Brian Blase, Ph.D.

Brian Blase, Ph.D., is the President of Paragon Health Institute. Brian was Special Assistant to the President for Economic Policy…

Reforming Government, Empowering Patients

Navigation

This paper shows that from 2018 to 2023, ACA markets fared better in states allowing short-term health insurance, with higher enrollment and lower premiums, suggesting potential harm from proposed federal restrictions on these policies.

What This Paper Covers

In 2018,the Trump administration liberalized federal requirements around short-term limited-duration health insurance (STLDI). In a 2021 analysis, I found that states that maximally permitted STLDI had more favorable trends in their individual insurance market relative to states that restricted or prohibited STLDI from 2018 to 2020. Affordable Care Act (ACA) plan enrollment, insurer participation, and premium trends were all better in STLDI favorable states. This paper uses years of additional data to evaluate whether those trends continued.

What We Found

The ACA individual market,regardless of metric, has performed better in states that fully permit STLDI. Between 2018 and 2023: 1) Exchange enrollment was up 62.7 percent in STLDI favorable states, more than 13 times greater than the 4.7 percent increase in STLDI unfavorable states; 2) The number of insurers selling exchange plans in STLDI favorable states increased 105 percent, more than three times the 31 percent increase in STLDI unfavorable states; and 3) Exchange plan premiums, particularly for benchmark plans and gold plans, decreased much more significantly in STLDI favorable states.

Why It Matters

In July,the Biden administration proposed a rule to significantly reduce the allowable STLDI contract period. The rule would change the allowable initial contract period from 364 days to three months and would change the total permissible duration of a plan from three years to four months. Ifthe administration finalizes this rule as proposed, it would create numerous harms, including reducing coverage options, stripping coverage from people who get sick and lack access to other plans, and increasing the number of people without health insurance. This study suggests that the proposed federal STLDI restrictions are more likely to harm, rather than improve,the ACA market.

Policy Suggestions

This paper provides further evidence that the Biden administration should withdraw its proposed rule to restrict STLDI. The costs of such restrictions would dwarf any benefits.

The Affordable Care Act (ACA) introduced significant new federal health insurance regulations, including requirements for what plans must cover and how products must be priced. The ACA did not impose any of these regulatory requirements on short-term limited-duration health insurance (STLDI) products, preserving a long-standing exemption for STLDI from federal health insurance regulation. Because the ACA caused individual market premiums to soar, and because this coverage tended to also have high deductibles and narrow provider networks, many people started to turn to STLDI as an alternative way to be insured.

In the fall of 2016, the Obama administration finalized a rule restricting STLDI.1 The rule changed the long-standing federal rules permitting STLDI plans to last for up to 364 days, restricting the contract to just 90 days. The rule did not prevent people from renewing their STLDI plans. As the National Association of Insurance Commissioners (NAIC) wrote in a comment letter opposing the Obama administration’s proposal, this rule most harmed people who got sick during the 90-day coverage period. They would not be able to secure other plans until the next ACA open enrollment period and would likely be left with no coverage options.2 The NAIC predicted that the rule would not improve the ACA markets.

The Trump administration pursued a different health policy approach aimed at maximizing coverage options for American families. The Trump administration reversed the Obama administration’s restrictions on the duration of STLDI, restoring the initial contract period to 364 days and permitting renewals for up to three years of coverage by a plan.3 At the time, the consensus was that the Trump administration rule would make coverage available to people at half the cost of ACA plans, reduce the number of uninsured by up to 2 million people, and lead to small selection effects against the ACA that would slightly increase gross premiums (although not net premiums because of the design of the ACA’s premium tax credits).4 President Biden gave mixed signals about how he would approach STLDI. During the presidential campaign, he pledged that he would not take away private coverage from anyone.

On July 16, 2020, Biden pledged that if he became president, “If you have private insurance, you can keep it.”5 However, in a January 2021 executive order, he signaled that he would restrict STLDI.6

In early 2021, I wanted to test the hypothesis that the expansion of STLDI harmed the ACA individual market for insurance—a hypothesis that had been raised by numerous policy experts critical of the Trump administration rule.7 Roughly half of the states permitted STLDI consistent with the Trump framework, and about half the states placed restrictions on STLDI, including their prohibition. I performed a simple analysis, comparing enrollment, insurer participation, and premium trends across states. Here is what I found:

Perhaps surprisingly, it turns out that states that fully permit short-term plans have had a much more favorable experience in their individual markets since the 2018 rule took effect. States that permit short-term plans have lost fewer enrollees in the individual market, have had far more insurers offer coverage in the market, and have had larger premium reductions since the 2018 rule took effect.8

While there are some people who purchase STLDI instead of ACA individual market plans, restricting STLDI and making the coverage worse for the sick by reducing the contract period could worsen the individual market. Moreover, because STLDI plans are an alternative for some people to ACA coverage, restricting or prohibiting STLDI could reduce competitive pressure on ACA insurers to offer better plans. Here is what I wrote in the 2021 paper:

The 2018 short-term plan rule may have, in fact, helped improve the individual market. This could have occurred because short-term plans forced insurers selling ACA-compliant products to offer more attractive products because of the added competition and because people with short-term plans who got sick or injured had short-term plans pay their expenses instead of moving to the individual market to get coverage to pay their expenses.

A separate study by Mark Hall and Michael McCue, which centered on average ACA individual market risk scores, came to a different conclusion.9 A risk score is a government calculation to measure the relative medical costs expected for enrollees. Hall and McCue assessed risk score trends between enrollees in states that permitted STLDI and those states with restrictions on STLDI. According to their calculations, from 2018 to 2020, risk scores declined by 11.4 percent in STLDI unfavorable states versus 8.3 percent in STLDI favorable states. They also estimated that enrollment in ACA-compliant plans sold off the exchanges declined 4 percent in STLDI unfavorable states versus a 27 percent decline in STLDI favorable states.

I used data from healthinsurance.org to classify states as favorable and unfavorable states. STLDI favorable states permit or nearly permit STLDI consistent with the federal rules. There are two sets of STLDI unfavorable states: (1) states that permit STLDI but restrict it relative to the federal allowances, most frequently by limiting the contract duration to six months or less; and (2) states that effectively prohibit STLDI. It turns out there are 29 STLDI favorable states, eight states that permit but limit STLDI, and 13 states as well as the District of Columbia that either ban STLDI or make the regulatory climate so difficult that STLDI is not offered.10

For enrollment, I used KFF’s annual reports at the conclusion of each open enrollment period that shows the number of people by state who selected coverage through the exchanges.11 For premiums, I used KFF’s annual reports containing premium information and insurer participation in the exchanges by state.12 In addition to KFF data, I used Mark Farrah Associates (MFA) data to estimate off-exchange individual market enrollment by state.13 MFA’s data matches Kaiser’s data for on-exchange individual market enrollment and represents enrollment at the end of the first quarter of each calendar year.14 Off-exchange individual market enrollment includes grandfathered plans15 and grandmothered plans,16 although there is significant attrition in enrollment in these products over time.

A Democratic House Energy and Commerce Committee report released in 2020 estimated that upwards of 3 million people had STLDI plans at some point in 2019.17 The committee estimated this through a data collection from insurers. Unfortunately, there is not a reliable way to regularly estimate STLDI enrollment, and enrollment for STLDI has generally been unreliable and underestimated.18

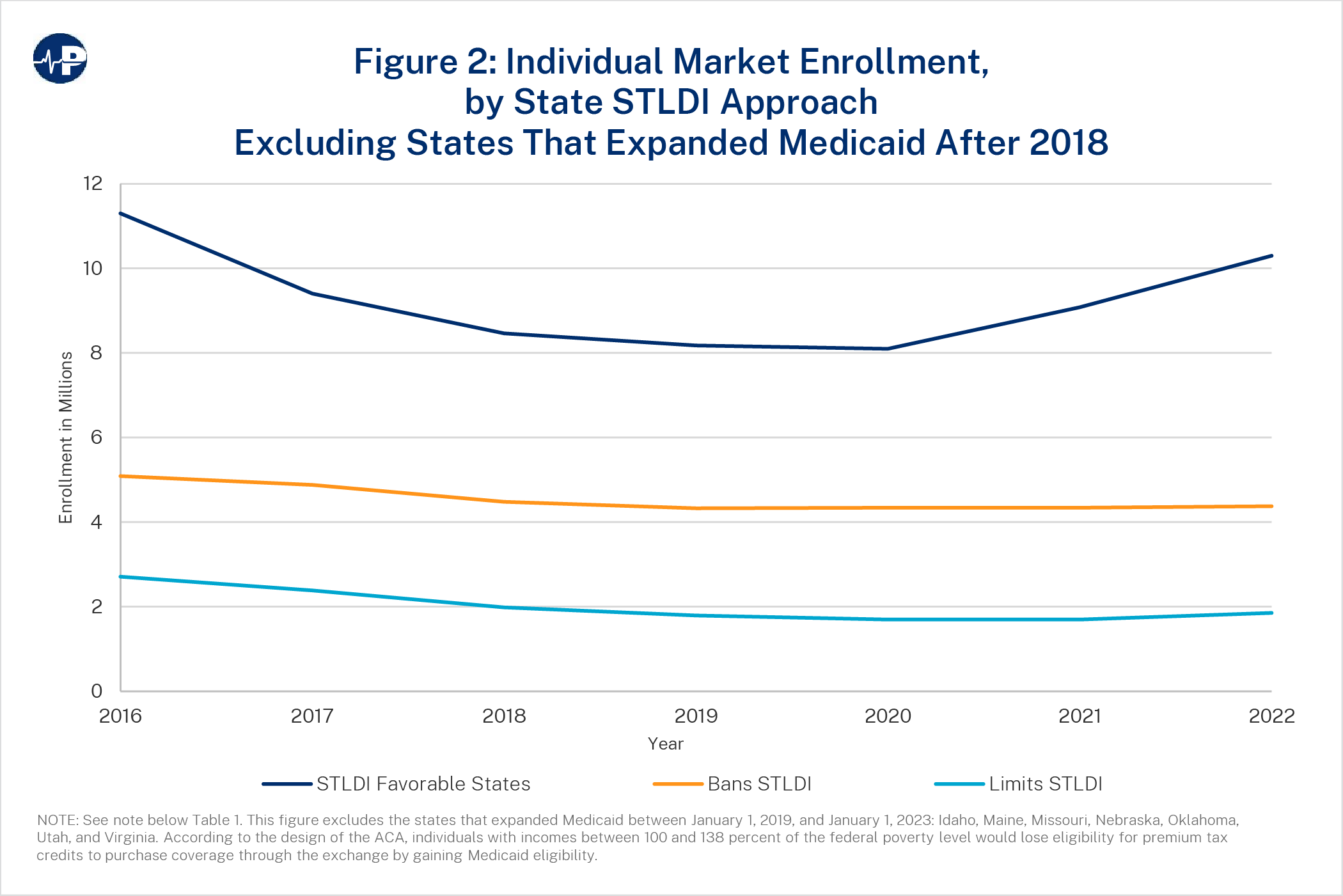

I accounted for states that expanded Medicaid between January 1, 2019, and January 1, 2023: Idaho, Maine, Missouri, Nebraska, Oklahoma, Utah, and Virginia. According to the design of the ACA, individuals with incomes between 100 and 138 percent of the federal poverty level would lose eligibility for premium tax credits to purchase coverage through the exchanges when gaining Medicaid eligibility. Thus, states that expanded Medicaid would lose enrollment in the exchanges, all else being equal, as individuals migrate from the exchanges to Medicaid.

I also checked enrollment trends using the Unified Rate Review (URR) data, as this was the source of the Hall and McCue analysis. Health insurers must submit a rate filing justification for each ACA plan they sell in the individual market. These filings facilitate a regulatory review for premium increases that meet or exceed the threshold specified in federal regulation.19 This data is publicly available for researchers to use.20 The URR data includes only ACA-compliant plans as well as grandparent plans.

Enrollment

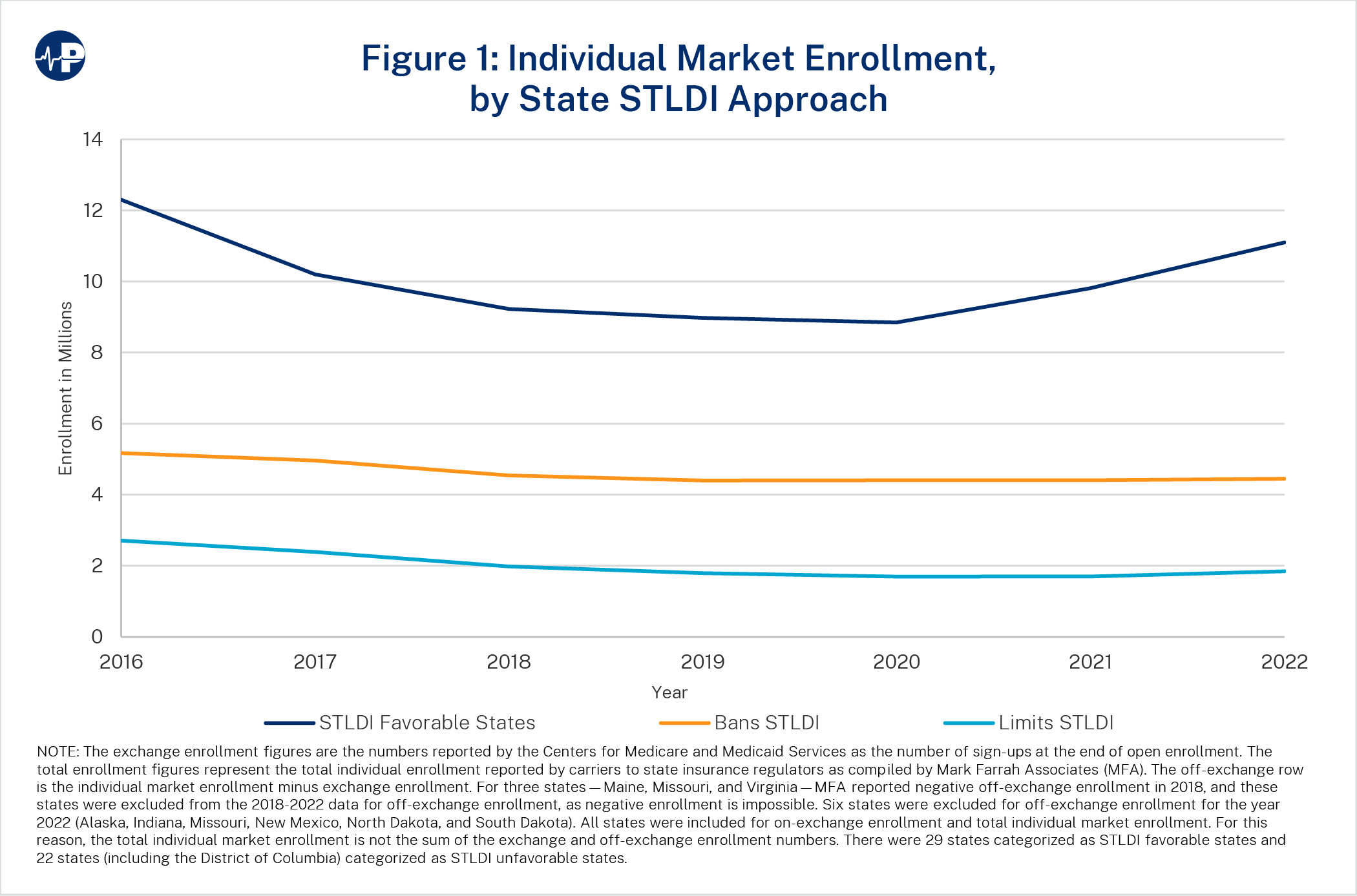

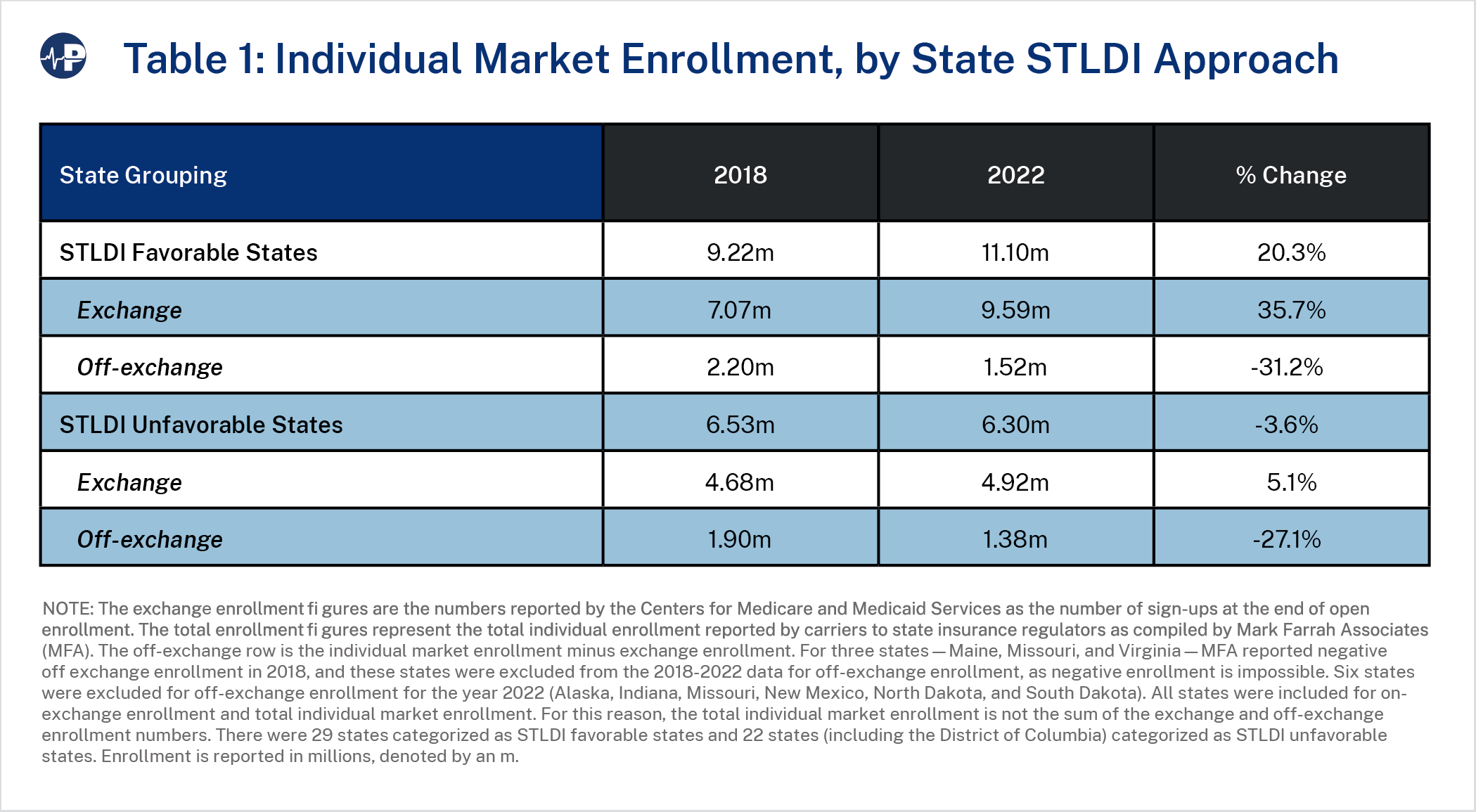

As shown in Table 1, between 2018 and 2022, individual market enrollment substantially increased in STLDI favorable states (up 20.3 percent) while slightly decreasing in STLDI unfavorable states (down 3.6 percent). Exchange enrollment increased substantially from 2018 to 2023 (exchange enrollment is available through 2023), driven by the enhanced ACA premium tax credits. However, the percentage increase in STLDI favorable states was 62.7 percent, more than 13 times greater than the percentage increase in STLDI unfavorable states (4.7 percent).

According to the MFA estimates, off-exchange enrollment dropped by similar percentages in both STLDI favorable and STLDI unfavorable states. The drop was expected, as off-exchange enrollment includes people enrolled in grandfathered and grandmothered plans, and over time people transition off this coverage, and new people are not able to enroll. Plus, the expanded subsidies make it more likely that middle-income and upper-middle-income households buy in the exchanges, as the subsidies are only available there.

As discussed below, state off-exchange enrollment are estimates. MFA estimates off-exchange enrollment by taking the difference between total individual enrollment reported by carriers and exchange enrollment reported in open enrollment period files from the Centers for Medicare and Medicaid Services as of the end of the first quarter of the calendar year. In both years, this calculation caused a few of the MFA estimates of off-exchange enrollment to be negative, and these were excluded from my analysis. The appendix contains figures that correspond to the tables. The figures show the trends over time across the three categories of states: (1) STLDI favorable states, (2) states that restrict but permit STLDI (in most cases using a six-month initial term), and (3) states where STLDI is not sold by an insurer.

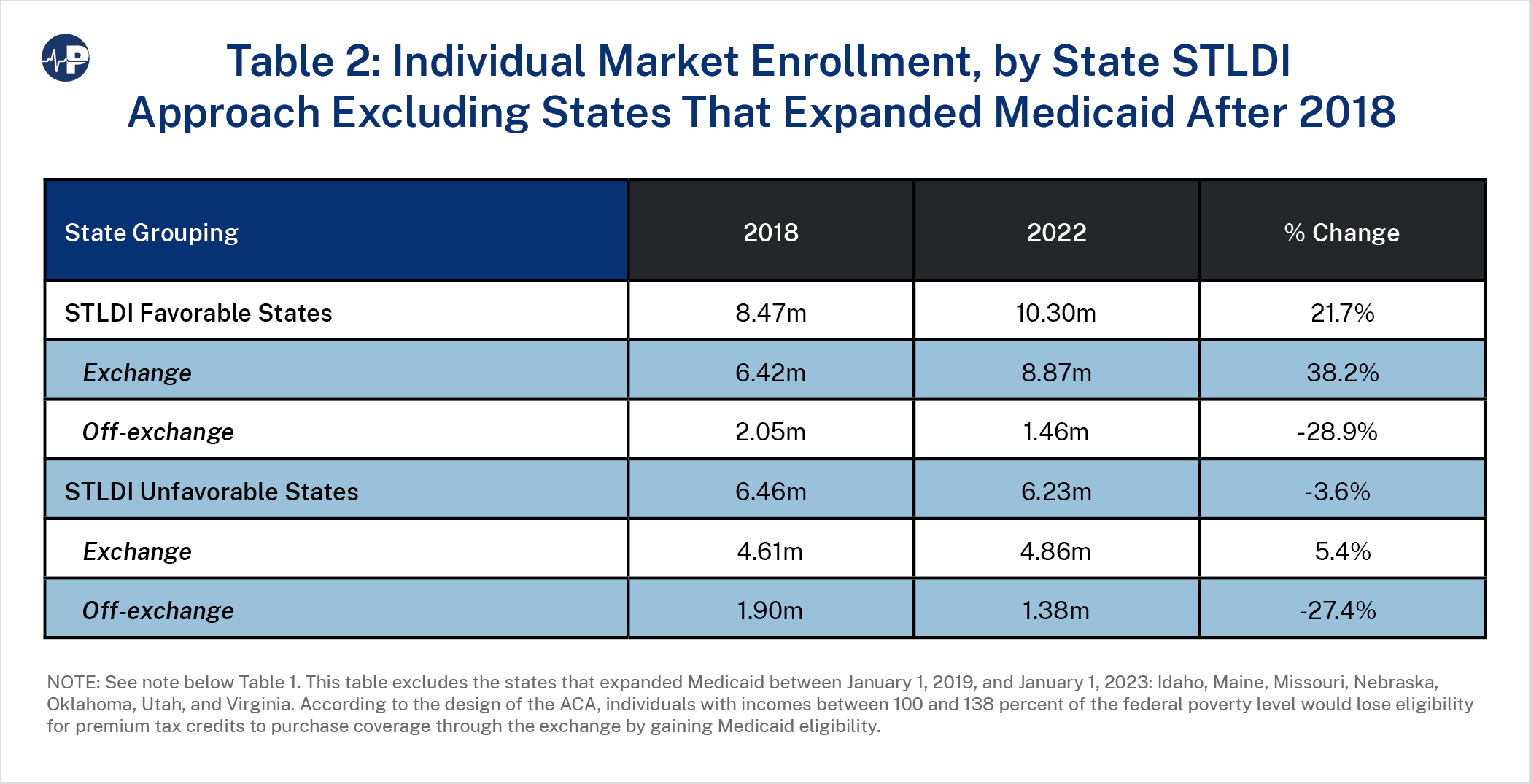

Table 2 shows the results, excluding states that expanded Medicaid during this period. Excluding these states does not significantly change the results, particularly because most of the states that expanded Medicaid during this period were relatively low population states. Overall individual market enrollment was up 21.7 percent in STLDI favorable states and down 3.6 percent in STLDI unfavorable states. As the table shows, this difference was driven by exchange enrollment, as the decline in off-exchange enrollment was similar in both categories of states.

Finally, I checked the URR data, which was utilized by Hall and McCue. Starting in 2020, URR began releasing point-in-time enrollment numbers. There is a lot of variability in these numbers from year to year, but they do show that off-exchange enrollment more than doubled in STLDI favorable states from 2020 to 2023 while declining by 40 percent in STLDI unfavorable states.21 These results cut against the findings of the Hall and McCue analysis and suggest that their conclusions are unreliable. Prior to 2020, point-in-time enrollment count was not part of the URR.

Hall and McCue relied on member month numbers.22 Using this latter methodology confirms greater attrition in the off-exchange individual market from 2018 to 2020 in STLDI favorable states. Using data from 2018 to 2023, however, reverses the trend Hall and McCue found from 2018 to 2020 and shows much better off-exchange enrollment trends in STLDI favorable states since 2018. Additionally, the trend that Hall and McCue found is not consistent with the MFA data.

Enrollment in the off-exchange individual market shows more variability, so making judgments about these enrollment patterns should be discounted. Off-exchange enrollment is subject to how insurers report information to states. Off-exchange enrollment can include ACA-compliant plans, grandfathered plans, grandmothered plans, STLDI, and health sharing ministry plans, among others. However, the exchange enrollment data is reliable. And that data clearly demonstrates that favorable state regulation toward STLDI does not harm exchange enrollment and, if anything, boosts it.

Insurer Participation

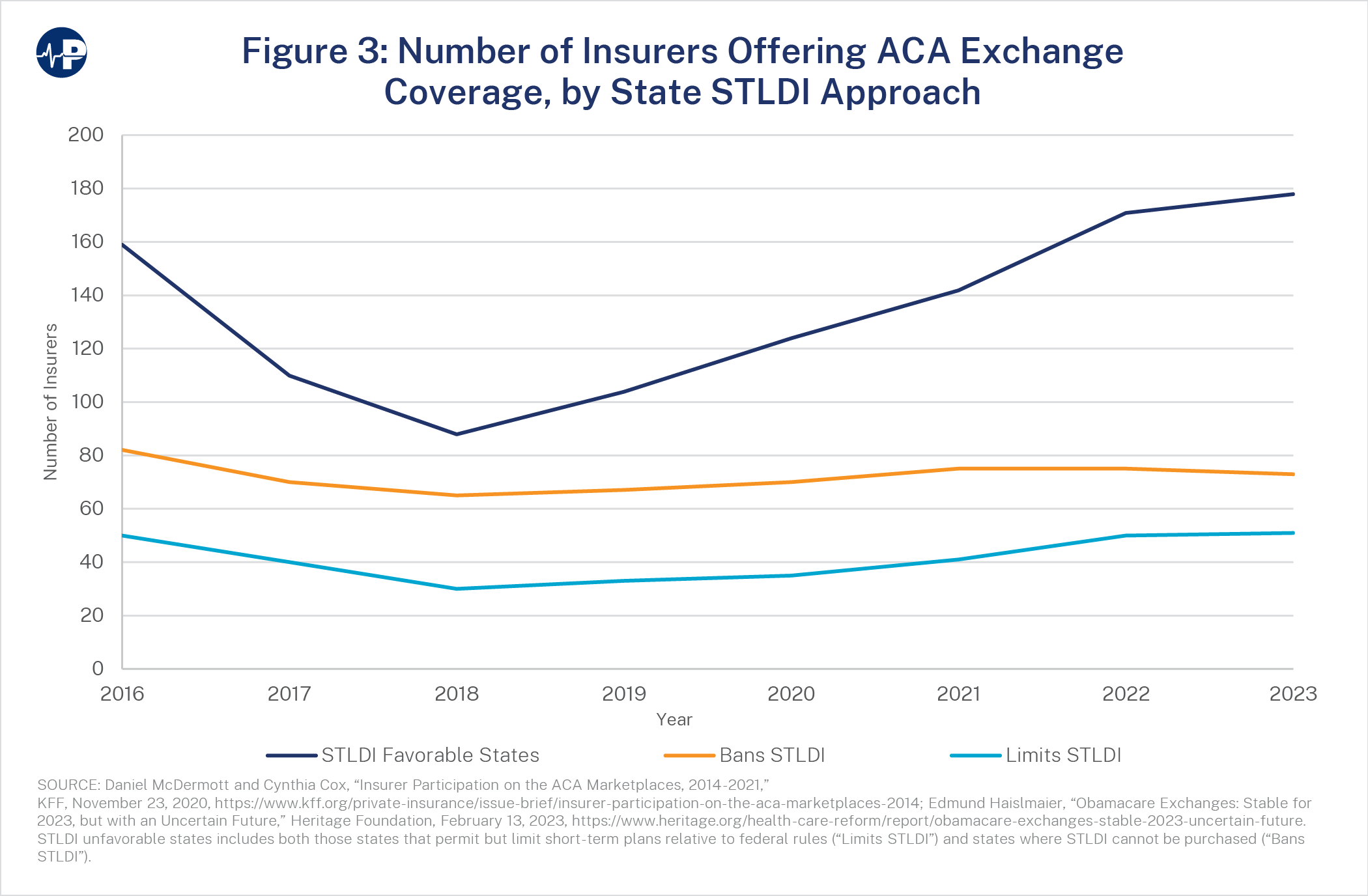

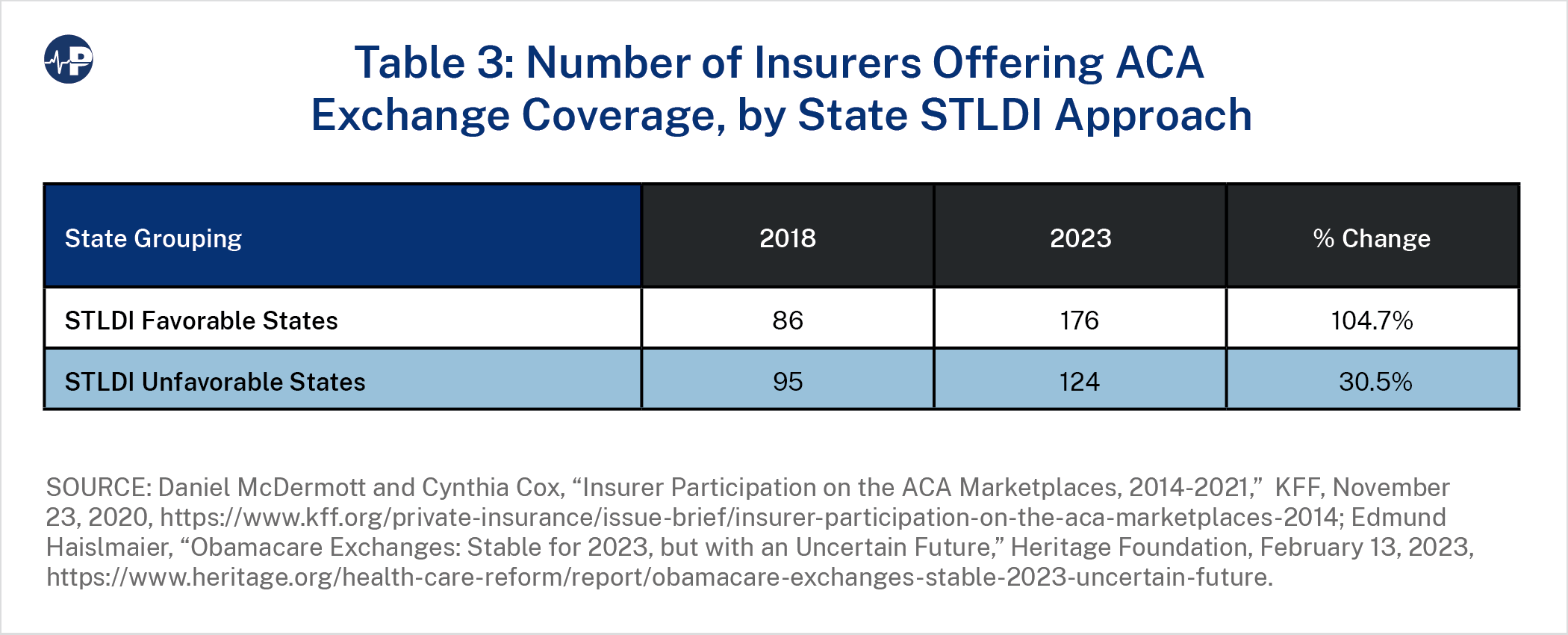

Another metric to measure the health of the individual market is the number of health insurers offering plans. Before the ACA’s rules took effect, there were 395 individual market insurers across the states.23 In 2014, that number dropped to 252, and it continued to decline through 2018 when it reached 181 insurers.24 However, since 2018, insurers have figured out how to make profits in the individual market—aided by expanded government subsidies. This came despite the elimination of the individual mandate tax penalty and the expansion of STLDI.

If the skeptics of STLDI were correct, we would expect fewer insurers to enter the exchanges in STLDI favorable states than in unfavorable states. However, the opposite happened. As Table 3 shows, the number of insurers offering ACA exchange plans more than doubled between 2018 and 2023 in STLDI favorable states, a percentage increase more than three times greater than the growth in the number of insurers offering exchange plans in STLDI unfavorable states.

Premiums

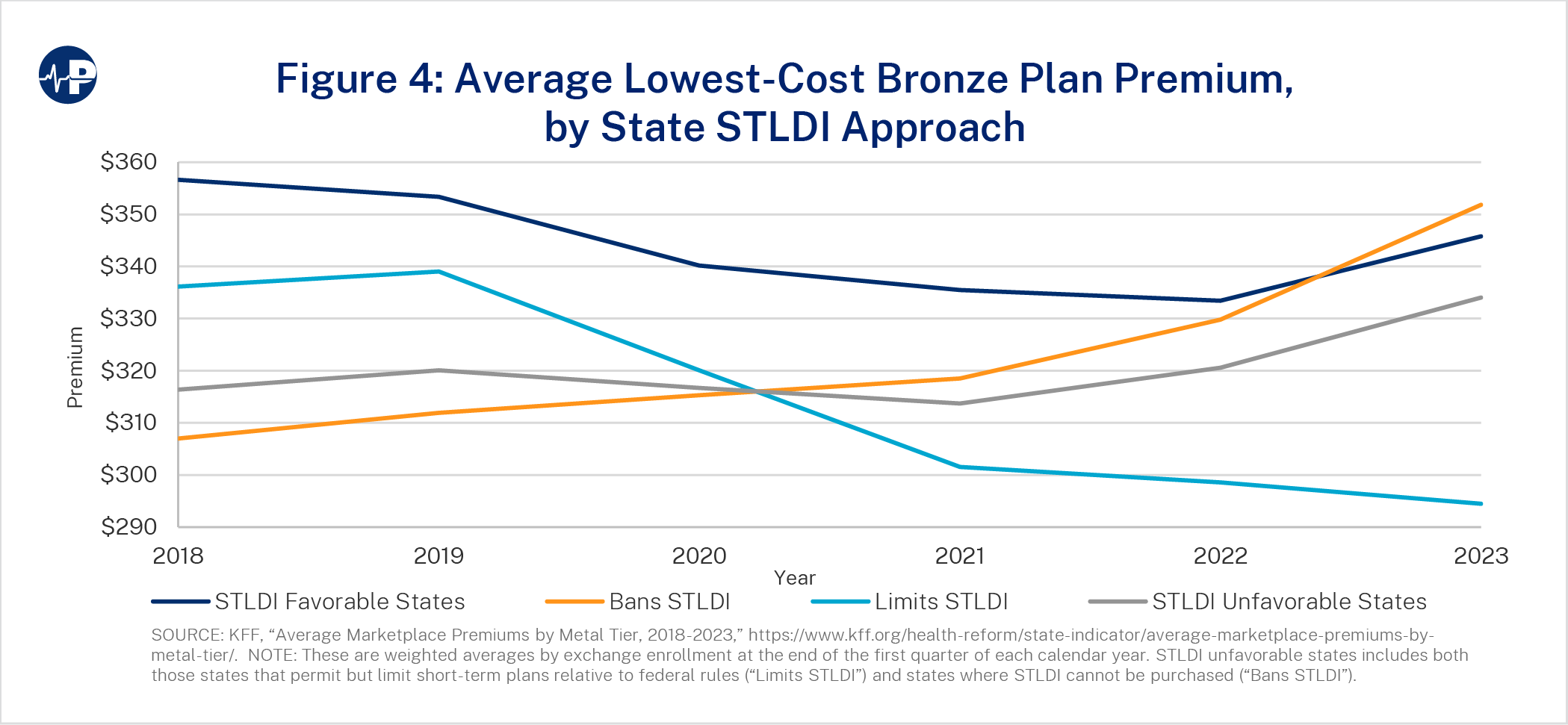

From 2018 to 2023, premiums for exchange plans generally declined. However, the premium declines were more significant across the board in STLDI favorable states. Tables 4-8 show the trends in exchange plan premiums based on state regulatory approaches to STLDI. The premiums are averages that are weighted using exchange plan enrollment across the states in those categories.

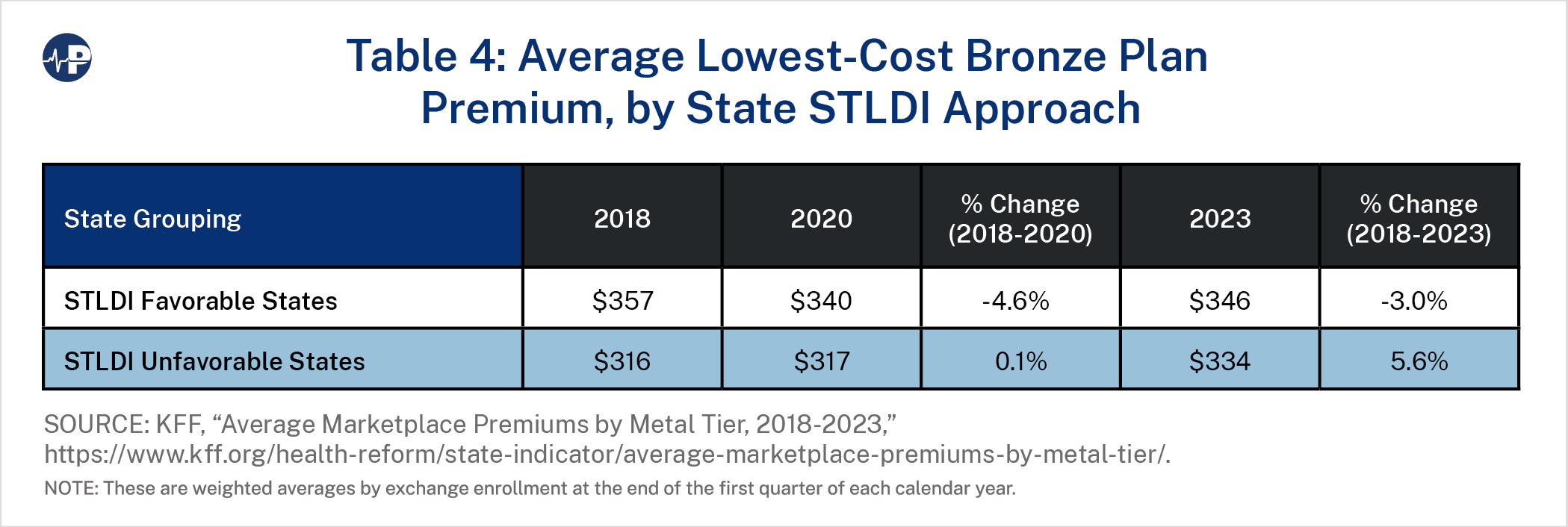

Table 4 shows the trends in the lowest-cost bronze plans from 2018 to 2020 and from 2018 to 2023 between STLDI favorable states and STLDI unfavorable states. From 2018 to 2020, premiums declined in STLDI favorable states by about 5 percent and remained roughly the same in STLDI unfavorable states. By 2023 the better premium trend continued in STLDI favorable states. However, premiums increased by about 6 percent in STLDI unfavorable states from 2018 to 2023.

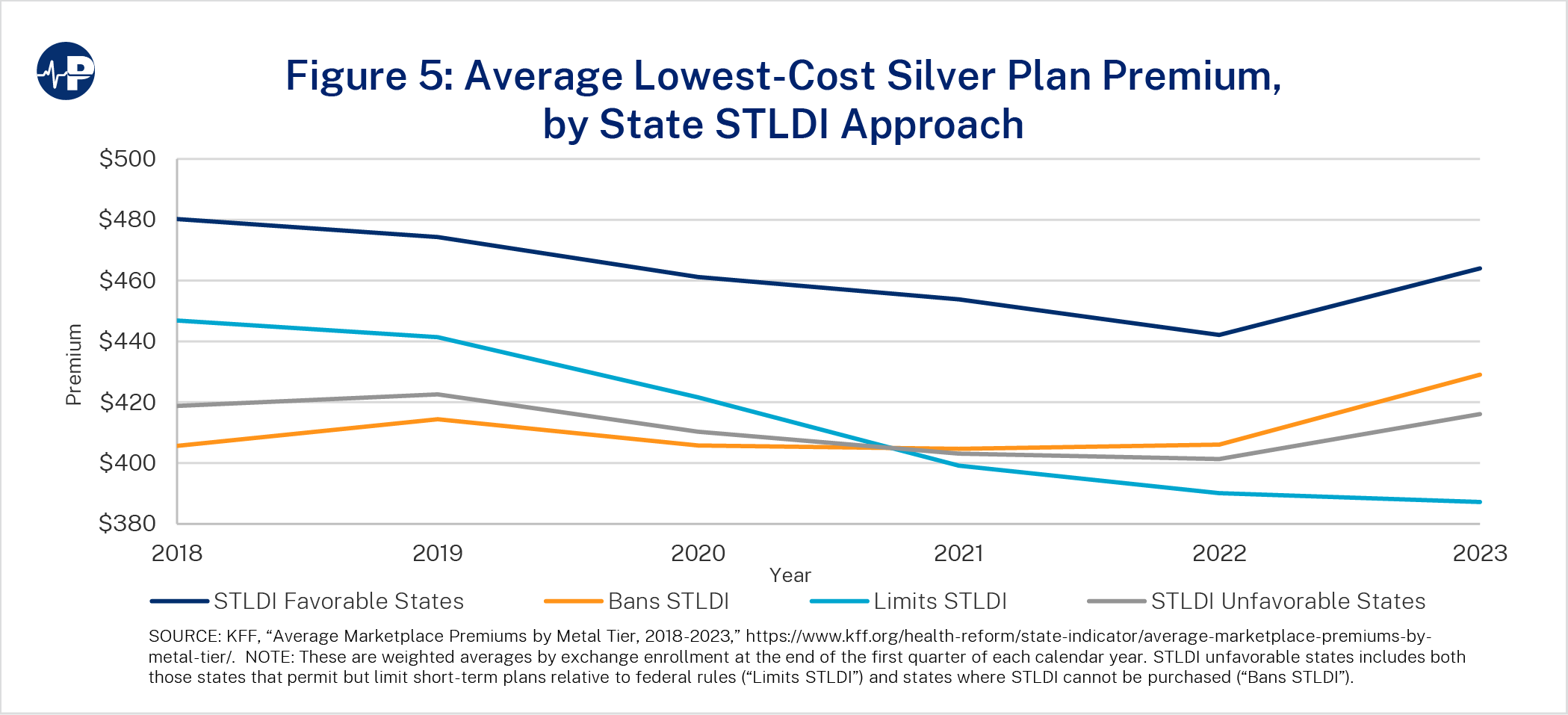

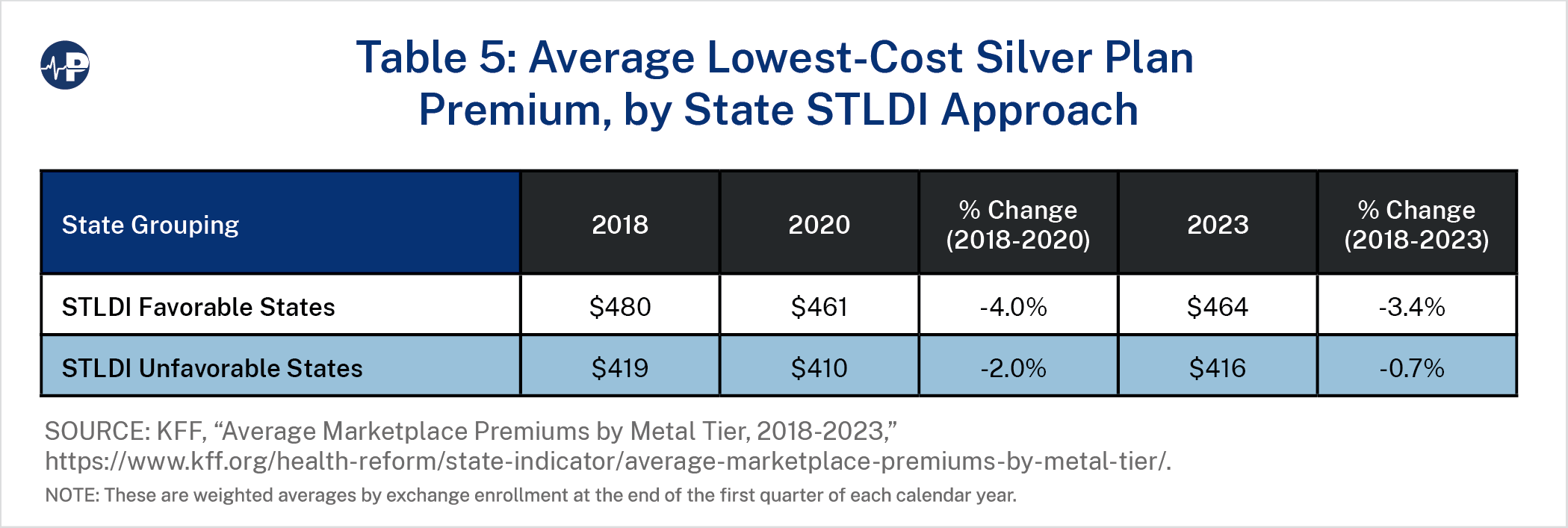

Table 5 shows the trends in the lowest-cost silver plans between STLDI favorable states and STLDI unfavorable states. From 2018 to 2020, premiums declined in both state categories by about 4 percent and 2 percent, respectively. From 2018 to 2023, the respective premium declines were 3 percent and 1 percent, again slightly more favorable trends in STLDI favorable states.

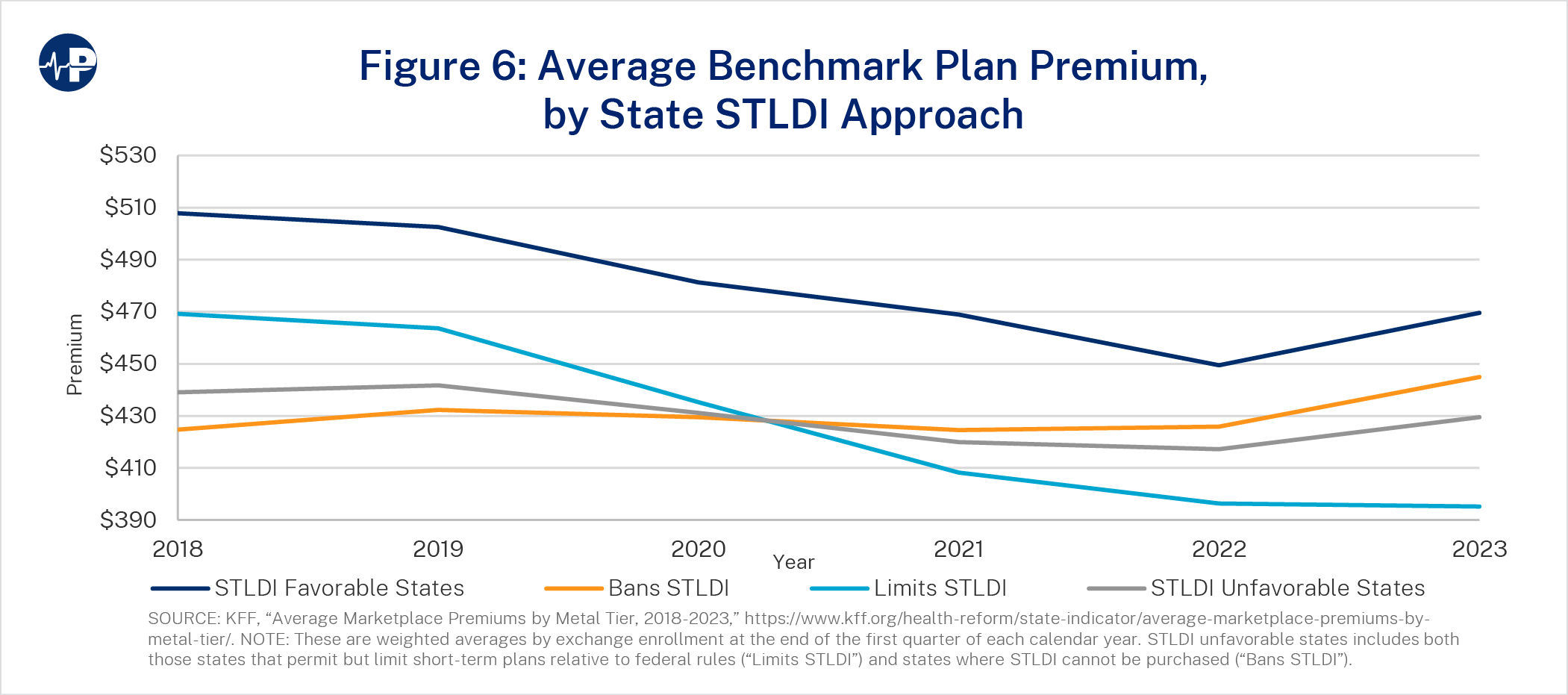

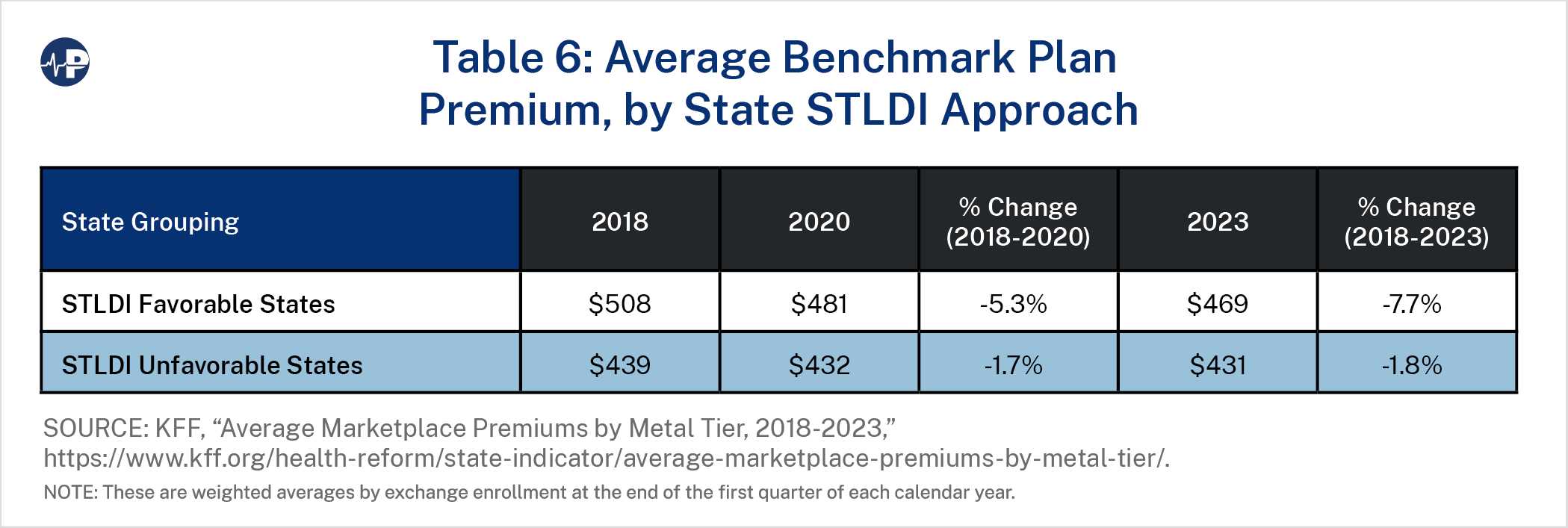

Table 6 shows the trends in the benchmark plans between STLDI favorable states and STLDI unfavorable states. The benchmark plan premium is important because it determines the amount of the premium tax credit, or the per enrollee cost that taxpayers bear to finance the subsidies. In states that restrict STLDI, benchmark premiums declined by about 2 percent from 2018 to 2020 compared to a larger 5 percent decline in STLDI favorable states. Benchmark plan premiums continued to decline in STLDI favorable states through 2023 relative to STLDI unfavorable states. Thus, this evidence suggests that more favorable STLDI rules do not increase the fiscal cost of the ACA by raising the benchmark premium.

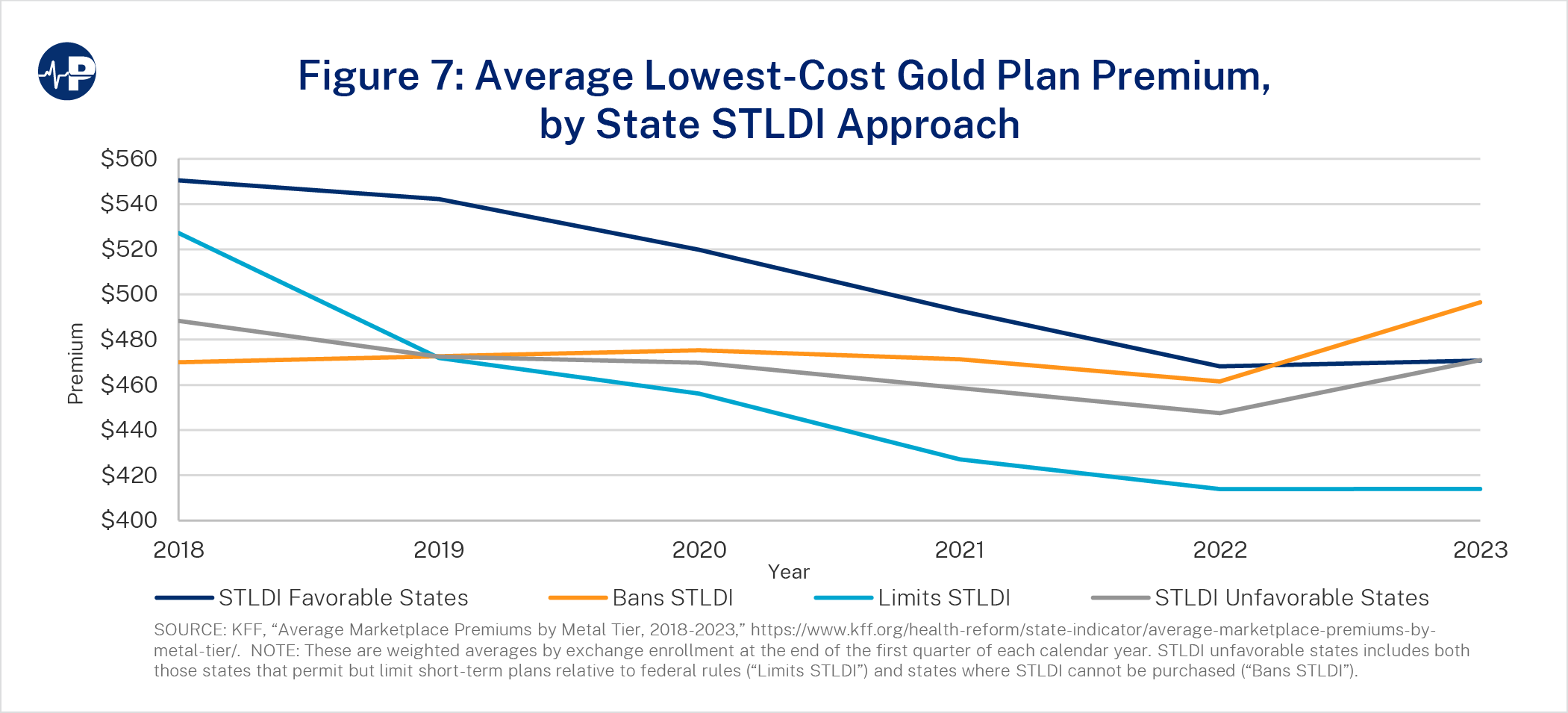

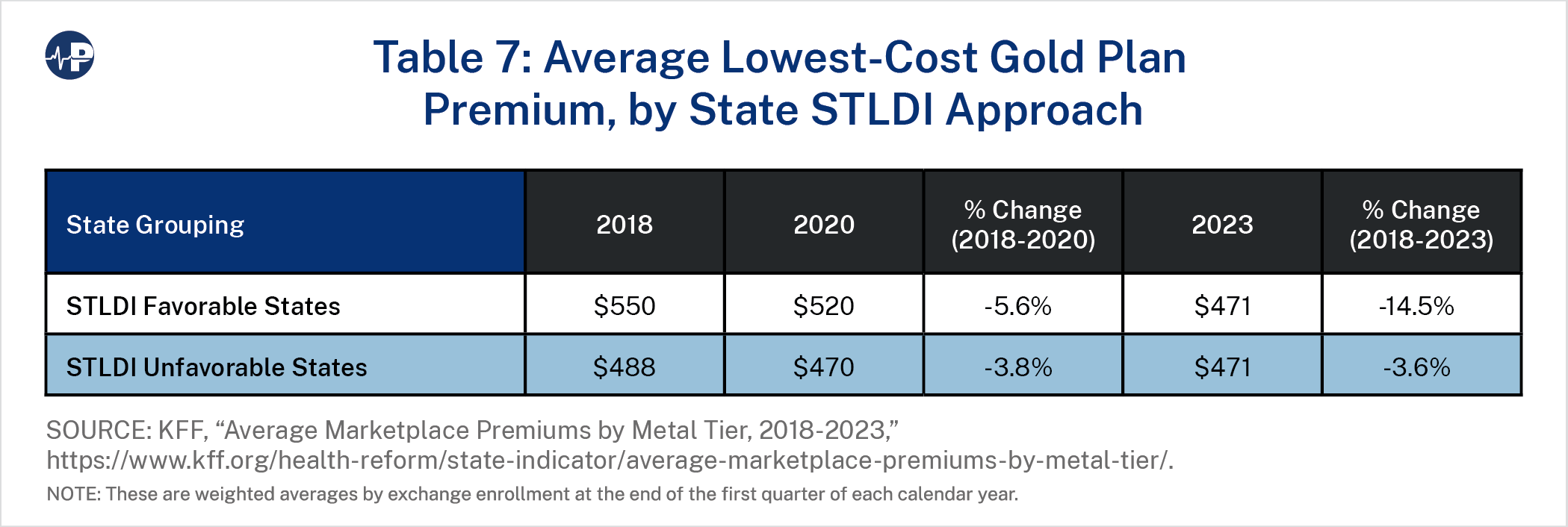

Table 7 shows the trends in the lowest-cost gold plans between STLDI favorable states and STLDI unfavorable states. From 2018 to 2020, premiums declined in STLDI favorable states by about 6 percent and STLDI unfavorable states by about 4 percent. However, by 2023, a much more favorable premium trend appeared in STLDI favorable states—a 15 percent reduction in gold plan premiums versus a much smaller decline (4 percent) in STLDI unfavorable states. If adverse selection were happening in STLDI favorable states, it would almost certainly involve gold plan premium increases, as people with greater need of medical services tend to purchase coverage with lower amounts of cost-sharing. As there are much larger gold plan premium declines in STLDI favorable states, there is no evidence of adverse selection in these states.

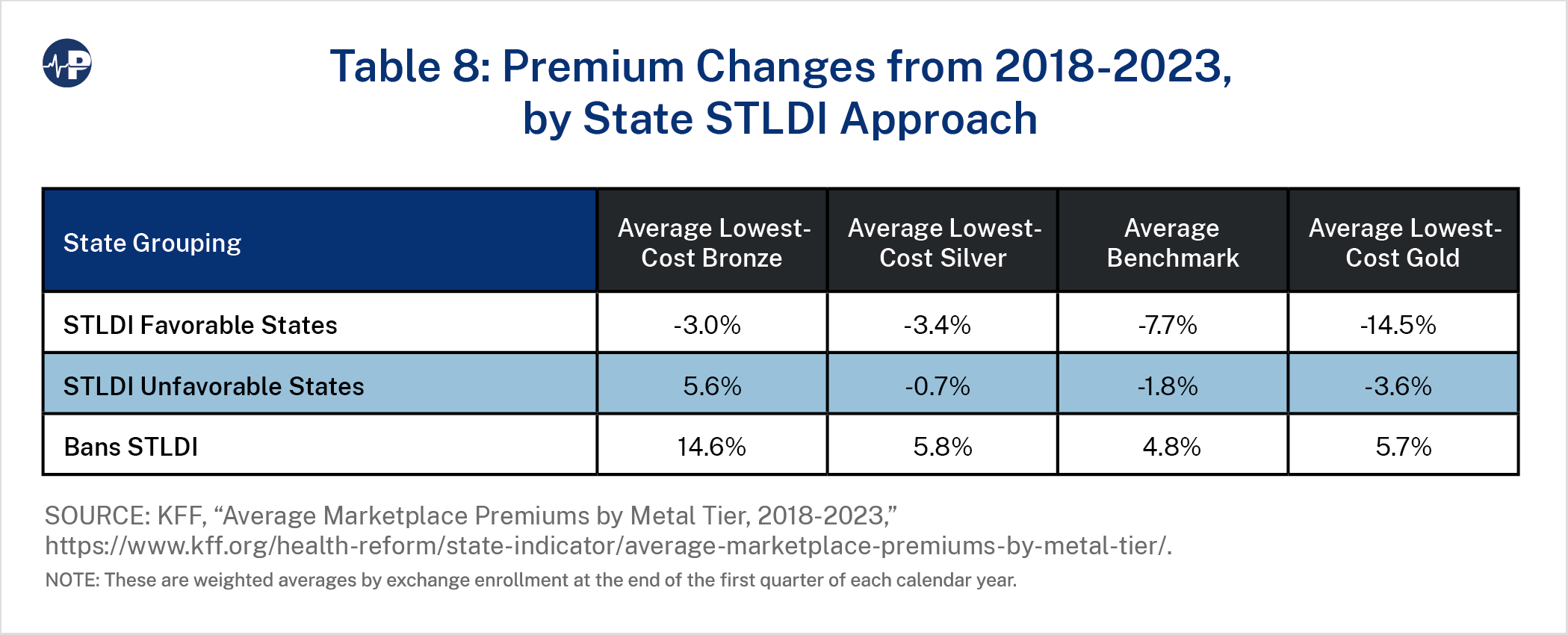

As Figures 4-7 in the appendix show, the exchange plan premium trends in states that restrict but permit STLDI were much more favorable from 2018 to 2023 than the trends in states where STLDI is not sold. Table 8 puts all the premium information together, showing the change in exchange premiums from 2018 to 2023 based on state approaches to STLDI. In every category, the best premium trends (premium reductions) were in STLDI favorable states, while the worst trends (premium increases) were in states where STLDI is not sold.

Impact of 1332 Waivers

In 2018 and 2019, theDepartment of Health and Human Services approved nine state applications for 1332 reinsurance waivers. Section 1332 of the ACA permits states to request that the government waive certain provisions of the ACA for those states. Using these waivers, states contribute funds forreinsurance programs,through which insurers receive government supportto cover a large share of the costs of people who incurred significant claims during a year. These states received federal funds back, generally around 60 percent of the amount that they put up, as the program lowered premiums and premium tax credits as a result. Of the ninestates,three—Montana, North Dakota, and Wisconsin—are STLDI favorable and six—Colorado, Delaware, Maryland, Maine, New Jersey, and Rhode Island—are STLDI unfavorable.

Excluding the 1332 states did not meaningfully change the results: Enrollment, insurer participation, and premium trends were all much better in STLDI favorable states than in STLDI unfavorable states. Waiver states did have the least attrition in their off-exchange markets and excluding 1332 states resulted in the STLDI unfavorable states having slightly more attrition in the off-exchange market than the STLDI favorable states. The number of insurers entering the exchanges in 1332 waiver states was relatively low, but the premium reductions from 2018 to 2023 were much more pronounced in the 1332 waiver states.

Federal regulators have paid significant attention to STLDI over the past several years, with the Obama administration tightening federal rules, the Trump administration liberalizing federal rules, and the Biden administration now proposing to tighten them even further than the Obama administration did. The costs of additional restrictions are clear: People have fewer health insurance options, the options eliminated tend to be low cost, people who get sick during their coverage periods will lose that coverage earlier and lose access to any coverage for up to a year, and the number of people without health insurance will increase. The purported benefits are that people will no longer be led to purchase non-ACA-compliant plans when ACA-compliant plans would be best for them and that the ACA markets will improve by restricting alternative options for healthy people.

There is no evidence that the ACA market would be better off from restricting insurers’ ability to sell STLDI plans that last up to a year. This study found that enrollment, insurer participation, and premium trends were all much more favorable after 2018 in states that fully permitted STLDI relative to states that restricted STLDI. The trends in the ACA market were the worst in states where people did not have the ability to purchase STLDI. In fact, this evidence suggests that states that restrict STLDI harm their ACA individual markets. This could happen for a few reasons, including that such restrictions cause overall competition in the state insurance market to decline, leaving less attractive plans, and because longer-term STLDI means that people who develop expensive conditions stay out of the ACA markets for longer.

Overall, this analysis strongly suggests that the intended beneficial effects the Biden administration anticipates from its proposed STLDI restrictions will not materialize. The costs of these restrictions will almost certainly dwarf any benefits. The Biden administration should withdraw its proposal.