health Clinics, Community Health Centers, and Federally Qualified Health Centers in communities where they may not be needed. This directs resources away from communities that are truly underserved and in need of assistance and costs taxpayers more than is justified.

In this Paragon paper, Bill recommends:

- Updating the list of shortage areas to reflect the modern workforce;

- Incorporating nurse practitioners (NPs) and physician assistants (PAs) into the provider-to-population ratio used to determine shortage areas;

- Excluding physicians, NPs, and PAs who are recruited to a shortage area by a federal program designed for this purpose from counting toward the loss of such designation.

Physician, NP, and PA Growth Has Significantly Outpaced Population Growth

This week’s Paragon Pic (below) shows, contrary to popular belief, that the United States has more physicians per 10,000 people today than it has ever had. In addition, U.S. patients now have the benefit of the nearly 600,000 currently practicing nurse practitioners (NPs) and physician assistants (PAs). Overall, the number of these health professionals per 10,000 people more than doubled between 1980 and 2020—from 21.4 per 10,000 to 44.4 per 10,000. Roughly 43.6% of that increase was from the growth in physicians and about 56.4% of that increase was from the growth of NPs and PAs, two classes of professionals that were largely nonexistent in 1980.

Setting the Record Straight on Long-Term Care Policy

Before we can reform government programs, we first need to correctly diagnose how they operate and document the resulting problems. Perhaps no health policy-related area has more common misperceptions than LTC. Recent stories by The New York Times and the Associated Press make common errors about LTC policy, particularly with respect to the role of Medicaid. In a new Townhall piece, Steve Moses and I lay out what policymakers need to understand. We discuss the key problems:

The most important fact for policymakers: middle class and affluent people may easily access Medicaid for their LTC needs, without having to deplete their assets first. It is the poor and underprivileged who typically lose everything due to Medicaid’s spend down rules.

Income rarely obstructs eligibility for Medicaid LTC. …

Sizeable assets also rarely prevent eligibility. Large assets are exempt from Medicaid eligibility determinations, including most home equity, a business, IRAs, a vehicle, prepaid burial funds, home furnishings, and personal belongings. People can take liquid wealth, purchase exempt assets, and apply to Medicaid. On top of easy eligibility requirements, elder lawyers can artificially impoverish wealthier applicants using special trusts, annuities, and other complicated strategies.

And also the solution:

Policymakers should eliminate Medicaid eligibility policies that favor the prosperous and harm the poor and instead incentivize early planning for future LTC risk. New research shows the average American could cover future LTC cost by setting aside $70,000 at or before age 65. Policymakers should let people use funds they’ve already accumulated in home equity, retirement savings and life insurance if LTC is needed.

Such policies would unleash the substantial wealth lying fallow in the American economy. More private financing that pays LTC providers better rates would help attract skilled caregivers, improve nursing home quality, and lead to more and better home-based care.

Thanks for taking time to catch up on Paragon’s recent work.

All the best,

Brian Blase

President

Paragon Health Institute