Small Businesses and Health Insurance

According to 2022 data from the Kaiser Family Foundation, the average annual premium for employers with 50 or fewer workers is $8,012 in annual premiums for single worker coverage, with family average exceeding $22,000.1

Post-COVID Small Business Environment

The aftermath of COVID has been devastating to the small business community. A combination of lockdowns, inflation, and supply chain problems have led to widespread business closures.

An accompanying labor shortage has led to higher salary expenses while general inflation hit a four-decade peak during 2022. A poll of 6,000+ small firms by the small business network Alignable found that 41 percent couldn’t pay rent on time or in full for November 2022.2

Background on Small Business Health Care Costs

Back in 2002, the government’s Medical Expenditure Panel Survey estimated that 44.5 percent of private sector firms (with fewer than 50 employees) offered health insurance. This percentage fell to 31.9 percent by 2021, a decline of 28 percent. During the same period, the average premium for a single employee rose over 118 percent, while the average family premium grew 140 percent.3

High costs threaten the availability of health benefits across the small firm landscape. A 2022 survey of 1,209 small firms found that 53 percent have considered ending health coverage due to rising cost.4 The same survey found that 74 percent have considered reducing employer contributions to employee health insurance costs.

Unaffordable health benefits adversely affects many dimensions of the small business market. A variety of U.S.-based surveys have observed health insurance expenses leading small businesses to:

- Cancel Raises and Reduce Hiring – Due to high health insurance costs, 45 percent of small firms could not increase salaries, and 37 percent could not expand their workforces.5

- Increase the Price of Goods and Services – 41 percent of small firms raised prices because of health insurance costs.6

- Convert Positions to Part-Time or Lay-Off Workers – Health insurance was the most common cause of unexpected expenses causing job conversions to part-time work or the layoff of workers.7

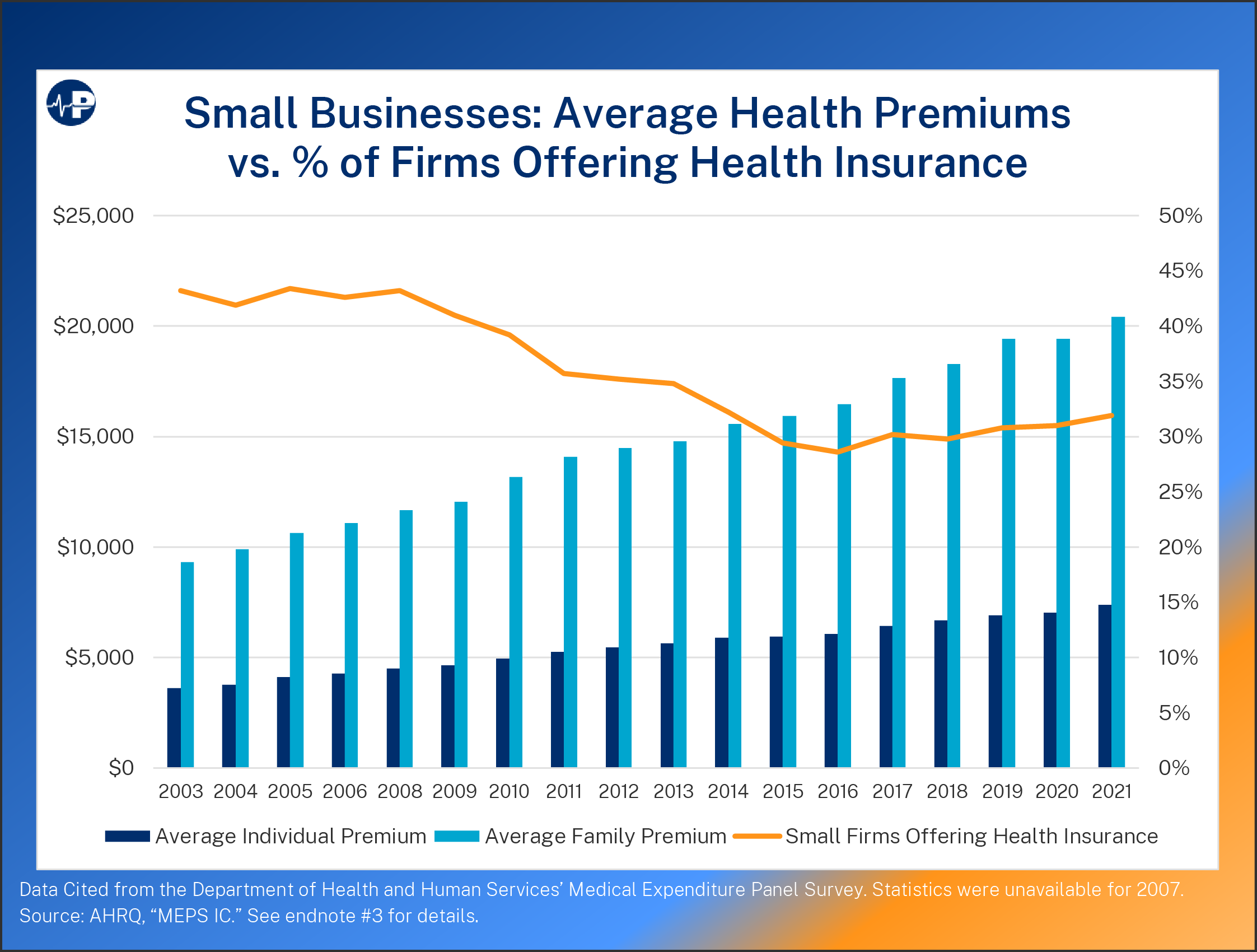

Small Business Insurance Premiums 2002-2021

The above chart displays small business health insurance premium growth over the past two decades. Family premiums for employees of small businesses increased an average of 7 percent from 2002’s baseline for 20 years, bringing the average family premium to $20,406 in 2021 from 2002’s $8,502.8 Individual coverage experienced a similar escalation: from $3,375 in 2002 to $7,382 in 2021. This is a rise of nearly 119 percent, which represents an additional 5.9 percent of expense each year during this period.9

Economists widely agree that the full cost of employer health coverage is borne by the employee (which includes the employer contribution that might otherwise go toward worker wages). However, the explicit contributions employees make in premiums may affect coverage participation. In 2002, the average employee contribution toward family health premiums was a quarter of its total cost.10 By 2021, the percentage exceeded a third of cost.11 This upward cost trend has coincided with a downward trend in health plan participation. Employee enrollment within small firms offering health coverage has declined from 61.3 percent to 53.8 percent over the past two decades.13

Gig Workers: The Overlooked Small Businesses

Gig work is a phrase often used to describe a variety of labor performed outside the model of permanent employment for a company. This labor may be either the worker’s primary income or supplemental earnings. Gig work covers independent contracting, freelancing, sole proprietorships, and other forms of incorporated and unincorporated businesses.

Given their labor performed outside permanent employment arrangements, gig workers are typically excluded from employer-sponsored health benefit plans. According to independent worker platform Stride Health, 24 percent of gig workers lack health insurance, and 58 percent of these uninsured gig workers cited prohibitive cost as the basis for why they did not purchase health coverage.12

Out-of-Pocket Costs Spike

Employee health care costs are more than monthly insurance premiums. Health plans engage in cost-sharing for covered medical services, where the plan members pay a portion of the health care costs directly from their own resources. These contributions are known as out-of-pocket costs and come in the form of deductibles, copayments, and co-insurance fees. While copayments and co-insurance are expenditures made alongside insurance company spending, a deductible is an amount of covered health care costs that a plan member must pay on his or her own before the health plan begins to pay for incurred health claims.

The percentage of small business employees whose health plan required a deductible contribution toward health care costs rose from 54.2 percent in 2002 to 86 percent in 2021.14 In other words, 58.6 percent more employees had deductible obligations than had been the case 20 years prior.

The expense of deductibles themselves grew dramatically in those 20 years. In 2002, the average deductible for family coverage was $1,371. By 2021, this amount had grown 260 percent to $4,945.15 Deductibles for single employee coverage grew even faster. The average 2002 deductible for health coverage was $602 for an individual employee with no spouse or dependents. Twenty years later, the average deductible for single employee was $2,485.16 This 2021 average was over four times the 2022 average and represented an out-of-pocket expense increase over 312 percent.

Why Small Biz Health Care Costs Can’t Be Ignored

Small businesses are a key component of the American economy. Over 5 million small businesses employ nearly 35 Americans17 in the private sector, according to data from the Bureau of Labor Statistics. To ignore the threat insurance costs pose to employment and wage growth at small businesses is to ignore the trouble facing the employer of one in five adults in the United States.

The Inequalities of Big Business Health Plans

While health insurance costs are escalating throughout the economy, large companies have enjoyed savings advantages unavailable to small businesses. These advantages, often related to scale, have created an environment where a big business pays less than a smaller firm for the same health benefits. For example, health insurance load (i.e., the premium portion that exceeds expected medical expenditures paid by the insurer) are higher for small groups as compared to large. Multiple studies have observed loads for businesses with 100 or more employees being less than half the expense compared to small businesses with fewer than 100 employees, with the savings growing larger for very big businesses.18 Large companies with thousands of employees are also in a better position to negotiate with insurers, because large employers offer insurers a bigger risk pool over which health claims may be spread and moderated. In some cases, these large companies can also negotiate lower rates with health care providers (because large employers offer providers a large volume of patients to utilize their services). However, health care providers have consolidated across the nation, and the negotiating power of large group health plans has diminished.19 Consequently, negotiation leverage may often require more covered lives than a single large company can provide within a given region. This need for greater scale, as the next section will demonstrate, can be addressed through an instrument analogous to cooperative purchasing.

A second advantage of large group health plans is overhead expenses. Among the areas in which large businesses have cost advantages is the percentage of premiums that can legally be used for profit and administration within a fully insured health plan. Small group plans devote 20 percent of their premiums to profit and overhead. Large group health plans, in contrast, are restricted to 15 percent for the same items, giving them a 5 percent savings advantage.20 Another cost efficiency for large group plans derives from the absence of a “user fee.” This fee, ranging from 2.25 percent to 2.75 percent of premiums, is charged to insurers selling “individual” coverage on an Affordable Care Act (ACA) exchange to self-employed businesses. In a state-based exchange such as Covered California, the charge is 5.2 percent for small group plans for businesses with multiple employees.21

A third advantage of large group health plans is the ability to customize the health plan’s benefit design to include features that can potentially lower premiums such as programs incentivizing positive health outcomes and economic value in medical treatment. While large group health plans do have benefit requirements, these mandates are not as costly as those mandates applicable to individual and small group market plans. Large group plans can also reduce costs by unbundling supplemental benefits such as vision and dental care into separate group plans. Accordingly, those who don’t desire such coverage do not pay for it, while those with such preferences still benefit from group rate savings.

Another advantage of large group health plans is their compatibility with self-insurance models where the employer pays for medical claims as opposed to a third-party insurer. Fully insured health plans, unfortunately, have a disincentive to control costs. Medical loss ratios constrain insurer earnings to a portion of premiums, so an efficient plan with less expensive medical claims reduces insurer revenue.

While small businesses may self-insure, it is difficult due to cash reserve requirements as well as the greater medical claims fluctuations of small risk pools. For large companies, self-insuring eliminates the cost of insurer profits and state premium taxation. More savings are afforded by claims analyses that identify billing errors and service “upcoding” by health care providers. Insurance companies, in contrast, are generally resistant to sharing claims data for analysis and may insist on quick claims payment even when the billing lacks proper Current Procedural Terminology (CPT) itemization. Another important self-funded savings advantage is the option of using a pharmacy benefits manager with a cost-plus pricing model (where rebating and spread-pricing schemes are prohibited). Fully insured health plans, unfortunately, have a disincentive to control costs in the manner outlined above for self-insured plans given rules around medical loss ratios.

Fairness for Small Business

Since large group health plans have innate cost savings, and they cover 78 million Americans22 (which is more than covered by the entire Medicare program) with high rates of satisfaction, federal policymakers should implement a framework extending these advantages to small businesses while retaining appropriate consumer protections. Essentially, the Department of Labor (DOL) should:

- Promote a legal instrument that allows small businesses to band together within a single employer group to obtain affordable large group health insurance coverage

- Preserve existing federal and state regulations enforcing consumer protections for large group health insurance plans

- Prevent a third party, including but not limited to insurance companies, from owning or controlling the health plan sponsored by an employer group

The DOL has a pre-existing tool—association health plans (AHPs)—that can be improved through regulatory changes to accomplish the above goals and bring equity to small business health insurance. An AHP is an organization composed of companies working together to provide their employees health coverage through a single large group health plan. While AHPs have existed for decades, suboptimal regulatory design and market access restrictions have prevented AHPs from widely transforming small business health coverage.

Large Group Requirements Applicable to AHPs

An AHP is considered a “group health plan” for purposes of the ACA and, thus, is subject to the ACA ’s “group health plan” requirements, which include:

- Covering pre-existing conditions

- Covering government-specified preventive care without copays

- Prohibiting annual/lifetime spending limits for all care coinciding with Essential Health Benefits

- Offering internal and external benefit determination appeals

- Retaining enrollment for eligible dependent children up to age 26

- Prohibiting benefit waiting periods beyond 90 days from the day of employee hire

Other legal requirements for AHPs outside the ACA include:

- HIPAA nondiscrimination rules (see discussion on next page)

- Covering maternity and newborn care similarly to other plan services

- Covering childbirth hospital stays of at least 48-hours

Complying with COBRA obligations allowing participants to continue in the health plan for 18–36 months despite termination (or hours reduction)

Recommended Improvements

The core savings mechanism of an AHP is the consolidation of many companies into a single buying unit. There is considerable precedent for this practice as seen in group purchasing organizations, professional employer organizations, group captives, and cooperatives (such as ACE Hardware). In each of these examples, organizations employ a similar strategy where demand for products/services is pooled among multiple businesses to secure lower prices from suppliers.

AHPs are regulated primarily under the Employee Retirement Income Security Act of 1974, though their operation is also governed by provisions within many other laws such as the Health Insurance Portability and Accountability Act (HIPAA) and the ACA. Legacy regulations for AHPs have deficiencies needing improvement if employer groups are going to share in the health care savings already enjoyed by big companies. These improvements fall into three categories:

- Reducing the barriers small businesses face when trying to band together to sponsor a single large group health plan

- Extending large group health plan savings to workers laboring within the gig economy

- Protecting AHPs from “bad actors” who misrepresent benefits or make false/misleading claims

These improvements would provide small businesses with lower cost health coverage, a stable insurance market, and sensible consumer protections. Moreover, the above goals can be accomplished without billions in new government premium and cost-sharing subsidies (the type of subsidization in the “individual” market) or further taxpayer spending for online marketplaces (i.e., the ACA exchanges) and tens of millions in grants and marketing for organizations assisting individuals with health insurance shopping and enrollment (i.e., the ACA’s Navigators).

HIPAA Non-Discrimination Provisions

AHPs are governed by the consumer protections within HIPAA. Under HIPAA, an individual may not be denied eligibility or continued eligibility to enroll in a group health plan based on health factors. Specifically, an AHP is prohibited from denying coverage based on:

- Health status (e.g., obesity, a physical disability, etc.)

- Pre-existing medical conditions (e.g., diabetes, high blood pressure, etc.)

- Pre-existing mental illnesses (e.g., depression, bipolar disorder, etc.)

- Medical claims history (e.g., expensive health care bills resulting from an accident)

- Medical history

- Genetic information

- Disability

HIPAA’s nondiscrimination rules prohibit an AHP from charging an individual enrollee higher premiums due to health factors. Likewise, the AHP benefits cannot be limited or excluded for an individual enrollee based on health factors.

Improvement Details for Employer Groups

Under current law, for a group of small businesses (50 or fewer employees) to form a single large group health plan, the group must qualify as a bona fide group or association of employers as defined in DOL guidance. If the employer group is not “bona fide,” each business within the group will be treated independently by regulators and forced into the more expensive small group market.23 Current bona fide requirements exclude employer groups that lack a narrowly defined professional commonality. Hence, a group of carpentry firms may qualify as bona fide, but a homebuilder group composed of carpenters, electricians, plumbers, and painters would not. Since considerable scale is needed to extract health care price concessions, regulatory betterments should (1) broaden the commonalities by which sizable employer groups may grow and (2) allow associations to form based on a shared need for affordable health insurance without this motivation invalidating their satisfaction of other bona fide requirements.

With respect to the first issue, federal policymakers should expand bona fide associations to encompass the government’s existing North American Industry Classification System.24 In addition, associations that combine a valid professional grouping with secondary membership considerations (e.g., minority-owned, veteran-owned, carbon-zero, etc.) should be permitted.

Federal policymakers should also consider groups of employers that do not share the same industry, trade, or profession as bona fide, provided that the group:

- Has been actively in existence for at least two years Was formed and maintained in good faith for purposes other than providing medical care through the purchase of insurance or otherwise

- Does not condition membership in the group on any health-status-related factor relating to any individual (including an employee of an employer member of the group or a dependent of an employee)

- Makes health coverage through the AHP available to all employer members of the group regardless of any health-status-related factor relating to its employer members (or individuals eligible for coverage through an employer member)

- Does not provide health coverage through the AHP to any individual other than an employee of an employer member of the group

Improvement Details for Gig Workers

Currently, a group or association is not considered bona fide if it includes self-employed individuals (e.g., gig workers). Gig workers are sole proprietors representing a sizable portion of the workforce, but one in four gig workers is uninsured. Given that a gig business operates simultaneously as employer and employee, gig workers should be allowed to access large group health coverage through an AHP, provided that:

- The group/association permits sole proprietor membership

- The gig workers satisfy the association’s membership criteria

- Each gig worker’s labor represents a true business as evidenced by at least 40 hours of gig work per month

This combination of individuals and employers within a single merged market is not novel. For example, in 2022 the government approved Maine’s 1332 waiver request for the merger of their ACA individual and small group markets.25 In the waiver, Maine justified the merger request by the premium reductions afforded by the merger as well as Massachusetts ’operation of a merged since 2007.26

Guidance for AHPs Wanting to Self-Insure

While fully insured AHPs have been a reliable feature of employer insurance for decades, self-insured versions have had a more spotty record, and there have been instances of insolvencies due to inadequate funding. It should be noted that self-insurance, otherwise known as self-funding, isn’t an inferior coverage model. Self-insured group health plans cover 36 million Americans (2019) and hold more than $102 billion in assets.27 In addition, mixed insurance models combining self-funding with insurance provide health benefits to another 28 million Americans.28 However, given that self-insurance is not the right option for many employer groups, it is recommended that federal policymakers should:

- Refrain from new AHP regulation that directly preempts state laws and regulation developed over decades to govern self-insured health plans (including reserve and contribution requirements), as these rules reflect individual state experience with self-funding arrangements

- Encourage a “level-funded” plan (with specified consumer protections) for two years prior to pure self-funding for new AHPs with no prior plan history. This would allow the AHP to collect meaningful claims data while eliminating health plan insolvency risks during this period

- Claims data analysis provides cost-savings opportunities as well as a sound actuarial basis for self-funded premium setting. Claims data can also reveal costly pricing differences inside a provider network that can be corrected alongside overbilling and inappropriate medical utilization. Some studies have found some form of error in four out of five medical bills, including errors that can inflate medical costs

- Require both “specific” and “aggregate” stop-loss insurances for AHPs committed to self-funding in order to protect these AHPs from medical claims in excess of actuarial projections. Specific stop loss is insurance for excessive medical claims of a single plan participant; aggregate stop loss insures excess claims for the group.

Anti-Fraud and Good Governance Provisions

Current federal regulation seeks to prevent AHP fraud by requiring the employers sponsoring an AHP to “control” the health plan in form and substance. Most if not all states include similar “control” requirements. Here, the employer group must establish a governing board with bylaws or other similar indications of formality. A majority of the board members must be made up of the group’s employer members participating in the plan that are duly elected by each participating employer member casting one vote during a scheduled election. Importantly, this board is considered a “fiduciary” and is required to operate the plan solely in the interests of participants and beneficiaries. No amounts paid into the plan by participating employer members and their employees may ever revert back to an employer member, a board member, a service provider, or any other third-party entity. To further protect the new AHP market, the DOL should:

- Allocate sufficient resources to identify and prosecute bad actors entering the market

- Establish penalties to deter those who would make false compliance representations within the improved AHP market

Federal policymakers should also update marketing rules to deter bad actors from entering the new market. If an AHP uses a third party for marketing, the AHP should be held responsible for advertisement accuracy.

Additional Guidance

The brief period of AHP reform in late 2018 through early 2019 demonstrated small employers’ health coverage strategy. Contrary to what the critics suggested, the new AHPs offered comprehensive major medical coverage, and that trend persists in today’s legacy AHP market. In many cases, current AHP coverage is more comprehensive than ACA-compliant “small group” and “individual” market plans. In addition, AHPs offer broader “health care provider networks” relative to many existing ACA small group and individual market plans and are priced at an “actuarially fair premium” for both young and old participants. AHPs are also subject to specific rules that prevent them from discriminating against individuals/employees based on health conditions. Most importantly, AHPs are prohibited from denying people coverage if they have pre-existing conditions.

However, in certain cases, organizations offering benefits through what they may call AHPs may not necessarily provide comprehensive major medical coverage (e.g., the arrangement is offering limited-benefit-type coverage such as indemnity, disability, or specified disease coverage). In these cases, the AHP should be required to explain clearly that its benefits are considered “excepted benefits” or other limited benefit designs—not major medical coverage—so there is no confusion among employees regarding what medical services are insured.

Much of what has been discussed in this brief are improvements to the law that can be performed through agency-level regulatory updates. Congress can take legislative measures to codify these improvements into law to protect the long-term health and stability of the AHP market. In addition, Congress may wish to consider codifying additional changes such as:

- Allowing an AHP to prevent a business from rejoining the AHP for two years after leaving the plan. This would discourage businesses from trying to “game” AHPs by leaving when medical claims are anticipated to be low and returning when they expect medical claims to rise.

- Allowing an AHP to establish base premium rates formed on an actuarially sound, modified community rating methodology (that considers the pooling of all plan participant claims) and use each employer’s specific risk profile to determine the employer’s contribution rates for its share of the AHP premium (by actuarially adjusting above or below the established base premium rates).

Among the benefits of congressional legislation (as opposed to agency rule-making alone) is the stability it communicates to the AHP market. Organizations would invest technology and marketing in the improved AHP market if there is not the fear of their capital being lost. If AHP improvements rest solely on regulation, they may be reversed quickly by a later administration.

Key Issues Raised by Critics

Critics of AHPs have rejected entering into a dialogue on the reform and betterment of the AHP market despite the continued decline of the “small group” market, unpopular consumer mandates, and escalating government spending. Unfortunately, these critics have:

- Ignored the financial stability of fully insured and level-funded AHPs and implied that all AHPs have the solvency risks that can attend self-funded plans lacking adequate cash reserves and stop loss

coverage - Obscured the material differences between third-party-controlled Multiple Employer Welfare Arrangements (MEWAs) and employer-controlled association health plans

- Concealed that AHPs are an instrument for small businesses to access quality and affordable large group health coverage while incorrectly arguing that AHPs are an “end run” around the ACA

- Disregarded five decades of state and federal laws that have been developed to improve oversight of AHPs

- Misrepresented AHP premium savings as possible only through younger and healthier risk pools.

The brief period of September 2018 through March 2019—during which several of the regulatory changes outlined in this brief were allowed in the market before legal challenges suspended their operations—saw AHP premium savings reaching into double digits. These savings materialized without the market segmentation and adverse individual and small group market effects that critics claimed would occur. In reality, in the absence of these improved AHPs, the small group health insurance market has continued to decline. In 2022, two-thirds (68.1 percent) of private sector firms (with fewer than 50 workers) did not offer health insurance.29 A study by the Commonwealth Fund found that enrollment in the small group health insurance market declined over 27 percent, from 18.1 million enrollees in 2012 to 13.1 million by 2018.30 If the existing small group insurance market was an economical and compelling solution for small businesses, how do we explain these statistics?

This policy brief promotes AHP changes to benefit small businesses and welcomes debate on the merits of its proposals. Unfortunately, some critics refuse to discuss improvements in good faith. Instead, their efforts focus on smearing AHPs and associating them with every historical MEWA violation, even in cases where the MEWA violation concerned welfare benefits that were neither AHPs nor major medical plans.

About the Author

This policy brief was authored by Kev Coleman. Mr. Coleman combines years of health care research with experience in health care technology design and implementation.

Special Thanks

The author thanks Christopher Condelucci for his helpful review and comments.

Footnotes

See also:

- The Employee Retirement Income Security Act of 1974 (ERISA)

- The Health Insurance Portability and Accountability Act of 1996 (HIPAA)

- The Civil Rights Act

- The Women’s Health and Cancer Rights Act

- The Public Health Service (PHS) Act

- The Mental Health Parity and Addiction Equity Act of 2008 (MHPAEA)

- The Genetic Information Nondiscrimination Act

- The Affordable Care Act

- The Consolidated Omnibus Budget Reconciliation Act of 1985 (COBRA)