On September 8, 2023, Paragon Health Institute submitted a public comment to the Administrator of the Centers for Medicare and Medicaid Services (CMS), The Honorable Chiquita Brooks-LaSure. The letter is signed by Paragon’s Brian Blase and Theo Merkel, and urges CMS to “modify its proposed remedy for the 340B drug payment policy struck down by the U.S. Supreme Court in American Hospital Association v. Becerra, 142 S. Ct. 1896 (2022).”

Dear Administrator Brooks-LaSure,

We are submitting for your consideration this comment letter urging the Centers for Medicare and Medicaid Services (CMS) to modify its proposed remedy for the 340B drug payment policy struck down by the U.S. Supreme Court in American Hospital Association v. Becerra, 142 S. Ct. 1896 (2022). While we support CMS’s proposal to adhere to the Medicare Outpatient Prospective Payment System’s (OPPS’s) budget neutrality requirements, the proposed approach of offsetting only $7.8 billion and doing so over a 16-year period would create more room for imprecision and uncertainty while straining federal budgetary resources.

Specifically, we recommend that CMS (1) increase the budget neutrality adjustment for OPPS non-drug items and services and (2) apply it over a shorter time frame. Furthermore, we believe CMS should pursue regulatory reforms to lawfully adjust Medicare payments for 340B-acquired drugs in alignment with the Supreme Court’s ruling by using survey data on 340B hospital acquisition costs.

Paragon Health Institute is a nonprofit, nonpartisan health care policy think tank dedicated to empowering patients and reforming government programs. Our analysis draws on the experience of a diverse range of experts, including former federal officials and academic researchers.

I. Problems with the Proposed Remedy

We agree with CMS’s proposal to apply budget neutrality adjustments to its proposed remedy. This appropriately aligns with OPPS policies required under Sections 1833(t)(9)(B) and (t)(14)(H) of the Social Security Act and would reduce the fiscal burden of the 340B remedy on the Medicare program. We are not raising objections to the proposed $9.0 billion lump-sum repayment to 340B hospitals.

However, we believe CMS’s proposed approach for applying the budget neutrality adjustment is flawed for the reasons outlined below.

1. CMS’s Proposed Offset Time Frame Increases Imprecision and Uncertainty

CMS proposes to offset the budget neutrality adjustment for the 340B provisions of the 2018 rule from CY 2025 through CY 2040, a 16-year period. As CMS acknowledges in its 340B remedy proposed rule, recouping payments over this time frame creates the risk of imprecision in how its payment reductions apply. Specifically, CMS states:

We are aware that, depending on how a hospital’s future mix of drug and non-drug services compares to its past mix of drug and non-drug services, as well as any absolute growth in a hospital’s non-drug services, some hospitals may ultimately receive slightly more (or less) of a payment reduction than the payment increase they received in CY 2018 through CY 2022. But there is often some imprecision inherent in budget neutrality calculation, and the alternative would require that we recalculate the additional amount that each hospital received under the prior policy and then apply a specific reduction to that hospital’s future non-drug service payment rates to offset that amount. That… would impose significant burdens and payment delays for 340B providers…. In addition, it would be administratively unworkable to tailor individual payment reductions for each of the thousands of impacted hospitals for over a decade and a half, meaning we would likely need to collect a lump-sum budget neutrality recoupment. That would impose all the burdens of an up-front budget neutrality recoupment we decided against proposing.1

CMS is correct that some imprecision in calculating budget neutrality adjustments is unavoidable and that the alternatives described in the above passage would be administratively difficult. But these are not the only alternatives available. CMS unnecessarily exacerbates such imprecision by choosing to recoup budget neutrality payments over a 16-year period rather than a shorter time frame. A longer time frame increases the chance that the relative and absolute amounts of non-drug services furnished by hospitals will deviate from what they were under the original budget neutrality adjustment and that the magnitude of these deviations will increase. This widespread imprecision in payment policy over an extended time would economically distort the health care system.

Choosing a 16-year recoupment time frame is motivated by CMS’s desire to reduce the costs borne by hospitals in any one year. However, CMS does not provide analysis in its proposed rule justifying 0.5 percent per year, as opposed to some other amount, as the appropriate adjustment level for OPPS non-drug items and services. There are several reasons to consider higher annual offset levels. First, the original budget neutrality adjustment finalized in the 2018 rule increased payment for OPPS non-drug items and services by 3.19 percent per year, over six times higher than the adjustment proposed by CMS. Second, Part B reimbursement of hospitals has grown at a rate of 5 percent per year on average between 2017 and 2021 (roughly 4 percent when excluding spending on separately payable drugs under the OPPS).2 One recent study also found that hospitals’ operating margins reached an all-time high during that time, and most did not experience

financial distress.3

2. CMS’s Proposed Payment Offsets Strain the Federal Budget

The budget neutrality adjustment proposed by CMS also negatively impacts the Medicare program’s finances to an unnecessary extent due to its amount and its time frame. Given that Part B benefits are the fastest growing component of Medicare expenditures, the program as a whole will increasingly rely on transfers from the Supplemental Medical Insurance Trust Fund, which in turn will divert general revenues from other federal programs and increase the federal debt burden. This is the reason why the Medicare trustees have issued a funding warning six years in a row and a determination of excess general revenue funding for Medicare seven years in a row.4

CMS provides several reasons in its 340B remedy proposed rule for why the amount owed to 340B hospitals exceeds the amount offset by the original budget neutrality adjustment from 2018 to 2022. We are not disputing any of these reasons. However, the decision to recoup only the original budget neutrality payments leaves a fiscal imbalance. Under CMS’s proposed remedy, 340B hospitals would receive a total of $10.5 billion in repayments from the federal government ($9.0 billion in lump-sum repayments and $1.5 billion in already-reprocessed claims from January 1 to September 27, 2022), but the federal government would recoup only $6.2 billion. (The remaining $1.6 billion would go to beneficiaries in the form of reduced cost-sharing.) This arrangement would amount to $4.3 billion in excess payments from taxpayers to hospitals. That is, despite CMS’s stated goal of “turning back the clock,” its proposed remedy leaves taxpayers $4.3 billion worse off than they would have been if its 340B policy had not been enacted.5 This does not fulfil the purpose of the OPPS budget neutrality adjustment, which, as CMS notes in its proposed rule, is to protect the public and beneficiaries by limiting Part B expenditures, which come mostly from tax and premium dollars.6

The disparate time periods for the lump-sum repayment and the budget neutrality adjustment also strain the federal budget for several reasons.7 First, numerous exogenous developments or shocks could occur over a 16-year time frame that would undermine the recoupment of $7.8 billion during that period. For example, a major recession, pandemic, or natural disaster could compel CMS or Congress to apply regulatory flexibilities to health care providers that would disrupt the recoupment process. A longer time frame therefore decreases the probability that CMS will successfully offset the full $7.8 billion as proposed. This also increases policy and business uncertainty for health care providers.

Second, the negative payment balance from this remedy would be larger in the near future than in the latter years, since the lump-sum payment would be offset over time. Since Part B expenses mostly come from general revenues, that means that this remedy would contribute to the federal debt in the short run. Interest payments on this debt would “lock in” its impact on the budget, and over the next decade such payments would exceed the preceding 50-year average as a percent of gross domestic product.8 Continued interest rate hikes by the Federal Reserve would exacerbate this situation.

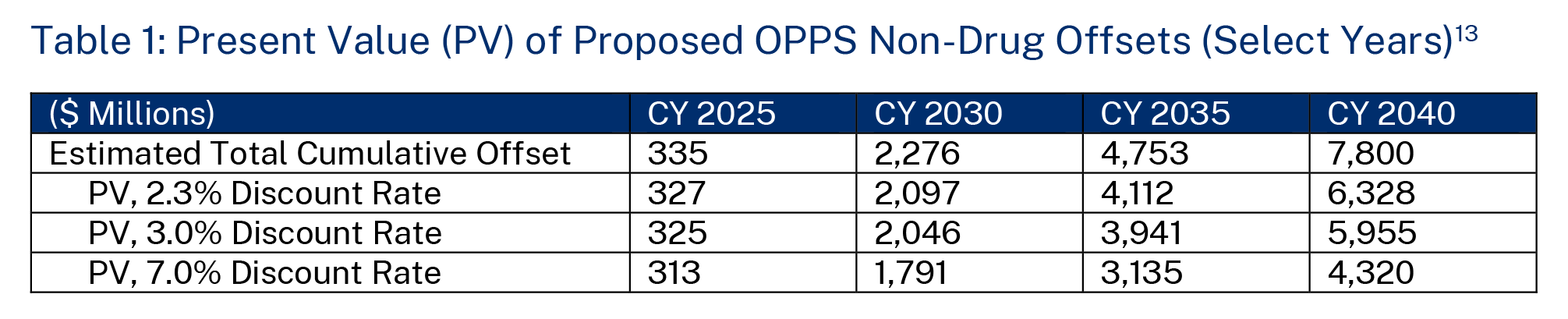

Finally, the disparate time periods further worsen the proposed remedy’s budgetary impact because each dollar of costs from the lump-sum payment will be more valuable than each dollar offset in future years due to the time-value of money. CMS does not discuss in its proposed rule whether its estimated budget neutrality adjustments are inflation-adjusted, nor does it offer analysis using discount rates. Guidance from the Office of Management and Budget (OMB) generally requires agencies to consider both factors in regulatory analysis, as “benefits or costs that occur sooner are generally more valuable.” Furthermore, “[b]enefits and costs do not always take place in the same time period. When they do not, it is incorrect simply to add all of the expected net benefits or costs without taking account of when they actually occur. If benefits or costs are delayed or otherwise separated in time from each other, the difference in timing should be reflected in [the agency’s] analysis…. When, and only when, the estimated benefits and costs have been discounted, they can be added to determine the overall value of net benefits”9 Stipulating that CMS’s regulatory impact analysis uses real rather than nominal dollars, which is particularly important in the recent high inflation environment, the long time frame of budget neutrality adjustments means that the present value (PV) of the funds that CMS expects to recoup is lower than the full $7.8 billion adjustment proposed. OMB generally requires agencies to report results using discount rates of 3 percent and 7 percent, and although this is not typical practice in CMS’s Medicare rulemaking, it is essential that it do so when it specifically proposes policy changes that extend over a longer time period.10

In Table 1 below, we compare CMS’s estimated cumulative budget neutrality adjustments from the proposed rule with the PV based on these two discount rates as well as the intermediate real-interest rate of 2.3 percent used in the 2023 Medicare trustees report.11 Based on this analysis, assuming no inflation adjustment is necessary, the PV of the total recoupment amount ranges from $4.3 billion to $6.3 billion rather than $7.8 billion. In terms of the net impact on federal payments (that is, subtracting the estimated impact on beneficiary cost-sharing), this budget neutrality adjustment would save $3.5 billion to $5.1 billion versus the $9.0 billion proposed lump-sum repayment and the $1.5 billion already paid out in 2022—amounting to a PV of $5.4 billion to $7.0 billion in excess taxpayer expenses.12

II. Recommended Modifications to the 340B Remedy

To address the problems with CMS’s proposed 340B remedy outlined in the previous section, we recommend that CMS modify the budget neutrality adjustment. We outline a few approaches to this below. In the next section, we also summarize the continued need to reform Medicare payment for 340B drugs and offer further recommendations for future CMS rulemaking.

First, CMS should increase the total amount of the budget neutrality adjustment for OPPS non-drug items and services, resulting in less federal payments and beneficiary cost-sharing than under the proposed remedy. While the budget neutrality adjustment from the 2018 rule increased payments for OPPS non-drug items and services by $7.8 billion, several factors—including CMS’s coverage of 2018-2022 beneficiary cost-sharing in its lump-sum repayment to 340B hospitals and its underestimate of the total amount of payment reductions to 340B hospitals under the 2018 rule—mean that the payment adjustment would not equal the increase in federal payments under the proposed remedy, and therefore the net impact would not be budget neutral. This is not consistent with the statutory requirements for budget neutrality in the OPPS under Sections 1833(t)(9)(B) and (t)(14)(H) of the Social Security Act. Instead, CMS should increase the total budget neutrality adjustment to $10.5 billion, amounting to about $8.4 billion in reduced federal payments and about $2.1 billion in reduced beneficiary cost-sharing for OPPS non-drug items and services. If CMS chooses to retain an extended recoupment time frame, such as the 16-year period proposed, the adjustment should have a PV of $10.5 billion. Given that CMS solicited comment on its proposed interpretation of its “budget neutrality obligations, equitable payment authorities, and recoupment authority,” we believe that finalizing our recommended policy would represent logical outgrowth from CMS’s proposed rule.14

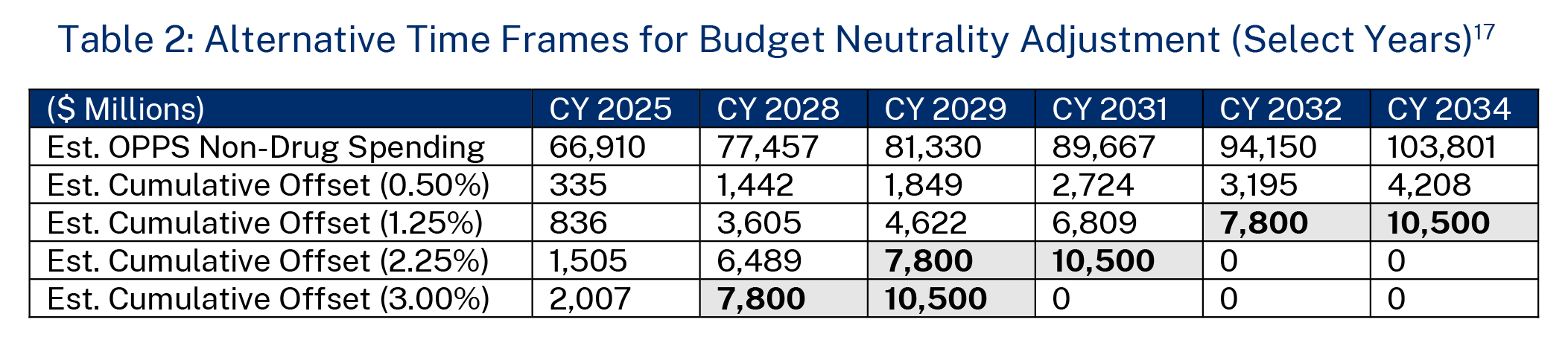

Second, CMS should reduce the time frame over which it recoups the budget neutrality adjustment payments from the 2018 rule. There are several options that CMS could pursue. Table 2 shows three different recoupment scenarios, in addition to CMS’s proposal, with annual budget neutrality adjustments that are greater than the 0.5 percent proposed reduction in OPPS non-drug items and services. This table does not calculate PVs of the total budget neutrality adjustments in these scenarios, because these recommended recoupment time frames are shortened. Under the first scenario, where CMS finalizes a 1.25 percent annual reduction in non-drug spending, the budget neutrality adjustment is fully complete within eight years (for CMS’s proposed $7.8 billion amount) or 10 years (for our recommended $10.5 billion amount). Under the second scenario, with a 2.25 percent reduction, the recoupment period is five years under CMS’s proposed amount and seven years under our recommended amount. Finally, a 3 percent annual reduction would lead to a four-year and a five-year recoupment period, respectively. We believe any of these approaches would be preferable to CMS’s proposed time frame, but our main parameters are to at least keep the recoupment period within a customary 10-year budget window and to keep the annual payment reduction rate below 3.19 percent so as not to have the reduction in OPPS non-drug spending under the remedy be more severe than the original adjustment under the 2018 rule. 15 As CMS solicited comment “on the annual percent reduction method described [in its proposed rule] and whether an alternative … would be appropriate,” we believe that finalizing one of our recommended approaches would represent logical outgrowth from CMS’s proposed rule.16

III. The Continued Need to Reform Medicare 340B Drug Payment

Beyond the 340B remedy rule, we also recommend other regulatory reforms to address the growing cost of Part B drugs in general and overpayments for 340B drugs in particular. Specifically, we believe that CMS should again attempt to set a lower reimbursement rate for drugs acquired through the 340B program than for other drugs—below the average sales price plus 6 percent.

OPPS payment for 340B drugs is flawed. Despite 340B-covered entities receiving discounts of 25 to 50 percent on drugs, Medicare and its beneficiaries pay the same rate for these as for other drugs (there is also no legal requirement to pass along these savings to needy patients). 18 This financial incentive has contributed to the growth of 340B program participation to about 40 percent of all U.S. hospitals. 19 The share of OPPS spending going toward separately payable drugs has also increased from about 15 percent in 2014 to about a quarter in 2020 and 2021.20

Addressing this problem was a major motivation for CMS finalizing its payment adjustments for 340B drugs in the 2018 rule. This problem persists in the wake of the Supreme Court’s decision to invalidate that policy. But CMS still has options. In its decision striking down that policy, the Court said that CMS could not target payment adjustments to a subgroup of hospitals without first conducting a survey of hospitals’ acquisition costs. CMS conducted such a survey between April 24 and May 15, 2020, although it has not yet incorporated this survey into its rulemaking. 21 CMS should again attempt to adjust Medicare’s Part B reimbursement rate for 340B drugs based on the findings of this survey or conduct another survey if it determines that those findings are not a sufficient basis for doing so. While CMS may wish to avoid incurring more legal challenges, it should be able to minimize litigation risk by proceeding cautiously and in accordance with the Court’s orders.

This or another approach to adjusting Medicare payments for 340B drugs would be a good first step to broader reforms of Part B drug payment policies.22 Simply maintaining the status quo is unacceptable.

IV. Conclusion

CMS’s changes to Medicare reimbursement for 340B drugs attempted to solve real problems in terms of excessive Part B drug spending. The Supreme Court’s invalidation of that policy means that continued reforms to 340B policy are needed, and CMS should continue to explore lawful ways to exercise its authority to reduce Medicare overpayments in accordance with the Court’s guidance. This includes using existing or new data on acquisition costs to adjust reimbursement rates. In the meantime, CMS should construct an appropriate remedy to the Court’s decision. To do this, it should modify its proposed budget neutrality adjustment for OPPS non-drug items and services to (1) fully account for the total costs of lump-sum repayments to 340B hospitals and (2) take place over a shorter time frame. This would reduce imprecision in applying the adjustments and minimize fiscal pressures on the Medicare program and the federal budget.

We appreciate the opportunity to comment on this proposed rule and urge you to adopt our recommendations.

Sincerely,

Brian Blase, Paragon Health Institute

Theo Merkel, Paragon Health Institute