In today’s newsletter, I discuss a recent misguided Biden administration rule to take away an affordable health coverage option and the growth of the 340B program.

Biden’s Rule Will Cancel Coverage for People Who Get Sick

On March 28, the Biden administration severely restricted health coverage that has benefitted millions of Americans. The rule requires insurers to cancel short-term plans after just four months. Short-term plans are exempt from most federal health insurance regulations, including mandates in the Affordable Care Act, and thus have much lower premiums for plans that typically cover far more doctors and hospitals. The rule reduces the allowable term for short-term plans from 36 months. This rule is rare in that there are clear losses to millions of people with only speculative and trivial benefits.

Here are three clear harms:

- This rule severely reduces consumer protections. Because of the limited ACA enrollment period, people who lose a short-term plan and get sick will have no ability to gain other coverage. Enrollees who do not get sick will be able to buy another four-month plan from a different insurer.

- This rule will lead to hundreds of thousands of additional people without health insurance. The ACA exchange plans are only attractive to people who obtain large subsidies to purchase them and many people, including the self-employed and 1099 contract workers, can afford a short-term plan but not an unsubsidized ACA plan.

- My research shows that the ACA exchanges performed much better from 2018 to 2023 in states that permitted short-term plans compared to states that restricted short-term plans. Thus, this rule appears more likely to harm than help the ACA individual market.

The administration ignored the actual evidence that the ACA markets performed better in states that permit short-term plans, dismissing Paragon’s comment and writing that short-term plans and ACA plans are “very different products,” and issuers of ACA plans are unlikely to have changed their product offerings to compete with short-term plans. Given this is the Biden administration’s perspective, their main rationale that its restrictions were necessary to prevent consumer confusion between short-term plans and individual market plans falls flat.

This rationale was always suspicious. Unlike ACA plans, which most enrollees only purchase because a subsidy covers all or most of the premium, people use their own money to purchase a short-term plan. Thus, they have incentives to make sure that the plan provides significant value to them and thus people, on average, receive far more value from a short-term plan than from an ACA plan.

Finally, this rule is plagued by aspects of cronyism, as the main beneficiaries are insurers that offer ACA plans that want to restrict their competition. Cato’s Michael Cannon has several important pieces on this misguided rule.

Contract Pharmacy Growth in 340B

The 340B Drug Pricing Program started as a small program in 1992 to better enable safety-net hospitals and other 340B covered entities (CEs) to provide care to more indigent patients by mandating that pharmaceutical manufacturers give the CEs large discounts on prescription drugs. CEs like qualifying hospitals were allowed only one off-site contract pharmacy in case they did not have an on-site pharmacy. A 340B contract pharmacy is a pharmacy that has entered into a written agreement with a 340B CE to dispense discounted drugs to eligible patients on behalf of the CE, such as retail or specialty pharmacies.

340B Growth

Explosive growth from the Affordable Care Act and an Obama administration rule implementing it have caused the 340B Program to become the second-largest drug program in the country behind Medicare Part D.

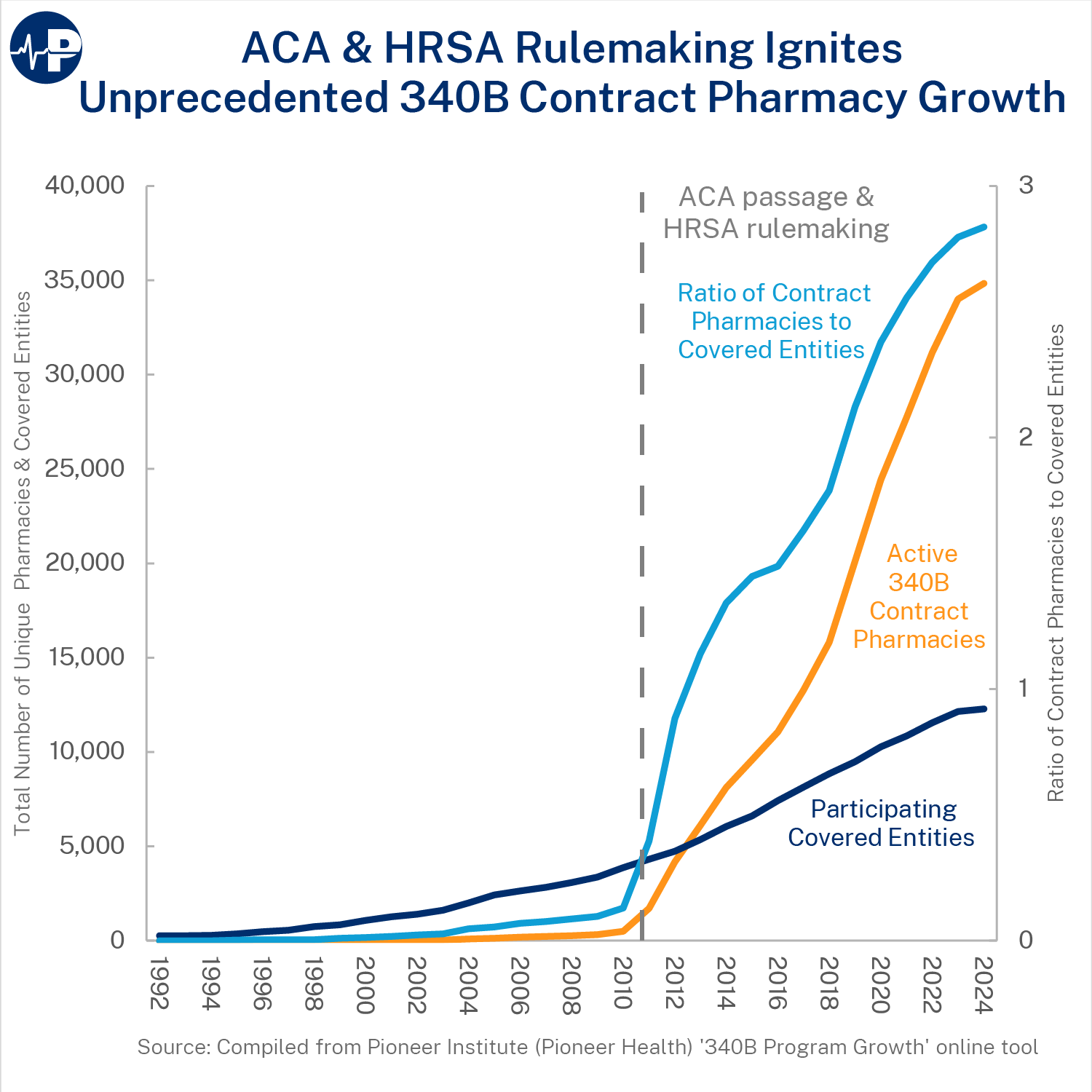

Starting in 2010, CEs were permitted to have virtually unlimited numbers of contract pharmacies, resulting in a nearly exponential increase in contract pharmacies in the program. As shown in the Paragon Pic below, the number of contract pharmacies increased from 503 in 2010 to 34,840 in 2024 – a whopping 6,826 percent increase.

According to the Pioneer Institute, hospitals used 17,250 contract pharmacies in 2024, up from 76 in 2010. By comparison, the number of CEs more than tripled from 3,866 in 2010 to 12,279 in 2024. Accordingly, as the Paragon Pic demonstrates, the ratio of contract pharmacies to CEs has substantially increased.

Lack of Transparency

The contract pharmacy surge also correlates with a major increase in the program’s cost (as measured in purchases at discounted 340B prices)—from $9.0 billion in 2014 to $53.7 billion in 2022. Despite the increased number of contract pharmacies that are helping CEs bring in record revenue, it is unclear if this revenue is being used to support the program’s original intent due to lack of transparency requirements.

As a 2014 report from the Government Accountability Office notes: “without adequate oversight, the complications created by contract pharmacy arrangements may introduce vulnerabilities in the 340B Program.” Moreover, although the purpose of the 340B Program is to support safety-net providers, increasing evidence suggests that the opposite is occurring. A 2022 JAMA paper found that “contract pharmacy growth was concentrated in affluent and predominantly White neighborhoods, whereas the share of 340B pharmacies in socioeconomically disadvantaged and primarily non-Hispanic Black and Hispanic/Latino neighborhoods declined.”

All the best,

Brian Blase

President

Paragon Health Institute