On February 17, 2022, Paragon’s Brian Blase testified before the House Committee on Education and Labor Subcommittee on Health, Employment, Labor, and Pensions.

Exploring Pathways to Affordable, Universal Health Coverage

My name is Brian Blase, and I was privileged to work for the House Committee on Oversight and Government Reform from 2011 through 2014. You have vital jobs serving the American people, and it is an honor to testify before this Committee today on this important topic.

I am the founder and president of a new health policy think tank—Paragon Health Institute. My testimony today represents my views and not those of Paragon. I am also a senior research fellow at the Galen Institute and a visiting fellow at the Foundation for Government Accountability. From 2017 through 2019, I served as a Special Assistant to the President for Economic Policy at the White House’s National Economic Council. In that capacity, I led policy and regulatory work on several areas that I am testifying about today, including Association Health Plans, short-term limited-duration health plans, individual coverage health reimbursement arrangements, and price transparency rules.

The title of today’s hearing is “Exploring Pathways to Affordable, Universal Health Coverage.” I’m here to discuss how we can achieve more affordable, higher quality health care—a worthy goal that nearly everyone supports. The goal of achieving universal health coverage can only be achieved if both health care and health coverage are affordable—and for too many people today, they are not. I will focus my testimony on how to achieve more affordable and higher-quality health care which will lead to millions more people having health coverage.

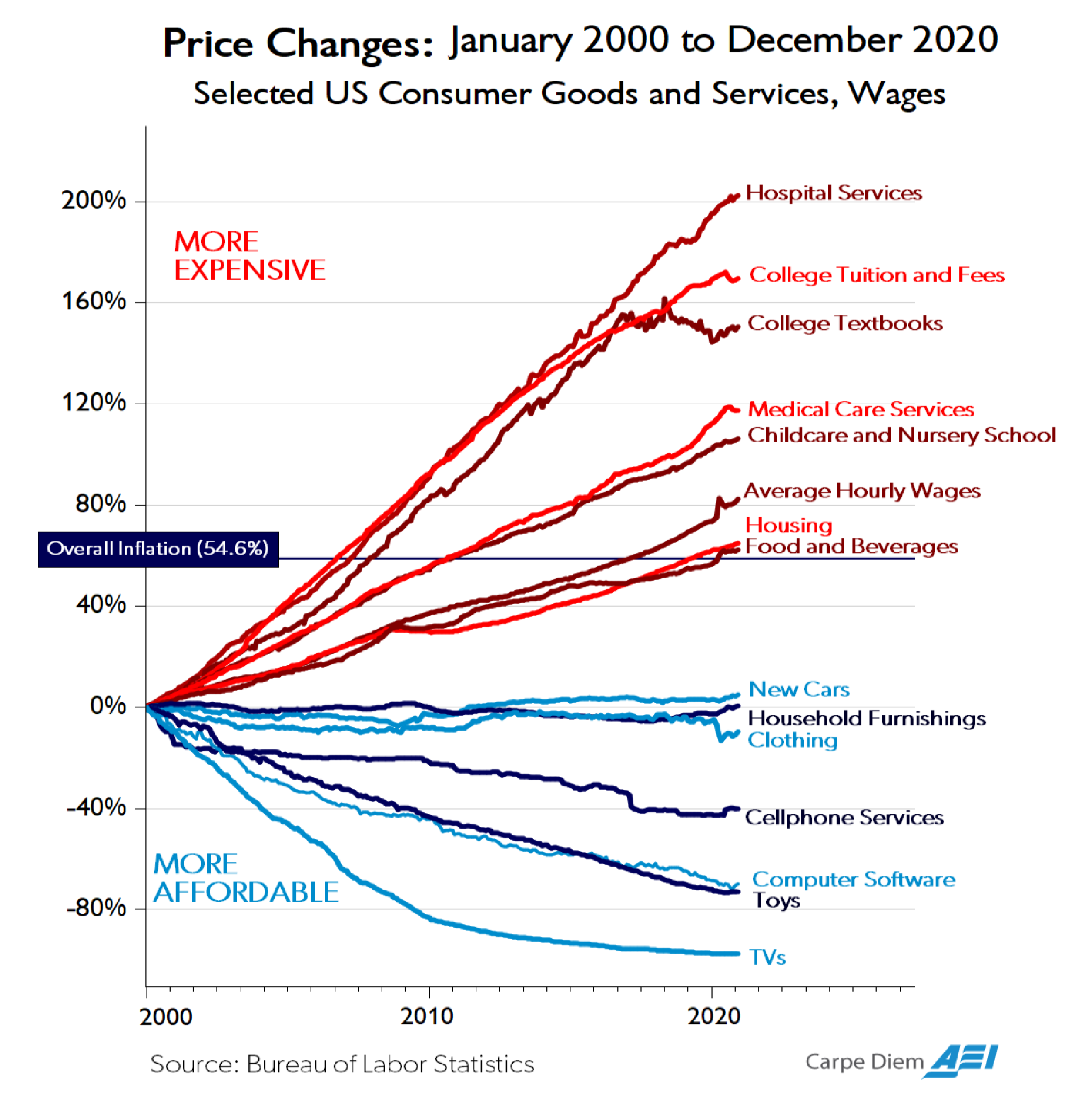

In many areas of the economy, products and services have become higher in quality over time while real prices, after accounting for inflation, have declined (Figure below: “Price Changes”).1 Unfortunately, this has not been the case for most health care products and services.2 As the following figure shows, prices for hospital services—the largest component of health care expenditures—have increased more than three times faster than general inflation over the past two decades.3 As health costs have risen, insurance premiums have correspondingly soared, even as plan deductibles have risen dramatically. In 2020, health care spending was 19.7 percent of U.S. Gross Domestic Product, a 6.4 percentage point increase and 48 percent increase from the 13.3 percent of U.S. GDP expended on health care in 2000.4 Importantly, over the past few decades, there have been some noticeable advances in health, such as a decline in cardiac mortality, improvement in cancer survival rates, a cure for Hepatitis C, and new AIDS treatments. However, there is also significant waste in the health sector and health outcomes have recently stagnated despite the Affordable Care Act’s (ACA) new spending and the significant expansion of Medicaid. American life expectancy was lower in 2019 than it was in 2013, before the ACA’s coverage and spending provisions took effect.5

Government Impact on Rising Health Care Prices and Costs

Current Policies

There are many policies—at both the federal and state levels—that raise health care prices and costs. Generally, high prices convey high value. But in health care because of government’s involvement, excessive third-party payment, and generally consolidated markets—high prices are often not a reflection of high value. A major consideration for policymakers in addressing high prices for medical care should be examining how existing government policies contribute to the problem and then focusing on reform.

A primary way that government inflates health care prices and costs is through tax and spending policies. In 2020, government health care spending—including both state and local government spending—was half of total U.S. health care expenditures.6 Federal policy also has a major influence over private sector health care spending, particularly through the tax exclusion for employer-sponsored health insurance. The Tax Policy Center estimated that this tax exclusion reduced federal revenue—both income and payroll tax collections—by $273 billion in 2019.7

The key economic reality is that when government subsidizes something, that thing becomes more expensive. Subsidies increase demand, raise prices, and thus increase total spending in that area. For complete economic analysis, the taxpayer share of the total cost must be considered. For households to receive subsidies, other households must finance those subsidies. This financing can occur through higher taxes or through greater debt. More debt represents higher taxes in the future, either through direct taxes or higher inflation.

Reforming government health care subsidies is crucial to making health care more affordable for families, businesses, and taxpayers. While such reform is critical to reducing health care cost pressures on family and government budgets, I am generally limiting my testimony on federal health care subsidies to current proposals that would make the existing problems even worse.

Health Subsidy Design Flaws

Although the magnitude of government subsidies for health care increases prices and spending, the design of the subsidies is also problematic. Historically, government programs and tax policy have encouraged third-party payment of health services. Thus for the vast majority of health care transactions, individuals do not directly spend their own money but instead rely on a government program or their insurance plan. Insurance should play a significant role in financing catastrophic and expensive care but having insurance pay for routine and shoppable services rather than relying on markets for these services distorts decision-making and leads to overconsumption and waste. While inflation in health care services has been substantial, health care services where third-party payment is limited—such as cosmetic surgery and Lasik-eye surgery—have had real price declines as quality has significantly improved.8 Also, a number of physician practices and medical centers, such as the Oklahoma Surgery Center, do not accept insurance and have much lower average prices.9

As I discuss below, the ACA made individual market health insurance less affordable and introduced a generally inefficient set of subsidies. The ACA expanded coverage in two ways—with a large Medicaid expansion funded almost entirely by federal dollars and with new premium subsidies to help people afford individual and small group insurance that was made much more expensive because of the ACA’s extensive new federal regulation.

Nearly the entire net coverage gains from the ACA occurred through Medicaid expansion, although many people who gained coverage through Medicaid were, in fact, not eligible for the program.10 Enrollment in individual market changes through the exchanges has largely been disappointing, falling far below original projections. From 2015-2020, exchange enrollment averaged about 10-11 million people11—about 60 percent below what the Congressional Budget Office projected in May 2013 in its last analysis before the ACA’s provisions took effect.12

Low exchange enrollment may be explained by the individual market premiums increasing 105 percent from 2013 to 2017.13 The vast majority of enrollees receive large subsidies as the premium increases have largely priced unsubsidized individuals out of the market.

For the unsubsidized in 2021, the average exchange plan annual premium plus deductible for a family of four was about $25,000—meaning that a family needed to spend about $25,000 before they received any real meaningful financial benefit from their insurance.14 In addition to the high cost, ACA plans tend to have narrow networks, excluding the best hospitals and doctors in local regions. For example, in Texas, not a single ACA plan covers Houston’s world-renowned MD Anderson Cancer Center.

Rather than addressing underlying problems with the ACA that caused high premiums and deductibles and narrow plan networks, the American Rescue Plan Act (ARPA) further increased subsidies for this coverage. These subsidies have multiple problems, including being inflationary and inefficient. They push up prices and premiums, and they are a poor use of taxpayer dollars since much of the benefit accrues to higher-income people who are already insured. I further detail the subsidies’ problems below.

Due to these problems, the projected subsidy expansion in ARPA equates to about $17,000 each year per newly insured individual. The expanded subsidies will increase exchange enrollment but will do so by shifting more cost to the taxpayer. For example, an individual who faced a $600 monthly premium and qualified for a $500 subsidy and refused to purchase ACA coverage would likely enroll if an expanded subsidy covered the entire cost of the premium. HHS reported that 14.5 million people enrolled in coverage or were automatically re-enrolled in coverage for the 2022 plan year through January 15, 2022—a 21 percent increase from the previous year before the ARPA’s increase in taxpayer subsidies.15

Increasing Affordable Health Coverage Without New Federal Spending

There are ways to increase affordable health coverage without new federal spending. Many policies implemented by the previous administration expanded affordable coverage options for families and workers without new federal spending.

These policies included:

- expanded coverage options through Association Health Plans (AHPs) and short-term limited-duration health plans,

- new flexible financing methods through individual coverage health reimbursement arrangements (HRAs), and

- price transparency policies intended to improve the functioning and efficiency of health care markets.

Key Facts: Limits of Insurance and Medicine

While access to affordable health coverage and care are important, it is vital for policymakers to recognize two key facts. First, a large amount of medical spending is wasteful—with some of it even harmful to patients. Second, health insurance expansions, particularly through government programs such as Medicaid, tend to have disappointing results in terms of health improvements.

A significant concern with our high medical spending is that a large share of it—estimated by some researchers to be 25 percent of spending—does not provide Americans with any benefit.16

In fact, some of that spending may instead harm our overall health. A 2016 study found that medical errors are the third leading cause of death in the United States and as many as 250,000 people die each year from errors in hospitals and other health care facilities.17 Medical tests and treatments all carry some risk. Those that are unnecessary will result, on balance, in harm to patients.18

The impact of health insurance on health is not as clear or as positive as commonly believed. At a macro level, despite the significant increase in health coverage beginning in 2014 as a result of the ACA, American life expectancy declined for three straight years from 2014 through 2017.19 The 2018 Economic Report of the President by the White House’s Council of Economic Advisers put it this way:

[T]he evidence shows that health insurance provided through government expansions and the medical care it finances affect health less than is commonly believed. Determinants of health other than insurance and medical care—such as drug abuse, diet and physical activity leading to obesity, and smoking—have a tremendous impact and have exacerbated recent declines in life expectancy, despite the ACA’s increased coverage.20

The report evaluated numerous studies, including the two well-known health insurance experiments—the RAND health insurance experiment and Oregon’s Medicaid experiment—in its conclusion that expansions of government coverage produce limited health benefits. They suggest at least four reasons why health insurance, through government coverage expansions, have a minimal effect on health.

According to the report, “The first three of these reasons—that the uninsured were often able to obtain care before coverage, access problems for patients who gain Medicaid coverage, and mandated insurance benefits that have a minimal impact on health—are particularly salient when examining the results of the ACA coverage expansion.”21

The fourth reason raised by CEA is that “public coverage may have limited or possibly negative effects on health because of its long-run impact on innovation. Many governments, particularly in Europe, have paired large coverage expansions with the imposition of price and spending controls. These centralized controls may have an adverse impact on medical innovation and make healthcare less effective and more costly to obtain in the future.”22 Of relevance to policymakers given this concern, Tomas Philipson, former Chairman of the CEA, co-authored a study that estimated that HR 5376 would significantly reduce drug innovation and that this reduction would lead to 135 fewer new drugs and a loss of 331.5 million life years in the U.S.23

Two recent studies have purported to show that ACA coverage expansions reduced mortality; however, these studies have been criticized as flawed.24 In his review of the studies, University of Chicago economist Robert Kaestner outlines several concerns about the methodologies employed and has concluded, “The studies were severely under-powered to detect a reasonably sized effect of health insurance … on mortality and, because of that, were prone to grossly overestimating the effect of interest if not get the direction of the effect wrong … The flaws of the two studies leads me to conclude that we learned little about the effect of health insurance on mortality from them.”25

The lack of clear health benefits from the expansion of Medicaid, which I detailed in a report released in the spring of 2020, should raise policymakers’ concern about additional subsidies that simply expand government spending on the current structure.26 I concluded that large coverage expansions disappoint for several reasons: the uninsured receive nearly 80 percent as much care as similar insured people, the crowd-out of potentially superior private coverage, and the indirect effects on others such as longer wait times for care.27

Furthermore, the ACA’s model of subsidization results in direct payments from the government to health insurance companies. A 2018 report from the Council of Economic Advisers found that health insurer profitability had soared—more than doubling the growth of the S&P 500 in the first four years of the ACA’s enactment.28 As I discuss further below, both the design of the ACA’s premium subsidies as well as the ACA’s Medicaid expansion were inflationary and resulted in high payments to health insurance companies. There have been a variety of news stories documenting how these programs that are intended to benefit lower-income Americans have produced windfall profits for health insurance companies.29

Guiding Principles

Policymakers should look for ways to reorient existing expenditures to minimize harmful distortions in the health care market and to expand families’ ability to access affordable health insurance coverage and affordable health care services. A guiding principle for reforming government health financing would be to allow Americans to control more of their own money for health care and coverage rather than to continue to have the government control how most of their money is spent. A guiding principle for reforming government health care subsidies should be to permit individuals and families’ greater control over the resources instead of having the government pay so much directly to insurers for restricted choices of plans. This includes Medicaid recipients, who also deserve more control over their care and coverage. Of note, a prominent economics study of Medicaid recipients found that they only value the program at 20 to 40 percent of the program’s cost—a testament to economic inefficiency.30

Policies to Increase Americans’ Options

Another way government policy inflates health care prices and costs is by restricting options available to consumers and patients and limiting the ability of doctors and other health care professionals to best treat their patients. I next provide several examples of how government can minimize harm caused by existing anti-competitive policies that push up prices. Given the Committee’s jurisdiction over self-insured employer plans, I will begin by focusing on employer-sponsored coverage.

Employer-sponsored coverage

Roughly half of Americans receive health insurance through their employer or the employer of someone in their family.31 Typically, employers offer workers comprehensive health insurance that covers a large number of hospitals and doctors. Workers at large firms often receive several different plans from which to choose, while most workers at smaller firms only receive one plan option.

Employers provide coverage for a variety of reasons, including that it is a tax-free employee benefit. Economists universally agree that employees pay for their health insurance in the form of reduced wages. This reality means that the rising premiums and overall costs for employer coverage have significantly eaten away at wage increases over this period.

According to the Kaiser Family Foundation’s survey of employers, the average premium for single coverage was $7,739 and the average premium for family coverage was $22,221 in 2021.32 In 2000, the respective premiums were $2,471 and $6,438.33 The premium includes both the employee share as well as the employer share; although referred to as the “employer share,” this amount is paid for by workers in the form of lower wages.

Over this two-decade period, premiums for individual coverage increased 213 percent, and premiums for family coverage increased 245 percent—much greater than the 60 percent increase in overall prices during this period. Although premiums for workplace coverage have increased, the increase in premiums for individual market coverage—which was much more affected by the ACA—rose far more rapidly since 2013.

Premiums for employer coverage increased by about 14 percent between 2013 and 2017, compared to the 105 percent increase in individual market premiums.34 Using 2013 to 2017 is the best period to measure the effect of the ACA on premiums because the ACA’s key provisions took effect in 2014. Additionally, 2017 was the first year without the ACA’s transitional reinsurance and risk corridor programs, which were intended to reduce premiums in the ACA’s transition period.

Since 2010, when the ACA was enacted, there has been a 20 percent decline in the number of workers covered by employer health benefits at firms with fewer than 50 workers and a 7 percent decline in the number of workers covered by employer health benefits at firms with between 50 and 200 workers.35 While there has been a sizeable drop in employees with employer coverage at small firms, coverage at large firms has remained steady.36

According to the Kaiser Family Foundation’s survey, the number one reason that small employers do not offer coverage is the high cost.37 Among small firms that do not offer health insurance, 74 percent believe employees prefer higher wages to health insurance benefits, compared to only 15 percent who believe employees prefer health insurance.38

Clearly, as premiums have increased, particularly in the individual and small group markets most affected by the ACA, enrollment in private coverage has generally declined. To increase coverage—the topic of this hearing—it is imperative to make coverage more affordable.

Considering the health care challenges facing employers and workers, particularly at smaller companies—the previous administration expanded Association Health Plans (AHPs) and individual coverage health reimbursement arrangements (HRAs), and promulgated price transparency requirements to improve shopping.

Association Health Plans (AHPs)

All employers—especially small employers—need additional options to provide coverage to their workers. One such option is to permit employers to band together to offer coverage through Association Health Plans. While AHPs have existed for decades, employers needed to have a close nexus in order to join together and offer coverage. For example, dental practices could form an AHP, but a dental practice and an auto mechanic shop in the same town could not.

In June 2018, the Department of Labor finalized a rule creating a new pathway for any employer, including sole proprietors, within a state and or common metropolitan area to join together and offer coverage through an AHP. This rule provided smaller employers a way to gain the regulatory advantages and economies of scale that large employers receive when offering health insurance.

As discussed in a Washington Post piece from early 2019, the AHP expansion had a promising start with most new AHPs launched by regional chambers of commerce.39 According to the Washington Post, “there are initial signs the plans are offering generous benefits and premiums lower than can be found in the Obamacare marketplaces.”40 The Post wrote that an analysis of the new plans showed they offered benefits comparable to most workplace plans and did not discriminate against people with preexisting conditions.41 A study by the Foundation for Government Accountability found that new AHPs produced savings of 29 percent on average.42 One local chamber of commerce that enrolled hundreds of employers was projected to save policyholders more than $2,000 on average.43 The Congressional Budget Office projected that these new AHPs would cover as many as 4 million people by 2023, half a million of whom would have been uninsured.44

Unfortunately, a March 2019 decision by a federal judge invalidated this new pathway.45 Although the Department of Justice appealed this decision and the appellate court heard arguments in November 2019, the court granted the Biden administration’s motion to pause the appeal while the DOL considers further agency action.

Given the litigation challenges and the Biden administration’s apparent opposition to AHPs, congressional action is likely necessary for businesses to benefit from the new AHP pathway. H.R. 4547, introduced by Rep. Walberg, would codify the Department of Labor’s 2018 rule. As projected by CBO, these new AHPs would help hundreds of thousands of businesses and millions of employees obtain more affordable health coverage and would reduce the number of uninsured. This increase in health coverage would involve no new federal spending.

Individual Coverage HRAs

In June 2019, the Departments of Health and Human Services, Labor, and the Treasury issued a rule creating individual coverage Health Reimbursement Arrangements (ICHRAs). Like AHPs, individual coverage HRAs should be bipartisan. They work within the ACA’s basic framework and should significantly increase individual market enrollment.

As of January 1, 2020, employers have been able to provide tax-preferred contributions through an individual coverage HRA, which their employees can use to purchase the individual market plan that work best for them. Most employers that offer health insurance only provide workers with a single option, so the HRA rule has the potential to significantly increase worker choice and control over their health insurance. Employees are currently limited to purchasing ACAcompliant plans in the individual market, although Congress could permit employees to use their HRAs to purchase a broader set of plans.

Individual coverage HRAs will help employers attract and retain employees, gain greater predictability over their health costs, and reduce administrative expenses, allowing them to better concentrate on their core business purpose. The rule should help reverse the decline in small employers that offer coverage to their workers. Moreover, the rule contains significant flexibilities for larger employers to offer coverage to part-time workers or hourly workers.

According to estimates provided in the June 2019 rule, 800,000 employers will offer individual coverage HRAs, and more than 11 million people will receive individual market coverage using this type of HRA by the middle of this decade.46 This rule is expected to reduce the number of people without health insurance by about one million.47 According to the Departments’ analysis, “Most of these newly insured individuals are expected to be low- and moderate-income workers in firms that currently do not offer a traditional group health plan.”48 Similar to AHPs, the increase in insured people through individual coverage HRAs involves no new federal spending.

Congress should consider codification of the 2019 HRA rule to enhance employers’ certainty about the future of defined contribution health insurance. Policies that improve the individual market would boost the opportunity for employers and employees to benefit from individual coverage HRAs. One such policy would be to permit states greater flexibilities over benefit requirements and pricing, such as widening the three-to-one age rating restriction in the ACA. There is not yet good data on the uptake of individual coverage HRAs, and there is a lot of education needed to ensure that employers and brokers understand them. Moreover, migration to individual coverage HRAs has been affected by employers’ understandable focus on weathering the pandemic as well as a general risk aversion to changing employee benefits in such a tight labor market.

Price Transparency

In 2019, HHS finalized a rule requiring hospitals to post complete price information starting in 2021. In 2020, HHS with the Departments of Labor and Treasury finalized a separate rule that requires health insurers and health plans to post complete price information starting this year.

Price information can enable both individual consumers as well as employers to be better shoppers of health care. Price information is particularly important in health care because it is a large part of the typical families’ budget and because there is significant variation in prices—with prices for the same service often varying by magnitudes, even within the same geographic area.

I analyzed these requirements and their potential impact in a 2019 report.49 Expanded price transparency should result in five benefits.

- First, price transparency will encourage more consumers to shop and obtain lower prices.

- Second, price transparency will help employers establish better payment structures. These payment structures include reference pricing models, in which the plan sets a payment rate regardless of which provider delivers the service and which have been shown to generate significant savings.

- Third, price transparency will better enable employers to monitor the effectiveness of their insurers by comparing different rates received by providers across payers and across regions.

- Fourth, transparent prices should help employers eliminate counterproductive middlemen and contract with other entities that will incentivize employees to utilize lower-cost providers, including ones outside of their local region.

- Fifth, just as sunlight is often the best disinfectant, price transparency will better enable consumers and the broader public to hold providers accountable when prices reach outrageous levels.

All these policy recommendations are organized around increasing choice and competition in the health sector, leading to greater affordability of care and coverage.

Expanding Health Care Choice and Competition While Limiting Wasteful Subsidies

The remainder of my testimony is focused on policies that would put needed downward pressure on health care costs and expand consumer access to more affordable care. I discuss four areas:

- Empowering consumers financially

- Promoting consumer-directed coverage options

- Enhancing competition to lower prices

- Reducing wasteful and inefficient subsidies.

Empowering Consumers Financially

Very little of our health care spending is under the consumers’ direct control. Nearly 90 percent of Americans’ spending on health care consists of third-party payment—either through their private insurance plan or through a government program. Health savings accounts (HSAs) are one example of initiatives created to put more control in the hands of consumers and improve their incentives to obtain value from their health care expenditures.

Unfortunately, current government rules allow HSA contributions only for people who have insurance coverage that meets narrow criteria. This restrictive structure precludes most Americans from contributing to an HSA. In 2019, the IRS expanded the number of preventive services that could be covered by plans below the deductible and remain HSA-qualified.50 This reform enabled plans to reimburse for medications like statins and insulin before enrollees reached the plan deductible.

The most important HSA reform would be to expand the number of people who can contribute to HSAs. Specifically, people enrolled in plans with a variety of benefit designs, including seniors with Medicare, should be allowed to make HSA contributions.

Promoting Consumer-Directed Coverage Options

Consumer-directed coverage could be promoted by codification of not only the AHP and HRA rules discussed above but also a 2018 rule by the Departments of HHS, Labor, and the Treasury, which modified federal rules impacting the allowable contract period for short-term, limited-duration health insurance plans. These plans, which are subject to state regulation, are exempt from federal health insurance rules, including ACA requirements. As a result, they are generally much less expensive and more flexible for individuals and families. According to the Congressional Budget Office, premiums for short-term plans may be 60 percent lower than premiums for the lowest-priced ACA bronze plan.51 Unlike ACA-compliant plans, these plans are available to be purchased year-round, so consumers do not have to wait for open season to enroll.

In a fall 2016 rule, the Obama administration reduced the allowable contract length of these plans to three months, an action which drew strong criticism from the National Association of Insurance Commissioners (NAIC). NAIC argued that restricting short-term plans would harm people whose three-month coverage expired and who acquired some condition or illness in their coverage period:

[I]f the person develops a new condition while covered under the first policy, the condition would be denied as a pre-existing condition under the next short-term policy. In other words, only the healthy consumers would have coverage options available to them; unhealthy consumers would not.52

NAIC also argued that the Obama rule would not improve the individual market risk pool since healthy people could continue to get short-term coverage. “Only those who become unhealthy will be unable to afford care, and that is not good for the risk pools in the long run.”53

The 2018 rule change, reversed the Obama-era restrictions, allowing people to purchase plans with up to 364 days of coverage with renewals permitted for up to three years. This change has the effect of better protecting people, since they can maintain coverage without having to go through medical underwriting as frequently.

More than half of states fully allow their residents to benefit from short-term plans, and from 2018-2021, the individual market improved more in states that fully permit short-term plans than those that restricted them.54 Codifying this rule is another way to decrease the number of the uninsured without any new federal spending. The Congressional Budget Office estimated that the short-term plan rule would cover 700,000 people who would have otherwise been uninsured.55

Enhancing Health Care Competition to Lower Prices

In December 2018, the Departments of HHS, Labor, and the Treasury with input from the Federal Trade Commission (FTC) released a report recommending more than 50 actions that federal and state governments can take to increase competition in the health care sector.56 In my position at the National Economic Council, I coordinated the work across the federal departments and agencies on this report. The following are important recommendations contained in or based on recommendations made in that report:

- Expanding site-neutral payments. In the previous administration, HHS pursued site neutral payments in the Medicare program. These payments reduce spending and—perhaps more importantly—reduce incentives for hospitals to acquire physicians’ offices. Medicare should not pay more for care provided in hospital-affiliated medical facilities that could be safely and effectively provided in either physicians’ offices or ambulatory surgical centers. Further reductions in spending, increased competition, and lower prices could be accomplished by Congress expanding the number of services paid the same through Medicare regardless of the site of care.

- Lifting limits on physician-owned hospitals. The ACA prohibited Medicare from reimbursing for services provided in physician-owned hospitals constructed after 2010. The moratorium on physician-owned hospitals reduces competition in hospital markets and seems especially problematic since such hospitals have a track record of providing high-value care. Rescinding the moratorium will increase competitive pressure on existing hospital systems and should lead to decreased prices with improved accessibility and quality of services.

- Improved Federal Trade Commission (FTC) oversight. There has been enormous growth in health sector consolidation over the past few decades. Yet, federal antitrust policy is limited in its ability to review mergers between nonprofit health care entities. Amending the FTC Act to extend FTC’s jurisdiction to nonprofit health care entities would address this problem.

- Encouraging states to lift barriers to competition. Unfortunately, many restrictions on competition are enacted at the state-level. As discussed in Paragon’s state health reform book Don’t Wait for Washington: How States Can Reform Health Care Today, states place barriers on telehealth services, restrict access to health care services through certificate of need and certificate of public advantage laws, and limit health care professionals’ ability to practice to the top of their ability as well as their mobility to practice wherever their services are most in demand.57 These restrictions all reduce patient access to care. Congress could consider conditioning some of the enormous amount of money it sends to states for health care purposes on state laws and policies that affect overall competition in the market.

Reforming Wasteful and Inefficient Health Care Subsidies

The federal government—through tax and spending programs—inflates health care spending and is responsible for substantial expenditures that provide little, if any, benefit to Americans. As mentioned above, estimates indicate that up to 25 percent of spending on health care provides no benefit, with some of it actually harmful, to our health. Reforms are clearly needed, particularly to our health care entitlement programs, but first it is important to not make the current problems worse.

Several recent health care proposals would increase inefficient health care spending and, in doing so, would exacerbate inflationary pressures in the economy. A far more efficient approach than expanding ACA subsidies would be for policymakers to redirect a portion of existing government spending on health care to financing high risk pools or state reinsurance programs. Such an approach, as demonstrated by the 15 states that have used Section 1332 waivers to establish reinsurance programs, would better target federal funds to individuals who have expensive medical conditions or who experience significant spending during a period of time.58

American Rescue Plan Act’s problematic expansion of ACA subsidies

The American Rescue Plan Act (ARPA) contained a significant expansion of subsidies for ACA exchange plans. ARPA increased the amount of taxpayer assistance that people receive to purchase exchange plans in two ways. First, it reduced what people with income between 100 and 400 percent of the federal poverty level (FPL) need to pay for a benchmark plan. Second, it lifted the cap on subsidy eligibility at 400 percent of the FPL.

The expansion of these subsidies is particularly problematic for many reasons.

- First, three-quarters of the new spending is on people who already have coverage. Because of this, the projected cost per newly insured person is $17,000 a year.

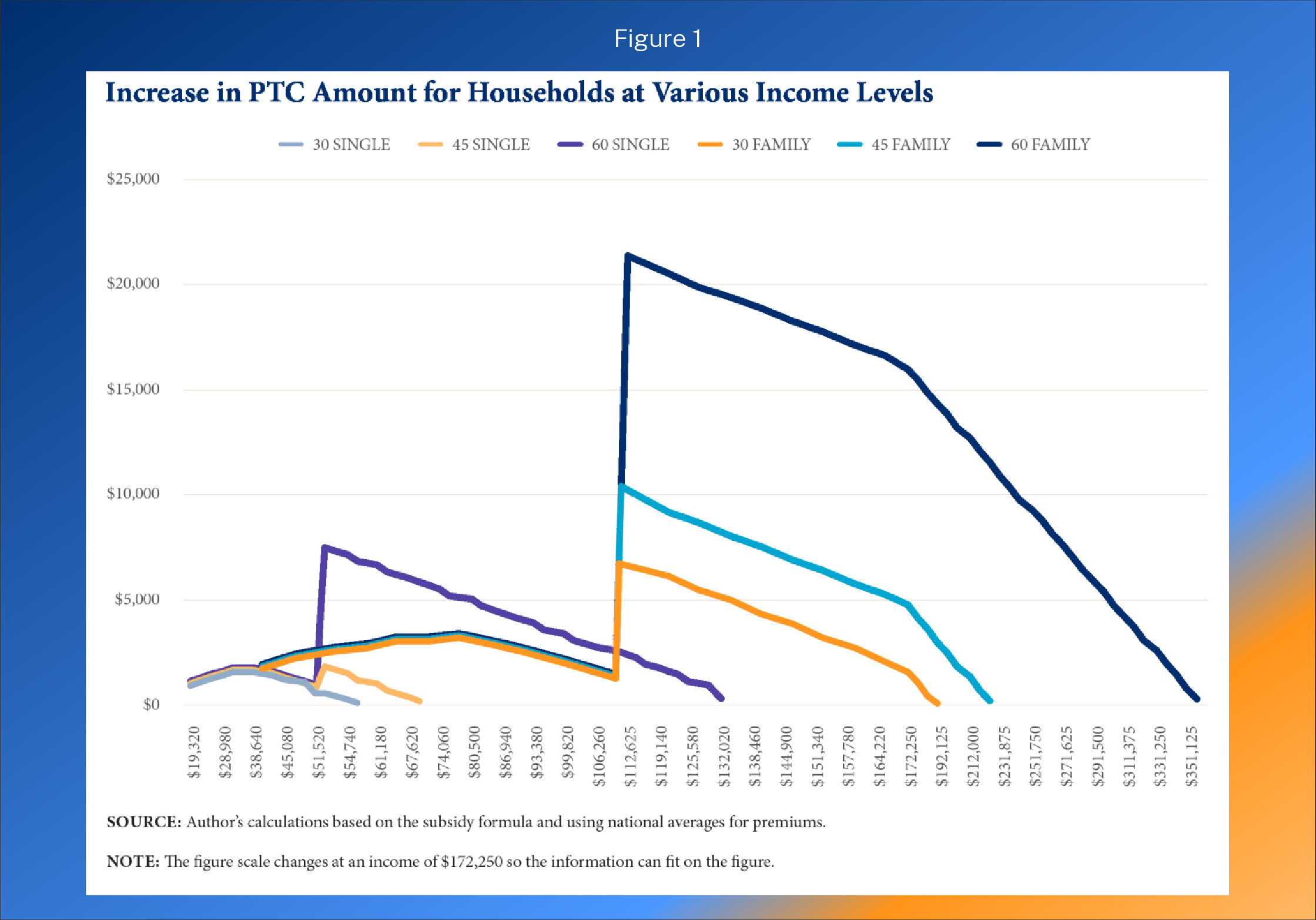

- Second, as the figure below (taken from a report I authored for the Galen Institute last year)59 demonstrates, the relatively wealthy receive far more benefit from the subsidy expansion than lower-income families. The figure shows the benefit in expanded premium tax credits (PTCs) for six different households at various income levels.

- Third, the subsidies go directly to health insurance companies, subsidizing their profits even though enrollees may place low value on the coverage and would prefer different health care and health coverage products.

- Fourth, if the subsidies are extended, millions of people will likely lose workplace coverage. This will be especially true of employees at smaller firms that are not subject to tax penalties from the ACA’s employer mandate.

- Fifth, the subsidies are inflationary in their design and will drive up health care prices and health spending, as well as prices throughout the economy.

- Sixth, the expansion of these subsidies will likely result in an annual federal spending increase of about $30 billion or more, depending on the extent of employer drop as the subsidies are generally larger than the tax revenue loss associated with the tax exclusion for employer coverage.

In areas of the country where exchange premiums are high, the expansion of the ACA subsidies leads to generous taxpayer subsidies for affluent households. For example, the benchmark premium for an exchange plan in Prescott, Arizona, for a family of five with a 60-year-old household head is $50,412 in 2022.60 A benchmark plan covers 70 percent of a household’s expected health care expenses on average. Of note, the fact that the exchange plan for a family of five can be more than $50,000 a year suggests serious underlying problems with the program.

- If that family made $150,000, they would qualify for a subsidy of $37,662.

- If that family made $350,000, they would qualify for a subsidy of $20,662.

- If that family made $500,000, they would qualify for a subsidy of $7,912.

- This family does not lose subsidy eligibility until they make more than $593,000

Injecting more federal Medicaid dollars to stat

The Medicaid program finances health and long-term care expenses for mostly lower-income Americans, although lax eligibility enforcement has resulted in many people with income above eligibility thresholds enrolled in the program. A provision in the Families First Coronavirus Relief Act (FFCRA) exacerbated this problem by penalizing states that removed ineligible Medicaid recipients.

FFCRA increased the federal share of state spending by 6 percentage points, or by about 10 percent. In exchange for accepting these funds, states could not remove anyone from Medicaid, even individuals who were no longer eligible for the program. As such, there are as many as 15 million people on Medicaid who are ineligible.61 Previous audits conducted by HHS suggest that some of these people may not even know they are enrolled on Medicaid.62

In addition to worsening eligibility problems, the surge of Medicaid spending has been misdirected and inflationary. States enjoyed record revenue collections over the past two years, so they did not need additional funds.63 States used the additional federal money, including about $30 billion in higher Medicaid payments in 2021 from ARPA, to increase overall spending. As spending by government goes up, more money is chasing the same amount of goods and services, so prices rise.

The ACA expanded Medicaid to a new class of enrollees—able-bodied, working-age, and generally childless adults with incomes below 138 percent of the FPL. From 2014 to 2016, the federal government reimbursed 100 percent of state spending on this expansion population. Although that rate has declined, it is now 90 percent. There are serious equity concerns with the federal government paying a much higher rate for the expansion population than for traditional Medicaid enrollees, such as lower-income children, pregnant women, seniors, and people with disabilities. It is likely that these higher payment rates divert resources away from those most in need. For example, most states have waiting lists for Medicaid services for people with intellectual disabilities.

The higher payment rates also present states with significant incentives to misclassify individuals as eligible under the Medicaid expansion. Following the ACA’s expansion of Medicaid, improper payment rates in the program surged—from less than 6 percent in 2013 to 22 percent now.64 Federal improper Medicaid payments are now $100 billion per year, a figure which likely grows to $150 billion a year when state spending is also included. In a Mercatus Center research project, University of Kentucky economist Aaron Yelowitz and I reviewed many state audits of Medicaid eligibility processes conducted by the Inspector General at the Department of Health and Human Services.65 Across those audits, the IG found “systemic errors include neglecting to obtain proper documentation; failing to properly verify income eligibility; misclassifying individuals, including into the newly eligible category; and failing to properly verify citizenship.”66

This waste of taxpayer dollars is a growing problem that speaks directly to the rising costs of health coverage. There is a crucial need for policymakers to address this waste, so taxpayer resources can be focused on ensuring the programs are serving their target populations.

In the past few months, various proposals have emerged that would further increase federal Medicaid spending, including a new home and community-based program through Medicaid. If states want to enact new programs, they can. Crucially, programs would likely be much more efficient if they were financed with state dollars instead of mostly with federal dollars. Although this principle always applies, pumping up federal Medicaid spending at a time of record high inflation and state revenues is certainly not fiscally responsible or wise. Rather than expanding federal Medicaid spending, conducting meaningful oversight of the program, including the surging improper payments in the program, would be a more prudent approach for Congress.

Conclusion

Renowned health economist and Harvard Business School professor Regina Herzlinger has written that “choice supports competition, competition fuels innovation, and innovation is the only way to make things better and cheaper.”67 Unfortunately, government policies—despite good intentions—often stifle choice, competition, and innovation in health care. Furthermore, these programs and policies produce incentives that lead to waste rather than value in our health care expenditures.

- Government mandates have pushed up the price of insurance. The high price of insurance necessitates large subsidies, so people can afford the coverage.

- Government restricts people from buying coverage that works best for them and prevents small employers from joining together to gain the same advantages that large employers obtain in their coverage.

- Government prohibits health care professionals from practicing to the top of their license and limits health care supply through rules such as anti-competitive certificates of need.

- Government contributes to higher health care prices and overall inflation with poorly designed subsidies.

Although increasing subsidies may be tempting, expanding inefficient health care subsidies makes health care less affordable. Government spending replaces private spending that would have otherwise occurred. Government subsidies often permit insurers to raise premiums with taxpayers on the hook for the higher premium cost. The subsidy cost of $17,000 per newly insured from the expansion of exchange premium subsidies by the American Rescue Plan Act is testament to its inefficiency. Extending the ACA premium subsidies beyond 2022 would further fuel higher health care prices and inflation in the economy.

Fortunately, by reforming existing government programs and pursuing policies that promote choice and competition in health care, policymakers can expand access to affordable health coverage without new government spending.

The following policies, if fully implemented, would help millions of families, and reduce the number of uninsured by a projected two million people—all without any new federal spending:

- Association Health Plans, which offered significant savings to small employers for highquality coverage.

- Short-term plans, which helped families in need of flexible, affordable coverage.

- Individual coverage health reimbursement arrangements, which permit employers a way to provide health coverage in ways that employees may prefer.

In addition to the expansion of coverage opportunities, new price transparency rules that are properly implemented can improve the functioning of health care markets and expand opportunities for consumers and employers to maximize value from their expenditures.

Another policy strategy needs to be reconsidered: much of federal policy in the past decade has focused on increasing funds to states to expand Medicaid. However, increasing federal Medicaid funds is inflationary because it increases federal debt and states can raise spending—with weak evidence of overall health benefit from Medicaid expansion. Moreover, those for whom Medicaid was created are being crowded out:

- The ACA’s funding structure discriminates against traditional program recipients such as low-income children, pregnant women, seniors, and individuals with disabilities in favor of the expansion population of able-bodied, working-age adults.

- Millions of people are currently enrolled in the program who are not eligible because of lax state approaches to ensuring eligible people are on the program. Given the 22 percent improper payment rate in Medicaid, Congress should strengthen and expand oversight of the program that has clearly grown beyond some states’ ability to properly manage.

Lastly, policymakers should avoid centralized regulatory or price controls that would diminish health care innovation. Rather policymakers should pursue policies that create a climate conducive to innovation in which entrepreneurs are best serving patient needs.

Thank you for the opportunity to testify before the Committee today, and I look forward to your questions.

The following clips feature Dr. Blase before the House Ways and Means Committee.